The global fireproof insulation market is expected to reach USD 23.79 Billion by 2021, at a CAGR of 4.6% from 2016 to 2021. Key driving factors for the growth of the fireproof insulation market are the growth of the construction industry in emerging economies such as China, India, and Brazil and stringent building codes for fire safety in the developed countries such as the U.S., Canada, and Germany.

The global fireproof insulation market is a competitive market, with key players adopting various growth strategies to maintain or increase their shares in the global fireproof insulation market. The key companies offering fireproof insulation have been mainly involved in expansions and mergers & acquisitions. They have been rigorously adopting these strategies to strengthen their position in the global fireproof insulation market. The large players operating in this market have been taking initiatives to enhance their global reach, while small companies have concentrated increasingly on the development of new products. Download the PDF Brochure for more insight @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=231138768 The strategy of expansions has been most important growth strategy adopted by the fireproof insulation manufacturer. This strategy accounted for a share of 44% of all strategic developments that took place in the market. The strategy of new product launches was the second-most preferred growth strategy adopted by the manufacturers and accounted for a share of 27% of the total development strategies that took place in the global fireproof insulation market. Rockwool International A/S (Denmark), Knauf Insulation GmbH (Germany), Saint-Gobain S.A. (France), Owens Corning Corporation (U.S.), Berkshire Hathaway, Inc. (U.S.), BASF SE (Germany), and Paroc Oy (Finland) are some of the key players operational in the fireproof insulation market. Rockwool International A/S (Denmark), is the leading player in the fireproof insulation market. The company offers a wide range of fireproof insulations. The company follows both organic as well as inorganic growth strategies to increase its share in the global fireproof insulation market. The company serves both commercial and residential markets and has effectively managed expansion of its existing or new facilities, development of new products, and acquisition of its sales partners to expand its product portfolio globally. For instance, in June 2016, Rockwool International established a new production facility in Poland with an investment of 80 million Euros. This new production line will help Rockwool to meet the growing demand for stone wool insulation in the Polish market. In December 2015, Rockwool expanded production capacity at its plant in Bohumin, Czech Republic. This is expected to help the company to expand its presence in Central Eastern Europe. BASF SE (Germany) is another key player operating in this market. This company manufactures and supplies a wide range of fireproof insulations. The products range from performance polymers, polyurethanes, and basotect plastic foam fireproof insulation. BASF also serves both commercial as well as residential insulation market. The company has adopted new product launches as the key growth strategy over the years. BASF launched a new XPS Styrodur 3000 CS under the brand Styrodur, in January 2015. The wide range of brands and products and active operations make BASF a leading player in this market.

0 Comments

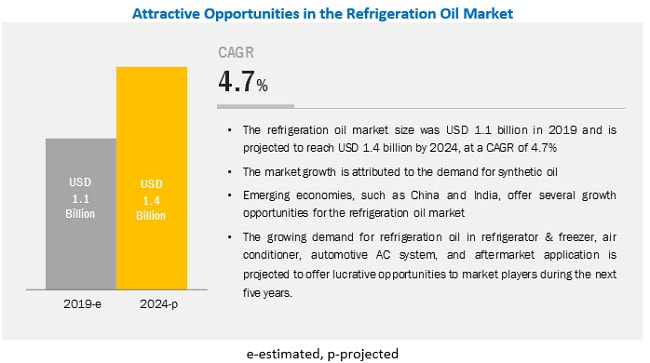

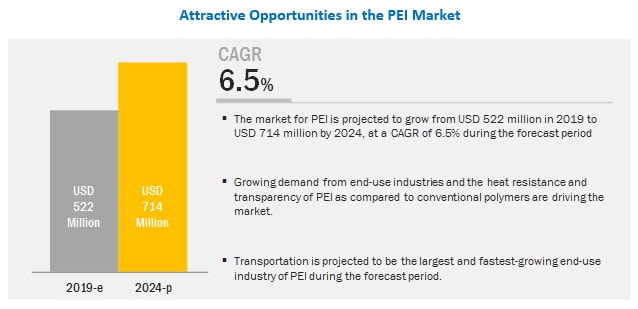

The refrigeration oil market size is projected to reach USD 1.4 billion by 2024 from USD 1.1 billion in 2019, at a CAGR of 4.7%. The growth of the market is driven by the increasing demand for consumer appliances, growing demand from food & pharmaceutical industries, and rising demand for low GWP refrigerants. Also, increasing consumption of packaged food products is expected to drive the refrigeration oil market. APAC is the key market for refrigeration oil, globally, followed by North America and Europe.

Download the PDF Brochure for more insight @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=126068118 Emerging economies are witnessing rapid urbanization along with a rise in disposable income. The consequent increase in the standard of living and growing consumption of convenience/packaged food products, coupled with the mass adoption of vaccines and drugs will drive the demand for refrigerators, freezers, air conditioners, and automobile HVAC systems. This will fuel the demand for refrigeration oil, ultimately driving the refrigerator oil market. Refrigerator & freezer application is estimated to be the largest segment of the natural fragrance market during the forecast period. The refrigerator & freezer application is estimated to be the largest segment of the refrigeration oil market, in terms of value, during the forecast period. The growth of this segment can be attributed to the rising demand for packaged food items and the changing lifestyle of people in developed and developing regions. Recent Developments

The presence of various refrigeration oil players, such as JXTG Group (Japan), Idemitsu Kosan Co., Ltd. (Japan), China Petrochemical Corporation (Sinopec Group) (China), Indian Oil Corporation Ltd. (India), and PETRONAS (Malaysia)., have a positive impact on the market. In addition, growth in refrigerator & freezer, air conditioner, automotive AC systems, and aftermarket sales in the region is increasing the demand for refrigeration oil. The key market players profiled in the report include JXTG Group (Japan), BASF (Germany), Idemitsu Kosan Co. (Japan), Royal Dutch Shell (Netherlands), ExxonMobil (US), BP (UK), PETRONAS (Malaysia), Chevron (US), Total (France), Sinopec Group (China), FUCHS (Germany), and Johnson Controls (Ireland). Don’t miss out on business opportunities in Refrigeration Oil Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  LTCC Market and HTCC Market is expected to grow from USD 916 million in 2019 to USD 1.1 billion by 2024, at a CAGR of 4.5% during the forecast period. The market is witnessing significant growth because of the growing demand from various end-use industries such as aerospace & defense, automotive, and telecommunications. Co-fired ceramic has good mechanical properties, such as excellent physical, chemical inactivity, hermicity, and high thermal stability properties.

Download the PDF Brochure for more insight @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=126252032 LTCC process type is the fastest-growing segment in the overall market. Co-fired ceramic is available in two process types, namely, LTCC (Low-Temperature Co-Fired Ceramic), and HTCC (High-Temperature Co-Fired Ceramic). LTCC process type is expected to register the highest CAGR during the forecast period as it is used in various applications such as high radio frequency, wireless devices, antennas, and radar. Glass-ceramic material type is the fastest-growing segment in the overall market. Co-fired ceramic is available in two material types, namely, glass-ceramic and ceramic. Glass-ceramic material is expected to register the highest CAGR during the forecast period as it can use noble metals such as gold, silver, and platinum for metallization on its layer. Some of the key players in the LTCC market and HTCC market are KYOCERA Corporation (Japan), DowDuPont Inc. (US), Murata Manufacturing Co., Ltd. (Japan), KOA Corporation (Japan), Hitachi Metals, Ltd. (Japan), Yokowo Co., Ltd. (Japan), NGK SPARK PLUG CO., LTD. (Japan), MARUWA Co., Ltd. (Japan), Micro Systems Technologies (Switzerland), TDK Corporation (Japan), and NIKKO COMPANY (Japan). The key strategies adopted by the major players for enhancing their business revenue are new product developments, partnerships, and acquisition. Key Questions Addressed by the Report

The natural fragrances market is projected to reach USD 4.3 billion by 2024, at a CAGR of 9.6% from USD 2.7 billion in 2019.

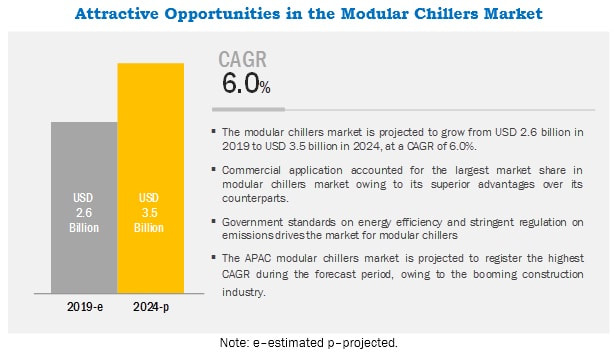

Rising demand for natural products and increased use of natural fragrances in various applications such as fine fragrances, personal care & cosmetics, and household care, are expected to drive the natural fragrances market. Additionally, rapid urbanization and industrialization in countries such as China, Japan, Brazil, and Argentina will increase the demand for various end-use products such as fine fragrances, personal care & cosmetics, and household care. This factor is estimated to drive the natural fragrance market. Download the PDF Brochure for more insight:https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=254324409 Based on the ingredient, the natural fragrance market has been segmented into essential oils and natural extracts. The essential oils natural fragrance ingredient is estimated to lead the natural fragrance market in terms of value. The awareness about health hazards due to the use of synthetic products has increased, hence creating a surge in demand for natural & organic products. Thereby, it increases the need for essentials oils and natural extracts. Europe is expected to account for the largest share of the natural fragrance market during the forecast period. Europe is expected to account for the largest market share in natural fragrance during the forecast period, in terms of value. The presence of various natural fragrance players, such as Givaudan SA (Switzerland), Firmenich SA (Switzerland), Symrise AG (Germany), Mane SA (France), Robertet SA (France), CPL Aromas (UK), Iberchem (Spain), and Dauper (Spain)., has a positive impact the market. In addition, growth in fine fragrances, personal care & cosmetics, and household care applications in the region is increasing the demand for natural fragrances. Key Market Players The key market players profiled in the report include as Givaudan SA (Switzerland), Firmenich SA (Switzerland), International Flavors & Fragrances (US), Symrise AG (Germany), Takasago International Corporation (Japan), Mane SA (France), Robertet SA (France), Sensient Technologies Corporation (US), T. Hasegawa Co., Ltd. (Japan), Bell Flavors & Fragrances (US). Givaudan (Switzerland) is developing its mold release agents business by launching new products, expanding its R&D capabilities, and by acquiring smaller companies. Givaudan acquired Albert Vieille, a French company specialized in natural ingredients used in the fragrance and aromatherapy markets. It will help the company cater to the growing demand of customers for natural fragrances. It also acquired Centroflora’s Nutrition Division (Centroflora Nutra) (Brazil), a manufacturer of botanical extracts and dehydrated fruits for the food, beverage, and consumer goods sectors. The acquisition will help the company strengthen its global offering of natural extract and increase its presence in Brazil.  The modular chillers market is projected to grow from USD 2.6 billion in 2019 to USD 3.5 billion by 2024, at a CAGR of 6.0% during the forecast period. The growth of the modular chillers can be attributed to the stringent government regulations on energy efficiency and emissions, globally. In addition, the competitive advantages of modular chillers over its substitutes has increased its demand in the HVAC and refrigeration systems.

Competitive advantages as compared to other alternatives, drives the demand for modular chillers in the commercial application. Modular chillers have a compact design, which is ideal for buildings where space is limited. It has control systems, which can be operated from remote places. Also, the biggest advantage of modular chillers is ‘modularity’, which means, operators can shut down any unit when cooling requirements are low and switch on any number of units when the requirement is high. Therefore, the modular chiller operators, can reduce the downtime to zero hours, as it is highly unlikely that all modules malfunction. In addition, modular chillers offers superior expandability, when operators plan infrastructure expansion. The modular chiller system capacity can be increased by adding parallel modules with the currently installed chiller system. These overall advantages of modular chillers have increased their demand. Download the PDF Brochure for more insights:https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=75609903 Recent Developments

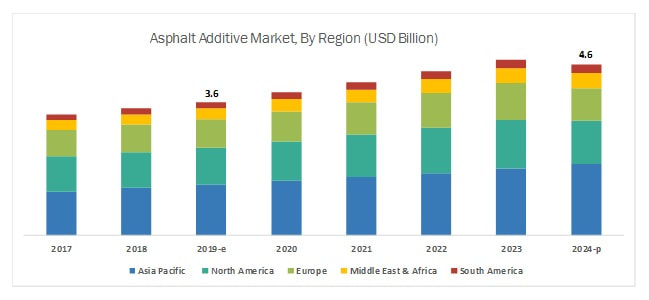

Carrier Corporation (US), McQuay Air-Conditioning (Hong Kong), Johnson Controls- Hitachi Air Conditioning (Japan), Midea Group (China), Ingersoll Rand (Ireland), Gree Electric Appliances (China), Frigel Firenze (Italy), Mitsubishi Electric Corporation (Japan), Multistack (US), and Haier Group (China) are the key players operating in the modular chillers market. These companies have adopted various organic as well as inorganic growth strategies between 2015 and 2019 to strengthen their positions in the market. Acquisition is the key growth strategy adopted by these leading players to enhance regional presence and product portfolios to meet the growing demand for modular chillers from emerging economies.  The asphalt additive market is projected to grow from USD 3.6 billion in 2019 to USD 6.3 billion by 2029, at a CAGR of 5.7% from 2019 to 2029. Increasing developments in the Asia Pacific infrastructure market, recyclability of asphalt, development of warm-mix asphalt, and increasing use of the material in roofing applications is driving the growth of the market across the globe.

Download the PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=156734514 Asphalt is a composite material used for the construction of pavements, roads, airport runways, parking lots, and bridges. Environmental damage, high load traffic, and use of low-quality construction materials lead to the deterioration of asphalt, which needs to be modified to reduce wear & tear. Asphalt additives help in improving the performance, durability, and service life of the asphalt. They also enhance the sustainability of tires, increase the braking efficiency of vehicles, and help reduce the stripping, rutting, and cracking of asphalt. Based on type, the rejuvenators segment is expected to grow at the highest CAGR during the forecast period, in terms of value. Increasing use of recycled materials, such as Reclaimed Asphalt Pavement (RAP) and Recycled Asphalt Shingles (RAS) in the asphalt pavements application, has resulted in the growing demand for rejuvenator asphalt additives to restore the strength and durability of aged binders. Rejuvenators are being widely used to improve properties, such as viscosity, of aging binders. The growth of this segment is due to the increased use of recycled road material for pavement application globally. Based on technology, the warm mix technology of the global asphalt additive market is expected to grow at the highest CAGR from 2019 to 2029, in terms of value. The demand from warm mix technology segment is rising due to various properties that have made it more attractive than other asphalt mixes. Less energy is needed to heat the asphalt mix, and less fuel is required to produce warm-mix asphalt. Also, it is environment-friendly as it produces fewer emissions, thus improving the working conditions at asphalt pavement sites. These properties will further increase its market share in the technology sector. To speak to our analyst for a discussion on the above findings, click Speak to Analyst Asia Pacific, North America, and Europe are significant regional markets for asphalt additive market. Growth in the infrastructure sector of emerging economies is driving the demand for new road pavements, and consequently, the demand for asphalt additives. Various leading manufacturers of asphalt additive have adopted the strategies of expansions, new product developments, acquisitions, and collaborations to cater to the increased demand for asphalt additive from various end-use industries.  The market size of waste heat recovery system (WHRS) was USD 44.14 Billion in 2015, and is projected to reach USD 65.87 Billion by 2021, at a CAGR of 6.90%. Rising energy & electricity prices coupled with stringent government regulations & incentives are expected to drive the market in the future.

Petroleum refining WHRSs are widely used in petroleum refining processes such as distillation (fractionation), thermal cracking, catalytic, and treatment. The thermal effectiveness of these energy-intensive processes is crucial to the petroleum refining industry and, hence, highly energy efficient WHRS are used for such applications. Many exothermic reactions occur in the refineries that also produce waste heat. Some modern refineries have highly integrated systems that recover heat from one process to use in other processes. However, still many refineries and their operations release high-temperature waste heat, but lack efficient WHRS to recover it for different applications. The growing oil & gas industries in the Asia-Pacific region, and increasing oil production in the Middle East & Africa is driving the demand of WHRS in petroleum refining industry globally. Chemical WHRS have been successfully used in the chemical industry for processes such as industrial gases, alkalis and chlorine, cyclic crudes, and intermediates, including ethylene, propylene, benzene/toluene, plastics materials, synthetic rubber, synthetic organic fibers, and agricultural chemicals. High efficiency, operational productivity, and utilization of specialized and customized equipment have made WHRS an important component in chemical production processes. Therefore, growth in the chemical industry is one of the driving factors of the global WHRS market. Metal Production Heavy metals manufacturing and refining involves many high-temperature processes from which waste heat can be recovered. Heavy metal foundries commonly recover clean gaseous streams. However, recovering waste heat from heavily contaminated exhaust gas sources such as coke ovens, blast furnaces, basic oxygen furnaces, and electric arc furnaces continue to present a challenge for economical functioning of WHRS. Other sources of waste heat include melting furnace exhaust, ladle preheating, core baking, pouring, shot blasting, castings cooling, heat treating, and quenching. The heat recovered from these sources is used in steam and electricity generation in and is further used as fuel in other processes. This helps the low revenue generating metal industry to boost its energy efficiency, and hence reduce operating costs. The demand of WHRS is increasing in metal production segment, as the metal industry is growing heavily in all the regions. Download the PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=202657867 The major restraints of the market are slow growth of the construction sector in Europe and high cost of these systems. Companies are focusing on various strategies to strengthen their market position such as supply contracts, agreements, and partnerships & collaborations. Supply contract is the most preferred strategy adopted by the key market players to sustain in this highly competitive market. The emerging technologies provide high growth opportunities to WHR system manufacturers. Increase in energy requirements in emerging economies such as China, India, and Brazil also plays an important role in fueling the demand. Some of the important manufacturers are ABB Ltd. (Switzerland), Amec Foster Wheeler (U.K.), Ormat Technologies Inc. (U.S.), General Electric Co. (U.S.), Mitsubishi Heavy Industries Ltd. (Japan), Echogen Power Systems Inc. (U.S.), Econotherm Ltd. (U.K.), Thermax Limited (India), Siemens AG (Germany), and Cool Energy Inc. (Colorado). Companies in this market compete with each other with respect to prices and product offerings to meet the market requirements.  The Bioplastics & Biopolymers market is projected to grow from USD 6.95 billion in 2018 to USD 14.92 billion by 2023, at a CAGR of 16.5% from 2018 to 2023. Increasing demand for bioplastics from the packaging industry, favorable government policies, increase in waste management regulations in Europe, and increasing concern for human health are projected to drive the bioplastics & biopolymers market. Increase in regulations is expected to propel the growth rate of the market.

Download the PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=88795240 Packaging is the largest end-use industry for bioplastics & biopolymers. The need for sustainable solutions has encompassed several industry verticals, including food & beverage. In addition, enhanced industrial & manufacturing technologies have enabled the food & beverage companies to incorporate bioplastics in packaging. The demand for packaging made from bioplastics for wrapping organic food as well as for premium and branded products is on the rise. Preference for packaging materials made from natural or organic polymers, derived from biomass sources, such as fats, oils, starch, and microbiota, is driving the market in the packaging end-use industry. Packaging Packaging protects goods during distribution, transportation, storage, and use. It is indispensable for preserving and moving goods, which cater to various sectors such as retail, institutional, and industrial. Change in the lifestyle of consumers has triggered the importance of polymer and use of packaging products, as they provide protection and containment. The packaging industry uses different materials such as glass, metals, wood, and polymers for packaging different types of products. Plastic constitutes 40.0% of the packaging materials. Properties of plastics such as high durability, plasticity, and impermeability to water have encouraged their use. However, increasing environmental regulations have restrained the use of conventional polymers, especially carry bags and packages, which is driving the demand for bioplastics & biopolymers. Packaging applications of bioplastics & biopolymers include food packaging, pharmaceutical packaging, cosmetics packaging, and shopping bags. Procter & Gamble and Johnson & Johnson use bio-PE for packaging various kinds of cosmetic products. PLA is widely used owing to its high recyclability. The increasing demand for eco-friendly packaging made from bio-based polymers is driving the demand for products such as PLA, PHA, and starch-based polymers in different applications. Consumer goods Bioplastics & biopolymers have a wide variety of applications in consumer products and can be used in casings, circuit boards, touchscreen computer casings, loudspeakers, keyboard elements, mobile casings, vacuum cleaners, and mouse for laptops. SUPLA has developed optimized PLA for the electronics industry. Similarly, the world’s first bioplastic touchscreen computer was developed in collaboration with a Taiwanese OEM/ODM, Kuender. The PLA blends used in the monitor screens also bring improved impact resistance; excellent high gloss finish; and stable and precise processing. Europe is the largest bioplastics & biopolymers market and is one of the major producers of plastics. It leads in the packaging end-use industry, which dominates the bioplastics & biopolymers market. These factors have been responsible for the development of bio-based plastics with collaborative research, which, in turn, is expected to transform Europe’s plastics industry. The political and economic conditions have also driven the market penetration of bioplastics & biopolymers. The EU Commission has focused on the Lead Markets Initiative, where bioplastics have been identified as one of the most important potential markets. Europe has, thus, become one of the major consumers of bioplastics & biopolymers. Key players profiled in this report include NatureWorks (US), Braskem (Brazil), Novamont (Italy), BASF (Germany), Total Corbion PLA (Netherlands), Biome Bioplastics (UK), Bio-On (Italy), Toray Industries (Japan), Plantic Technologies (Australia), and Mitsubishi Chemical Corporation (Japan).  Globally, the chlor-alkali market is one of the largest chemical industries, in terms of both value and volume. The major chlor-alkali products are chlorine, caustic soda, and soda ash.

Caustic soda has a wide range of applications in different end-use industries such as alumina refining, organic & inorganic chemicals, soaps & detergents, water treatment, and food and pulp & paper. Major challenges for the global caustic soda manufacturers include the high-energy costs and stringent environmental regulations. In India, there are high input costs, which make the local industry less competitive. However, there have been changes in the policies and it is expected that there will be positive outcome for the local caustic soda industry of India. The improving manufacturing industry globally will help increase the caustic soda demand in chemical and alumina applications. Soaps and detergents application, especially in India will drive the caustic soda market in the region. The global market size of chlor-alkali is estimated to reach USD 102.60 Billion by 2021 and is projected to register a CAGR of 5.4%. The applications for caustic soda are alumina, inorganic chemicals, organic chemicals, food and pulp & paper, soaps & detergents, textiles, water treatment, and steel/metallurgy-sintering. Download the PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=708 Asia-Pacific is the largest chlor-alkali market, globally. The region accounts for a major share of the chlor-alkali market and is the largest producer of chlor-alkali, globally. China is the largest and fastest-growing chlor-alkali market in the region. With the continuous increase in capacity of chlor-alkali, the country has an upper hand, as the manufacturing costs in the country for chlor-alkali are low. India is another high growth market for chlor-alkali in the region; the country is expected to be a driving factor for the industry in the region. Stringent environmental regulations for mercury emissions have forced the producers to shift to diaphragm and membrane cell technologies. There is an oversupply of caustic soda in the market due to the electro chemical unit ratio. Solvay S.A. has a global footprint with a wide product portfolio and diverse revenue stream. The demand from the Asia-Pacific market has provided an opportunity for the company to cater to the needs of the region. The volatile exchange rates are affecting the financial situation of the organization. The company’s strong R&D laboratories help it to stay a step ahead of its competitors. It is focused on sustainable development, innovation, and operating excellence. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed