MarketsandMarkets projects that the perlite market size will grow from USD 1.51 Billion in 2017 to USD 2.20 Billion by 2022, at an estimated CAGR of 7.78%. The perlite market is expected to witness high growth as a result of the rapid urbanization, large-scale investments in the building & construction sector, and the rising number of construction activities in emerging economies.

Download the PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=219145595 The Perlite market is segmented by type in to Expanded Perlite and Crude Perlite. Expanded perlite finds application in several sectors, which drives its demand. This segment dominates the perlite market and is projected to grow at a higher rate during the forecast period. Expanded perlite possesses high insulation, acoustic, and excellent water retention, and higher water density properties. Hence, the expanded perlite form accounted for a relatively larger market share than the crude perlite segment. Expanded perlite finds diverse applications in the industrial sector, ranging from high-performance fillers for plastics to cement; as a filtering agent for petroleum, water, and geothermal wells; and for cryogenic insulation that requires insulation for extremely low to medium and high temperature including insulating concrete, refractory bricks, and underfloor insulation. Safety certifications from regulatory authorities present opportunities for manufacturers to strengthen their position in the perlite market, in order to maintain the quality and performance standards of perlite. Target audience

0 Comments

The electronics industry segment of the persulfates market is projected to grow at the highest CAGR9/24/2019  The market size for persulfates is estimated to grow from USD 549.4 Million in 2017 to USD 727.8 Million by 2022, at a CAGR of 5.8% from 2017 to 2022. The growth can be attributed to the increased demand for persulfates from various end-use industries, such as polymers, cosmetics & personal care, electronics, and pulp, paper & textiles.

Increasing demand for persulfates from the electronics industry is expected to boost the persulfate market in this segment. Persulfates are used as cleaning agents and etchants in the printed circuit board manufacturing. With the increasing demand for printed circuit boards, the consumption of persulfates in the electronics industry is projected to grow at the highest rate during the forecast period, in terms of value. Download the PDF to know more @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=59168451 Key Target Audience:

This research categorizes the persulfates market on the basis of type, end-use industry, and region. Persulfates Market, By Type:

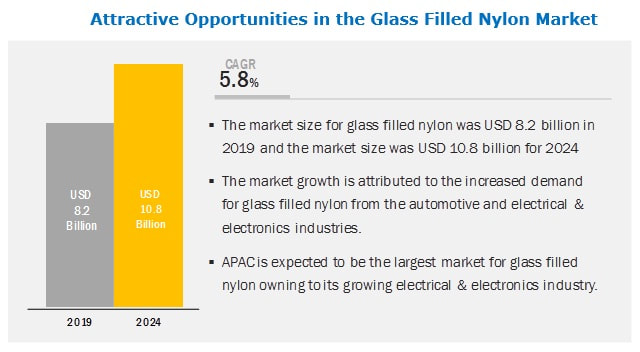

Key companies profiled in this research report on the persulfates market include PeoxyChem (US), United Initiators (Germany), Mitsubishi Gas Chemical Company (Japan), Ak-Kim Kimya (Turkey), and Fujian Zhanhua Chemical Company (China). Glass Filled Nylon Market | Nylon 6 market | Industry Analysis and Market Forecast to 20239/23/2019  The use of glass filled nylon is increasing due to its superior properties such as high strength, long durability, dimensional stability, stiffness, strength, chemical resistance, and creep resistance. The glass filled nylon market size is estimated to grow from USD 8.2 billion in 2019 to USD 10.8 billion by 2024, at a CAGR of 5.8% between 2019 and 2024. The increasing use of glass filled nylon in the automotive and electrical & electronics industries is bolstering the market, globally.

Download the PDF Brochure for more insights @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=25070558 The glass filled nylon market, by end-use industry, is segmented into automotive, electrical & electronics, industrial, and others including aerospace, construction, and marine. The market in the automotive end-use industry is projected to register the highest CAGR, in terms of value, during the forecast period. Automotive is the largest end-use industry segment of the glass filled nylon market, followed by the electrical & electronics end-use industry. The growing usage of glass filled nylon is these end-use industries is bolstering the market. The glass filled nylon market, by type, is segmented into polyamide 6, polyamide 66, and others including polyamide 11, polyamide 12, and other specialty polyamides. Polyamide 6 is the most widely used glass filled nylon due to its easy availability and low price. It also offers superior properties such as excellent tensile strength, high mechanical strength, and chemical resistance, which make polyamide 6 the widely glass filled nylon in the automotive and electrical & electronics end-use industries. The glass filled nylon market, by manufacturing process, is segmented into injection molding and extrusion molding. Injection molding is the most widely used process for the manufacturing of glass filled nylon. The ease of manufacturing glass filled nylon through this process is one of the major factors attributed to the high market size during the forecast period. By region, the glass filled nylon market is segmented into five regions, namely, North America, APAC, Europe, the MEA, and Latin America. APAC is expected to record the highest growth rate, in terms of value and volume, during the forecast period. The growth of end-use industries such as automotive, electrical & electronics, and industrial in the key countries of APAC such as China, India, and Japan is expected to drive the demand for glass filled nylon in the next five years. The key market players have realized the immense potential offered by the region for the growth of the glass filled nylon market. For instance, Asahi Kasei Corporation acquired Sage Automotive Interiors, Inc. This acquisition is a forward integration which will be beneficial for the growth of the glass filled nylon market, as automotive is the major end-use industry of glass filled nylon.  Steel rebar or reinforcement bars are used to strengthen the ability of concrete to resist tension in construction. The steel rebar market is expected to reach USD 154.08 billion by 2021, at a CAGR of 5.0% from 2016 to 2021. Growth in this market is mainly attributed to the increasing demand for steel rebar for the infrastructure, housing, and industrial segments across the globe.

Download the PDF for more insight @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=176200687 On the basis of end user, the steel rebar market has been classified into infrastructure, housing, and industrial segments. The infrastructure segment of the steel rebar market includes highways, dams, bridges, and roads, among others. The housing segment includes real estate, hospitals, schools, and petrol pumps among others, while the industrial segment consists of projects for energy & power, oil & gas, and telecommunications. In terms of value, the infrastructure segment is expected to be the fastest-growing segment in this market during forecast period. This growth is mainly attributed to the significant use of steel rebar in applications such as bridges, roads, dams, and highways, among others. On the basis of process, the steel rebar market has been classified into basic oxygen steelmaking, and electric arc furnace. The basic oxygen steelmaking process is the fastest-growing segment in this market, which is used across different regions, and is used in more than 70% of the global crude steel production. On the basis of type, the steel rebar market has been segmented into deformed, and mild steel. The market for deformed is the fastest-growing, owing to the deformation property on the bar surface which helps in increasing the bond between materials and minimizes slippage in concrete. Mild steel bars have a plain surface and round sections of diameter from six to 50 mm. The mild steel rebar is commonly used as a tensioning device in reinforced masonry structures and reinforced concrete that hold the concrete in compression. The Asia-Pacific steel rebar market is expected to grow at the highest CAGR between 2016 and 2021. The Asia-Pacific steel rebar market includes countries such as China, Japan, India, and South Korea. The market in this region is witnessing increased consumption of steel rebar in the construction industry. China is estimated to be the major producer of steel rebar in 2016. Rapidly growing household incomes in the Asia-Pacific, along with the growing middle class population is expected to fuel the growth of various end-use industries utilizing steel rebar in the Asia-Pacific region. The steel rebar market is highly fragmented and competitive and has a large number of prominent players. Key manufacturers in the steel rebar market are mainly located in the Asia-Pacific and Europe with some presence in North America, and the Middle East & Africa. The U.S. is the largest market in the North American region. Increasing investments on the infrastructure and housing segments is driving the steel rebar market in the region.  The global iodine market is estimated at USD 832.1 Million in 2017 and is projected to reach USD 1,041.0 Million by 2022, at a CAGR of 4.58%.

Download the PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=65097087 The market is witnessing growth due to the increasing use of iodine in optical polarizing films in LCD applications. Growing deficiency of iodine in developing countries and use in applications such as X-ray contrast media, fluorinated derivatives, and photography are some of the factors driving the market for iodine. “Caliche ore: The largest source of iodine” Caliche ore was the largest source for iodine extraction in 2016. The large share of caliche ore is because mining of iodine from caliche ore is less cumbersome and less capital intensive in comparison to its extraction from underground brines and seaweeds. Furthermore, the iodine mined from caliche ore contains more concentration (ppm) of iodine as compared to other extraction sources. “X-ray contrast media: The largest application of iodine” X-ray contrast media was the largest segment of the iodine market, by application in 2016. The high consumption of iodine in X-ray contrast media is attributed to the rising aging population and their susceptibility to various diseases which is expected to increase the use of X-ray contrast media in diagnostic imaging, thereby, driving the market for iodine in this application. “Western Europe: The largest iodine market, by region” The Western European region was the largest market for iodine, in terms of value and volume, in 2016. The high consumption of iodine in the region is attributed to the increasing demand from the healthcare and chemical industries. Growing investments in medical research, advancements in diagnostic imaging techniques, strong healthcare infrastructure with significant number of CT and MRI examinations, and growing iodine deficiency in Rest of the Western European counties are some of the factors responsible for the large market size of iodine in Western Europe. Sociedad Química y Minera (Chile), Iofina (UK), ISE Chemicals Corporation (Japan), IOCHEM Corporation (US), Compañía de Salitre y Yodo (Chile), and Algorta Norte SA (Chile) lead the global iodine market. These players are the major manufacturers of iodine and are gaining a strong foothold in the market through their strategies of capacity expansions.  The monochloroacetic acid (MCA) market is projected to reach USD 908.9 million by 2022, at a CAGR of 3.6% between 2017 and 2022. Asia Pacific is expected to be the largest market for MCA and is also projected to witness the highest growth during the forecast period. The growth of the market in this region can be attributed to rising population, growing urbanization, increasing demand from the building & construction industry, growing disposable income, and changing lifestyle in emerging countries of the region. These factors are expected to attract multinational companies to invest more in Asia Pacific countries like India and China.

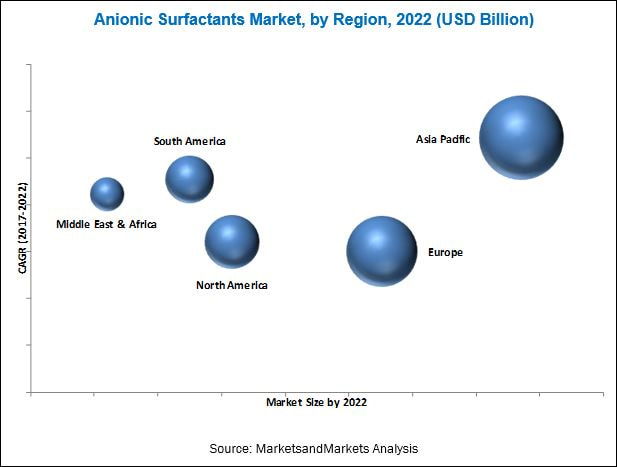

Download the PDF Brochure at https://www.marketsandmarkets.com/requestsampleNew.asp?id=120010112 The MCA market is expected to witness high growth in emerging economies, such as China, India, and Indonesia. Factors such as increasing disposable income and changing lifestyles of the middle-class population in these countries are expected to fuel the demand for personal care products, textiles, detergents, crop protection chemicals, and medicines. The growth of these industries propels the consumption of carboxymethylcellulose (CMC), which consequently drives the demand for MCA in the aforementioned economies. Additionally, the growth of the building & construction industry drives the consumption of CMC and thioglycolic acid (TGA), which, in turn, drives the demand for MCA in the Asia Pacific region. Based on product form, the liquid segment is projected to register the highest growth rate. The high growth in the use of liquid MCA is due to its easy miscibility as an intermediate, and efficient operation. Increased R&D activities to develop new and innovative products for use across a wide range of application areas are expected to boost the growth of the MCA market during the forecast period. The surfactants segment is projected to be the fastest-growing application segment between 2017 and 2022. Surfactant-based face wash, gel, and hair cream, among other personal care products, are replacing conventional products, owing to their cleansing ability, ease of usage, and customization. The increasing use of MCA in the manufacturing of amphoteric surfactants, such as betaines and imidazolines, is expected to boost the surfactant market during the forecast period. Increasing adoption of surfactants in the cosmetic industry in developing countries, such as India, China, Indonesia, and Brazil, is expected to drive the demand for MCA in this application. Increasing disposable income and changing lifestyles of consumers are key growth drivers for the surfactants market in emerging countries.  The global anionic surfactants market is estimated at USD 16.36 billion in 2017 and is projected to reach USD 20.10 billion by 2022 at a CAGR of 4.2%. The market is mostly driven by the growing number of applications in home care, personal care, oil & gas, and construction industries. Factors such as technological advances, increasing working population, rising incomes, and changing consumer preferences are driving the anionic surfactants market. The demand for anionic surfactants is growing as they provide multifunctional properties to various personal care products such as skin creams, sunscreens, anti-aging creams, anti-acne creams, hair conditioners, and hair shampoos, among others. The growing awareness among consumers regarding the availability of products with multifunctional properties and rising concern for personal hygiene are also driving the demand in the home care segment. Download the PDF Brochure for more insight @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=239519688 The anionic surfactants market, on the basis of type, has been classified into linear alkylbenzene sulfonate (LAS), lignosulfonates, alcohol ether sulfates/fatty alcohol sulfates (AES/FAS), alkyl sulfates/ether sulfates, sarcosinates, alpha olefin sulfonates (AOS), phosphate esters, and alkyl naphthalene sulfonates, among others. Lignosulfonates is expected to be the fastest-growing type segment during the forecast period. Lignosulfonates are water-soluble anionic surfactants used in applications in industries such as construction, oil & gas, etc. They are the by-products obtained from the production of wood pulp using sulfite pulping. Typical application areas of lignosulfonates are concrete additives, crop protection, pigment dispersion, fertilizers, and leather tanning, among others. The construction application segment of the anionic surfactants market is expected to witness the highest growth during the forecast period. The anionic surfactants market in the construction industry is witnessing high growth in various regions such as the Middle East and Asia Pacific, especially in countries such as China, India, the UAE, and Saudi Arabia, among others. These factors, along with the upcoming infrastructure projects in the energy and manufacturing sectors in Saudi Arabia, are expected to drive the market in the region. Asia Pacific is expected to be the fastest-growing market for anionic surfactants. Rapid industrialization, coupled with the growing personal care and home care industries, is expected to drive the market in the region. Rising disposable incomes of consumers and changing lifestyles play a significant role in boosting the demand for anionic surfactants. In Asia Pacific, China is the largest market for anionic surfactants owing to its rapidly growing home care and personal care industries. Improved lifestyles, increasing standards of living, increasing population, and high economic growth of the emerging countries such as China, South Korea, India, and Indonesia have made Asia Pacific an attractive market for personal care and home care products. The increasing population and availability of affordable products are primarily responsible for the high demand for personal care ingredients in the region.  The glass flake coatings market is projected to reach USD 1.80 billion by 2022, at a CAGR of 4.48% from 2017 to 2022. Asia Pacific is estimated to lead the market for glass flake coatings in 2017, in terms of value, due to the increased demand for glass flake coatings from countries such as China, South Korea, Japan, India, and Indonesia.

Download the PDF brochure for more insight @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=8719963 The presence of key players of glass flake coatings in the Asia Pacific region is one of the main factors driving the growth of the market in this region. Key players in the market, such as Chugoku Marine (Japan), KCC Corporation (South Korea), Nippon Paint (Japan), and Kansai Paint (Japan), have their manufacturing bases in Asia Pacific. Other top companies operating in the global glass flake coatings market are also shifting their production bases to Asia Pacific, owing to the low cost of production and ease of serving emerging local markets. The glass flake coatings in the marine industry will be dominated by Asia Pacific, particularly China, South Korea, and Japan, due to the presence of major shipbuilding companies in these countries. The rapid developments in glass flake coating technology in India, Indonesia, and Australia, is another reason expected to fuel the growth of the Asia Pacific glass flake coatings market. Based on resin, the epoxy segment is expected to witness the highest growth during the forecast period. The growth of this segment can be attributed to the increasing use of epoxy-based glass flake coatings in the building of marine offshore & onshore infrastructures, large cargo ships, interior & exterior of storage tanks, and various chemical processing areas. Epoxy glass flake coatings impart excellent corrosion, abrasion, chemical, and temperature resistance to oil, gas, solvents, and chemical & petrochemical products. Based on substrate, the steel segment is projected to witness the highest growth during the forecast period. Steel meets the strength and toughness criteria required for the manufacture of pipes for the oil & gas; tanks for the chemical & petrochemical; and various parts of cargo ships for the marine end-use industries. The use of glass flake coatings protects steel from corrosion, fouling, and abrasion. Based on end-use industry, the marine segment is projected to witness the highest growth during the forecast period. This is due to increase in use of glass flake coatings to protect cargo ships and various onshore & offshore infrastructures from harsh weather conditions. Glass flake coatings are also vital in enhancing the fuel efficiency of a ship and decreasing the impact on the environment.  The global propylene glycol market was valued at USD 3.47 Billion in 2016, and is projected to grow at a CAGR of 5.8% from 2016 to 2021, to reach USD 4.60 Billion by 2021. Eco-friendly production process of bio-based propylene glycol has led to the growth of the global propylene glycol market. Also, the growing automotive industry in Asia-Pacific is driving the market as propylene glycol is widely used in engine coolants and sheet molding compounds among others.

Download the PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=264488864 In terms of end-use industry, the market is classified into transportation, building & construction, pharmaceuticals & cosmetics, food & beverage, and others. Transportation is expected to be the fastest-growing end-use industry Transportation is projected to be the fastest-growing end-use industry of the global propylene glycol market during the forecast period, mainly due the rising demand for propylene glycol in the automotive coolants, aircraft wings, pleasure boats, and ships. This industry in the Asia-Pacific region is anticipated to grow at the highest CAGR during the forecast year. The growth is attributed to increasing sales of automobiles in the region. In addition, improving standards of living and increasing disposable income in emerging countries such as India, China, and South Korea are driving the growth of the transportation industry. Also, China, Korea, Japan, and India are witnessing high demand for new ships for both military and commercial purposes. On the basis of region, the market is segmented into Asia-Pacific, Europe, North America, Middle East & Africa, and South America. Currently, the Asia-Pacific region is the largest market for propylene glycol. Rapid industrialization and improved living standards is expected to drive the increasing demand for propylene glycol. The region is also projected to be the fastest-growing market from 2016 to 2021. This growth is attributed to the rapidly growing transportation industry in the region. Some of the key players in the global propylene glycol market are The Dow Chemical Company (U.S.), LyondellBasell Industries N.V. (Netherlands), BASF SE (Germany), Archer Daniels Midland Company (U.S.), Global Bio-chem Technology Group Co., Ltd. (China), DuPont Tate & Lyle Bio Products Company, LLC (U.S.), Huntsman Corporation (U.S.), SKC Co., Ltd. (South Korea), Temix International S.R.L. (Italy), and Ineos Oxide (Switzerland) among others. To speak to our analyst for a discussion on the above findings, click Speak to Analyst |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed