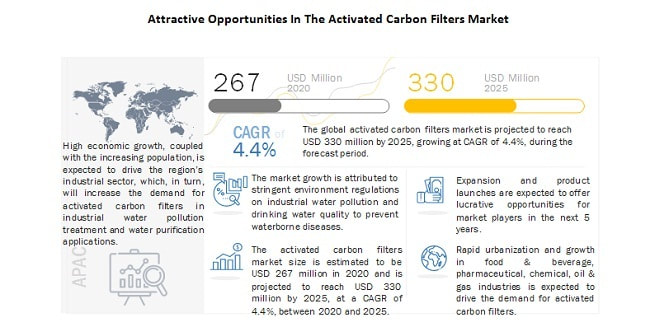

The global activated carbon filters market size is estimated at USD 267 Million in 2020 and is projected to reach USD 330 Million by 2025, at a CAGR of 4.4%, between 2020 and 2025. Activated carbon filters are used to remove organic compounds, and free chlorine from water to make it suitable for drinking and reuse in manufacturing processes or to discharge in water bodies. They are used to remove organic elements, such as humic acid and fulvic acid from potable water to prevent the formation of trihalomethanes, a class of carcinogens. They are also used for air/gas filtration in various industries. The filter media, which is used in the filtration process is activated carbon, also known as activated charcoal. Activated carbon is a form of carbon that removes organic compounds from liquids and gases by a process known as “adsorption”. It is extremely porous and thus has a very large surface area available for adsorption. APAC is estimated to be the largest market for activated carbon filters in 2019. The market for this region is segmented into China, India, Japan, Malaysia, Indonesia, and the Rest of APAC. According to the World Bank, APAC is the fastest-growing region in terms of both population and economy. The region has witnessed significant growth in the past decade, accounting for over one-third of the world’s GDP. High economic growth, coupled with the increasing population, is expected to drive the region’s industrial sector. This is expected to increase the demand for activated carbon filters in water pollution treatment and water purification applications. The key players in the activated carbon filters market are TIGG LLC (US), Puragen Activated Carbons (US), Cabot corporation (US), Westech Engineering (US), Kuraray Co. Ltd. (Japan), Lenntech B.V. (The Netherlands), Donau Carbon Gmbh (Germany), General Carbon Corporation (US), Sereco SR.L. (Italy), Carbtrol Corp (US). The activated carbon filters market report analyzes the key growth strategies adopted by the leading market players, between 2016 and 2019, which include expansions, new product developments, and collaborations. To know about the assumptions considered for the study download the pdf brochure TIGG LLC (US) is one of the leading players in the activated carbon filters market and a subsidiary of Newterra Ltd. The company offers a wide range of standard and custom made granular activated carbon adsorption and filtration systems. It provides filtration equipment for liquid and vapor treatment solutions for industrial manufacturing, municipal water treatment, air filtration, water filtration, environmental remediation application, and activated carbon & media exchange services. It is fully certified with ASME code shop and has both National R and ASME U stamp certifications. Puragen Activated Carbons (US) is one of the major players in the activated carbon filters market. The company provides activated carbon filters under the brand name OxGuard. Its high-grade carbon steel filtration vessel, meets material standards of FDA (Food & Drug Authority), EPA (Environmental Protection Agency), and AWWA (American Water Works Association). The company provides activated carbon filtration equipment to a wide variety of markets and applications, such as water filtration, air filtration, chemical manufacturing, decolorization and impurity removal in food & beverage, and pharmaceutical industries. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=213859954

0 Comments

The outbreak of COVID-19 has tightened travel restrictions in almost all countries globally. The increasing number of infected patients and total lockdown in major industrial hubs since March 2020 have brought the manufacturing industry to a halt. To curb the spread of the coronavirus, workers have either returned to their hometowns or have been quarantined. The potential upstream supply chain issues have forced the construction, automotive, chemical, textile & coatings companies to close sites. The demand for residential building construction is anticipated to be low, as negative consumer sentiment and declining incomes are discouraging people from seeking new homes. The demand for automotive has declined drastically due to uncertain future conditions. The impact on textile order for clothing and clothing accessories has dropped by 30% on average across the globe. Chemical manufacturing companies have halted their production or operating at a low utilization rate. However, gradually, the government bodies around the world are encouraging construction, automotive, chemical, and textile & coatings companies to resume work with the lifting of lockdown, and companies are working towards recovery of the market with the expected increase in sales gradually in 2021.

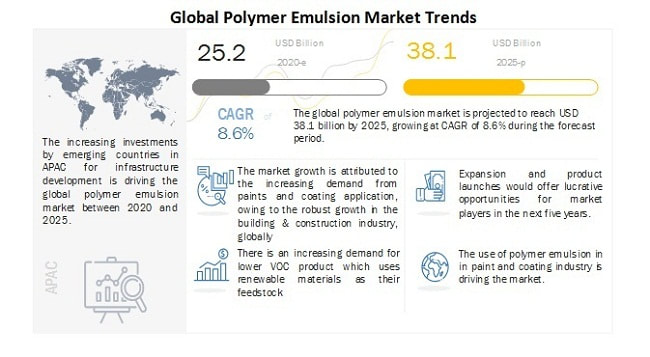

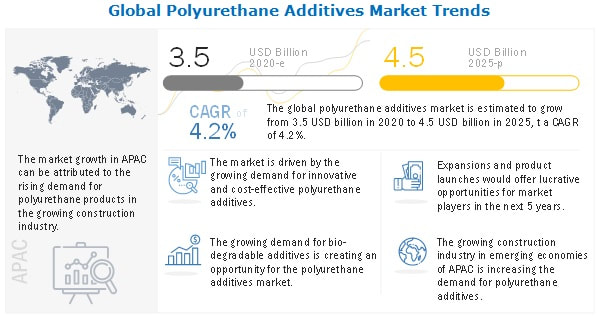

To know about the assumptions considered for the study download the pdf brochure The global polymer emulsion market size is estimated at USD 25.2 billion in 2020 and is projected to reach USD 38.1 billion by 2025, at a CAGR of 8.6%, between 2020 and 2025. Monomers dissolved in water are known as polymer emulsions. They are formed by a chain reaction known as emulsion polymerization. They are also known as waterborne polymers due to their water content. Polymer emulsions are used increasingly as substitutes for solvent-based polymers. Polymer emulsions have high molecular weight and are considered eco-friendly as they have low VOCs. The key applications of polymer emulsion are paints & coatings, paper & paperboard, adhesives & sealants, and others. Paints & coatings is the largest application in the polymer emulsion market The paints & coatings segment is the largest consumer of polymer emulsion. The growth of the market is attributed to the high demand in industries, such as construction and automotive. Polymer emulsion is used widely in paints & coatings as its manufacturing process has a lower carbon footprint. The high VOC content of solvent-based products and the implementation of government regulations regarding air pollution control has stimulated the development of low VOC paints & coatings. This increased the demand for water-based paints & coatings, which in turn, drive the growth of polymer emulsions in the paints & coatings segment. APAC is the largest and fastest-growing market for polymer emulsion. The region is witnessing growth in the polymer emulsion market because of the rapid expansion of building & construction, consumer durables, and transportation sectors. The manufacturers are attracted to the region as skilled labor required for the operation of manufacturing units are available at lower wages. The presence of major polymer emulsion manufacturers and stringent government regulation related to VOC emission are major factors supporting the growth of polymer emulsion in the region. DIC Corporation (Japan), Dow Chemical Company (US), BASF SE (Germany), Arkema Group (France), Celanese Corporation (US), Trinseo (US), The Lubrizol Corporation (US), Wacker Chemie AG (Germany), Synthomer Plc (UK), and Asahi Kasei Corporation (Japan) are the major players in the polymer emulsion market. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1269  The polyurethane additives market size is projected to reach USD 4.5 billion by 2025 at a CAGR of 4.2% from 2020. The demand for polyurethane additives market is increasing, owing to the growing demand for innovative and cost-effective additives.

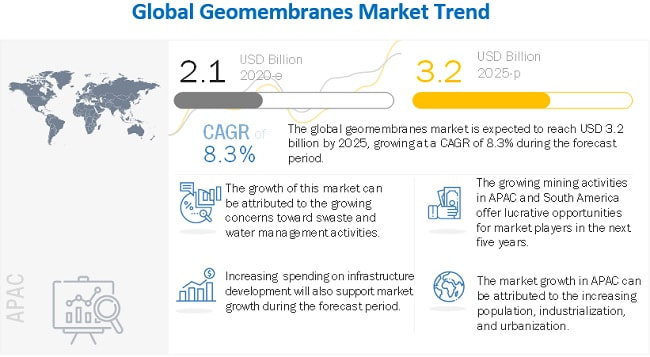

A few polyurethane additives are hazardous, and their application is limited owing to negative effects on polymer mechanical properties. Accordingly, identifying materials that are environmentally friendly and harmless to humans has become urgent. There are a few alternative polyurethane additives that are gaining research interest. Those are natural and recyclable resources that can enhance the flame retardant properties of other polymers. Room for improvement is always present as the related technology is continually developed. Hence, the growing demand for environment friendly polyurethane additives is creating a growth opportunity for the market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=121317889 The automotive & transportation industry to be the largest consumer of polyurethane additives Polyurethanes are used in various parts of an automobile. In addition to the foam that makes car seats comfortable, bumpers, interior “headline” ceiling sections, the car body, spoilers, doors and windows all use polyurethanes. Polyurethane enables manufacturers to provide drivers and passengers significantly more automobile mileage by reducing weight and increasing fuel economy, comfort, corrosion resistance, insulation, and sound absorption. APAC is projected to be the largest polyurethane additives market The polyurethane additives market in APAC is projected to register the highest CAGR during the forecast period. The foams market in APAC is driven by the growing construction industry, increased consumer spending, and strong economic growth. The recent COVID-19 pandemic is expected to impact the global automotive industry. The entire supply chain is disrupted due to limited supply of parts. For instance, Hubei province in China, which accounts for 8–10% of the Chinese auto production, is severely impacted by pandemic. Chinese suppliers around the globe have placed production lines on halt or shut them down completely. The legal and trade restrictions, such as sealed borders, increase the shortage of required parts. Such disruptions in supply chain is expected to affect the assembly of OEMs in Europe and North America. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=121317889 Increasing spending on infrastructure development driving the market of Geomembranes Market1/12/2021  The global geomembranes market size is expected to grow from USD 2.1 billion in 2020 to USD 3.2 billion by 2025, at a Compound Annual Growth Rate (CAGR) of 8.3% during the forecast period. This high growth is due to the increased mining activities in APAC and South America, the growing concerns towards waste and water management activities, and the increasing spending on infrastructure development.

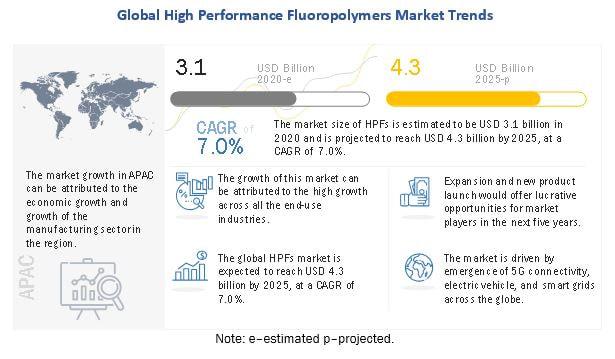

To know about the assumptions considered for the study download the pdf brochure Geomembranes Market Dynamics Driver: Increased mining activities in APAC and South America Rapid industrialization and urbanization in key countries such as China and India have spurred the demand for metals and minerals in the past few years. Other countries in APAC that have attracted significant mining investments include Australia, New Zealand, Japan, South Korea, Singapore, Mongolia, and Indonesia. South America is also a high-growth region for the mining industry. It has become a preferred destination for mining investments by major global mining companies. Key countries such as Brazil, Peru, and Chile have large mining capacities and have witnessed increased investments from foreign companies over the past five years. The mining industry is one of the major consumers of geomembranes. Geomembranes are used to help recapture and recycle the harmful chemicals being used in solution to treat ponds and secondary containment applications. This is expected to drive the geomembranes market during the forecast period. Restrain: Fluctuating raw material prices on account of volatility in crude oil prices Volatility in crude oil prices is one of the major restraining factor for geomembranes manufacturers. Most raw materials for geomembranes are petroleum-based and are vulnerable to fluctuations in crude oil prices. The rise or fall in crude oil prices directly impacts the price of the raw materials required for geomembranes. Manufacturers have to cope with high and volatile raw material costs, which reduce their profit margins. This scenario has compelled market players to enhance the efficiency and productivity of their operations to sustain growth and retain market share. Opportunity: Increasing spending on infrastructure development Infrastructure development includes creating water supply and treatment plants, roads, tunnels, dams, railways, airports, bridges, telecommunication networks, schools, and hospitals. According to the Confederation of International Contractors’ Associations (CICA), the output for residential and non-residential (including commercial, industrial, and others) infrastructures will grow by 85%, in terms of volume, to reach USD 15.5 trillion by 2030. There are a multitude of applications for geomembranes within construction sector.. The long shelf-life along with good physical & mechanical properties of geomembranes will work in favor of the market. Thus, growing infrastructural developments, are expected to create growth opportunities for the geomembranes market during the forecast period. COVID-19 Impact on the global geomembranes market The outbreak of novel coronavirus (COVID-19) pandemic has affected people in more than 200 countries across the globe. According to the International Monetary Fund (IMF), the global economy is expected to shrink by 3.0% in 2020. According to IMF, the pandemic has forced the global economy into the worst ever recession since the Great Depression of the 1930s. Many countries are under strict lockdown, which has forced several sectors to shut down their operations. Due to lockdown, manufacturing and construction activities are at a halt, and this has reduced the demand for geomembranes. In the second half of 2020, some countries have started to lift restrictions and gradually start business operations in various sectors. Even if the lockdown is being lifted, it will be challenging for the companies to get back to normal working conditions. This will subsequently affect the geomembranes market. Major vendors in the geomembranes market include Solmax (Canada), Raven Industries (US), AGRU (Austria), Carlisle Construction Materials LLC (US), Atarfil (Spain), PLASTIKA KRITIS (Greece), JUTA (Czech Republic), Maccaferri (Italy), Firestone Building Products (US), The NAUE group (Germany), Anhui Huifeng New Synthetic Materials (China), Carthage Mills (US), Environmental Protection (US), Geofabrics (Australia), Geosynthetics Limited (UK), Ginegar Plastic Products (Israel), Global Synthetics (Australia), Layfield Group (Canada), CETCO (US), Nilex (Canada), SOTRAFA (Spain), SOPREMA (France), Texel Industries Limited (India), Titan Environmental Containment (Canada), and US Fabrics (US). Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=133281673  The high performance fluoropolymer (HPF) market is projected to grow from USD 3.1 billion in 2020 to USD 4.3 billion by 2025, at a CAGR of 7.0%. The growth of the high performance fluoropolymer industry can be attributed to its high demand from various end-use industry and growing demand from renewables.

The high performance fluoropolymers are used mainly in the industrial processing. COVID-19 has severely impacted this industry HPFs are used in end-use industries such as transportation, electrical & electronics, medical, food processing, chemical processing, oil & gas, power plants, and building & construction. They are used in the industrial processing, where high thermal and chemical resistance is essential to conduct the operation. Due to the ongoing pandemic, industrial production has been severely affected throughout the world. Workforce shortage, logistical restrictions, material unavailability, and other restrictions have drastically slowed the growth of the industry. COVID-19 has led the industrial and manufacturing sectors into an unknown operating environment globally. Government restrictions on the number of people that can gather at one place have severely impacted the sector. For example, the component manufacturing sector is heavily hit by the impact of the virus. The production and factory operations in the automotive, electronics, and aerospace are on halt. Most of the industries are dependent on China for raw material supply. Hence, supply chain disruptions also have a major impact on industrial output. The global economy is contracting due to the pandemic. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=497 APAC is projected to be the fastest-growing HPF market APAC is expected to be the fastest-growing market for HPF, owing to the presence of large manufacturing and highly populated countries, such as China and India. China, India, Japan, Indonesia, and South Korea are some of the key countries in the HPF market in this region. In 2019, China accounted for the largest share of the APAC market, owing to the presence of huge chemical, automotive, medical, and electronics industries. The growing production of automobiles, consumer household, medical disposables, and their increasing demand across the region boosts the demand for HPF. Growth in the manufacturing of automobiles and electronics hardware across the region is expected to grow further with changing demographics. Owing to which APAC is projected to be the fastest-growing HPF market. The recent COVID-19 pandemic is expected to impact the global manufacturing sector. COVID-19 led the manufacturing sector into an unknown operating environment, globally. Government restrictions on the number of people that can gather at one particular place, severely impacted the industrial output. HPFs are used in end-use industries such as transportation, electrical & electronics, medical, food processing, chemical processing, oil & gas, power plants, and building & construction. They are used in the industrial processing, where high thermal and chemical resistance is essential to conduct the operation. Due to the ongoing pandemic, industrial production has been severely affected throughout the world. Workforce shortage, logistical restrictions, material unavailability, and other restrictions have drastically slowed the growth of the industry. Most active players in the HPF market: The Chemours Company (US), Daikin Industries (Japan), 3M (US), Solvay (Belgium), AGC (Japan), The Dongyue Group (China), GFL Ltd. (India), Halopolymer OJSC (Russia), and Hubei Everflon polymer (China) are a few active players in the HPF market. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=497 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed