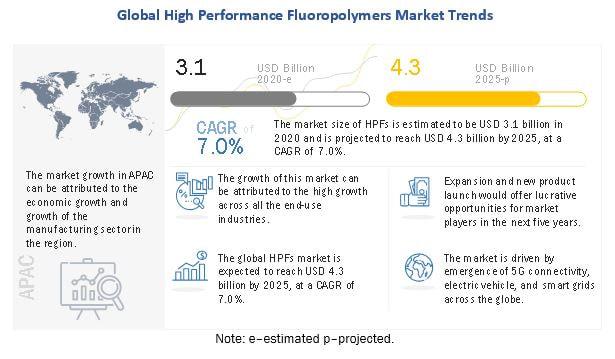

The global high performance fluoropolymers (HPF) market size is estimated to be USD 3.1 billion in 2020 and is projected to reach USD 4.3 billion by 2025, at a CAGR of 7.0%, between 2020 and 2025. HPF is used mainly in industrial processing, transportation, electrical & electronics, and medical, among others. It is used for manufacturing various products such as coatings, films, membranes, tubes, wire & cable, seals, gaskets, liner, mechanical parts, and many others in these industries. High chemical & temperature resistance, excellent dielectric properties, and lightweight are some of the characteristics owing to which the demand for high performance fluoropolymers is high in industrial processing segment.

The key players in the HPF market are The Chemours Company (US), Daikin Industries, Ltd. (Japan), 3M (US), Solvay SA (Belgium), AGC (Japan), The Dongyue Group (China), Gujrat Fluorochemicals Ltd. (India), Halopolymer OJSC (Russia), and Hubei Everflon polymer (China). Expansion is the key growth strategy adopted by key HPF manufacturers. Apart from this, acquisition and new product launch are other strategies adopted by manufacturers between 2015 and 2020. To know about the assumptions considered for the study download the pdf brochure AGC (Japan) was one of the key players in the HPF market in 2019. It is primarily engaged in the production and marketing of glass, electronic materials, chemicals, and ceramics globally. It has 210 subsidiaries and has a presence in 30 countries across APAC, Europe, North America, South America, and the Middle East & Africa. It has a strong foothold across the APAC region, contributing around 70% of the group’s revenue. The company has adopted organic growth strategies to increase its market share and revenue. For example, in February 2019, the company launched FEP high performance fluoropolymer under its brand AFLAS. This polymer is used majorly in automotive underhood component systems and can withstand an operating temperature of 392OF. The Chemours Company is one of the leading providers of performance chemicals. It is a pioneer in the fluoropolymers products and has renowned brands, namely, Teflon, Zonyl, and Tefzel, have acquired a significant share in the market. The company has been focusing on organic strategies to maintain its competitive position in the HPF market. In July 2016, the company opened a new Teflon finishes plant at Chemours’ Changshu Works site in Changshu (Jiangsu), China. This expansion was aimed at enhancing the production of various fluoroproducts to cater to the growing demand for HPF in Asia Pacific. Gujarat Fluorochemicals Limited (GFL) is a market leader in fluoropolymers, industrial gases, chemicals, energy, and entertainment. It was the fourth-largest producer of PTFE globally in 2019 and had sales & distribution network across 50 countries across the globe. The extensive geographical presence helped the company capture a significant market share and maintained its leadership in the high performance fluoropolymers market. It accounted for over 11% of the global fluoropolymer market share with the help of its worldwide presence and 20,000 tons of PTFE production capacity. Don’t miss out on business opportunities in High Performance Fluoropolymers Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 Comments

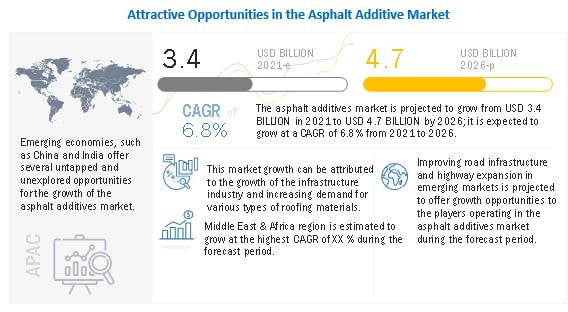

The asphalt additive market is projected to grow from USD 3.4 billion in 2021 to USD 4.7 billion by 2026, at a CAGR of 6.8% from 2021 to 2026. Increase in road construction projects along with the growing usage of asphalt additives in roofing application are some of the major key factors driving the growth of the asphalt additive market across the globe.

Nouryon (Netherlands), DowDuPont (US), Arkema SA (France), Honeywell International Inc. (US), Evonik Industries (Germany), Huntsman Corporation (US), Kraton Corporation (US), Ingevity Corporation(US), and BASF SE (Germany) are some of the leading players operating in the asphalt additive market. These players have adopted the strategies of expansions, new product developments, acquisitions, and collaboration to enhance their position in the market. To know about the assumptions considered for the study download the pdf brochure Kraton Corporation is a leading specialty chemical company that manufactures styrene block copolymers and other engineered polymers. In September 2016, Kraton Performance Polymer Inc. changed its name to Kraton Corporation. The company has operations in performance products, performance chemicals, specialty polymers, adhesives, cariflex, and tires. The company operates its business through two segments namely, Polymer and Chemical. Kraton Corporation provides asphalt additives under its polymer segment. It has a strong geographic reach across the Americas, Europe, the Middle East, Asia Pacific, and Africa with operations in over 70 countries worldwide. The company is focused towards inorganic development to enhance its market share. For instance, Kraton Polymers LLC acquired Arizona Chemical Holdings Corporation, having spent USD 1,370 million. This development helped the company diversify its product portfolio of engineered polymers and specialty chemicals and expand its adhesives, road construction, coatings, and oilfield chemical operations. Ingevity Corporation is a manufacturer of specialty chemicals and high-performance carbon materials. The specialty chemical products are used in a range of high performance applications, such as pavement technologies, oil field technologies, and industrial specialties. The company operates its business through two segments, namely, Performance Materials and Performance Chemicals. The performance materials segment offers automotive carbon products used in gasoline vapor emission control systems in cars, trucks, motorcycles, and boats. The performance chemicals segment provides products derived from pine chemicals used in asphalt paving, oilfield technologies, and other diverse industrial specialty applications, such as adhesives, agrochemical dispersants, publication inks, lubricants, and petroleum. The company has around 1,750 employees and has a presence in over 60 countries with nine manufacturing facilities across North America, South America, Europe, the Middle East & Africa, and Asia Pacific. The company focused towards organic business development strategy to enhance its customer base. For instance, in June 2019, Ingevity upgraded its manufacturing facility, which is located in DeRidder, LA facility to manufacture products that are used in a variety of applications, such as asphalt paving, oilfield drilling, lubricants, adhesives, inks, and coatings. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=156734514  Carbon capture, utilization, and storage (also referred to as CCUS) is a process that involves capturing carbon dioxide (CO2), transporting it through pipelines, ships, and other modes of transport and storing it under the Earth’s surface to prevent CO2 emissions. The stringent eco-friendly lawas emphasizing on curbing the CO2 emissions from industrial and power plants, is driving the growth of the market. The global carbon capture, utilization, and storage market size is expected to grow from USD 1.9 billion in 2021 to USD 4.1 billion by 2026, at a CAGR of 17.0% during the forecast period.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=151234843 Over the past years, companies have strengthened their position in the global carbon capture, utilization, and sstorage market by adopting expansions as a major strategy. From 2016 to 2021, the partnership was the key strategies adopted by the market players to maintain growth in the global carbon capture, utilization, and storage market. Royal Dutch Shell is an international energy company that specializes in the exploration, production, refining and marketing of oil and natural gas.

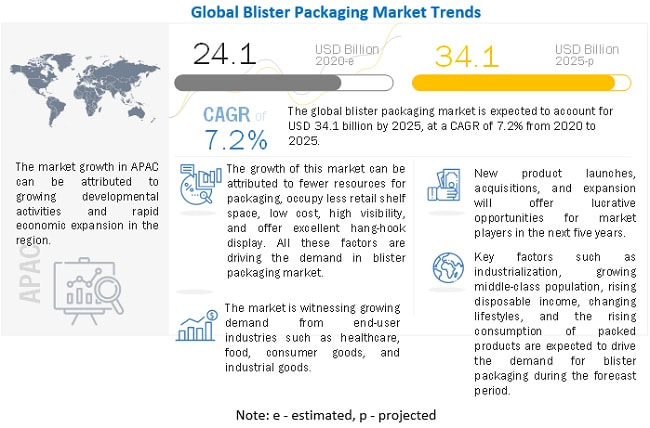

Don’t miss out on business opportunities in Carbon Capture, Utilization, and Storage Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The global blister packaging market size is estimated at USD 24.1 billion in 2020 and is projected to reach USD 34.1 billion by 2025, at a CAGR of 7.2%, between 2020 and 2025. Blister packaging is a transparent, portable packaging material, with a flat base and raised cover of plastic, which is tamper-evident and resistant to moisture, protecting the product from damage. The product to be packed is attached to the base substrate, which could be paperboard, rigid plastic, or aluminum foil. A molded, transparent plastic film is sealed to the base substrate through the heat-sealing process. The transparent plastic film offers high visibility of the product.

The key players in the blister packaging market are as Amcor Plc (Switzerland), DOW (US), WestRock Company (US), Sonoco Products Company (US), Constantia Flexibles (Austria), Klockner Pentaplast Group (Germany), E.I. du Pont de Nemours and Company (US), Honeywell International Inc. (US), Tekni-Plex (US), Display Pack (US). The blister packaging market report analyzes the key growth strategies adopted by the leading market players, between 2015 and 2020, which include expansions, merger & acquisition, new product developments, and collaborations. To know about the assumptions considered for the study download the pdf brochure Amcor Plc (Switzerland) was formerly known as Australian Paper Manufacturers (APM) and it changed its name to Amcor Plc in May 1986. Amcor Plc is a global packaging manufacturer that offers innovative packaging solutions. It offers plastic, packaging film, metal, and glass packaging for several industries such as beverage, food, medical, household, industrial goods, pharmaceuticals, and tobacco. Amcor Plc is currently focusing on reducing the packaging footprint by making the packaging lighter, increasing recycling of raw materials, developing efficient transport packaging and re-closable packaging, and creating packaging sustainable to heat treatment. The key strategy of Amcor Plc is the focus on geographic expansion through the acquisition of various packaging units in different regions for various segments such as food, beverages, and pharmaceutical. The company has operations in 43 countries in Europe, North America, and emerging countries such as India and China with more than 180 operating sites.

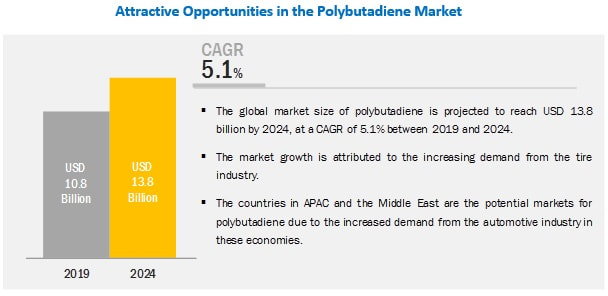

The global polybutadiene market is estimated to be valued at USD 10.8 billion in 2019 and is projected to reach USD 13.8 billion by 2024, at a CAGR of 5.1% during the forecast period. The demand for polybutadiene in the automotive industry for manufacturing tires is expected to be driven by the growing automotive sales, mainly in the Asian countries such as China and India. Emerging economies such as China, India, Indonesia, and Thailand are experiencing high demand for polybutadiene. Increasing disposable income, huge consumer base, rising urban population, low labour costs, and easy availability of raw materials are attracting global automobile manufacturers to shift their production facilities to the region, thus, creating a high demand for polybutadiene in this region. The key players of the polybutadiene market are ARLANXEO (Netherlands), JSR Corporation (Japan), UBE Industries Ltd. (Japan), SABIC (Saudi Arabia), LG Chem Ltd. (South Korea), Versalis SPA (Italy), PJSC SIBUR Holdings (Russia), Sinopec (China), and Kuraray Co. Ltd. (Japan). These companies adopted new product development, joint venture, and expansion as their major business strategies between January 2015 and August 2019 to earn a competitive advantage in the polybutadiene market. To know about the assumptions considered for the study download the pdf brochure ARLANXEO is one of the leading players in the polybutadiene market. The company has been focusing on expansion and collaboration strategies to maintain its leading position in the market. ARLANXEO is one of the world’s leading manufacturers in the polybutadiene market with a strong product portfolio and geographic presence across major regions. The company has established competitiveness through significant spending on R&D to develop new and advanced products in the market. Furthermore, the company is collaborating with other organizations to meet varied requirements of the customers. It has aggressive expansion plans to develop new products. It has established a strong reputation in the polybutadiene market. For example,

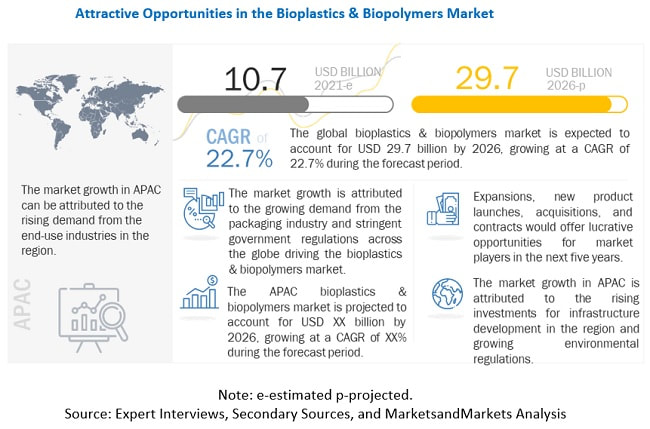

ARLANXEO offers polybutadiene products for various applications such as tires, golf ball, sports, band conveyor, belt conveyor, machine & equipment construction, rubber covered roll, seals, side wall, technical rubber goods, wiper, buffers, injection molding, shock absorber, and tubes. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=56692050 NatureWorks (US) and Braskem (Brazil) are Leading Players in the Bioplastics & Biopolymers Market8/22/2021  The global bioplastics & biopolymers market size is projected to reach USD 29.7 billion by 2026 growing at a CAGR of 22.7% from 2021 to 2026. The increasing demand for bioplastics & biopolymers material in various end-use segments coupled with stringent regulatory and sustainability mandates concerning healthcare safety is driving the market for bioplastics & biopolymers.

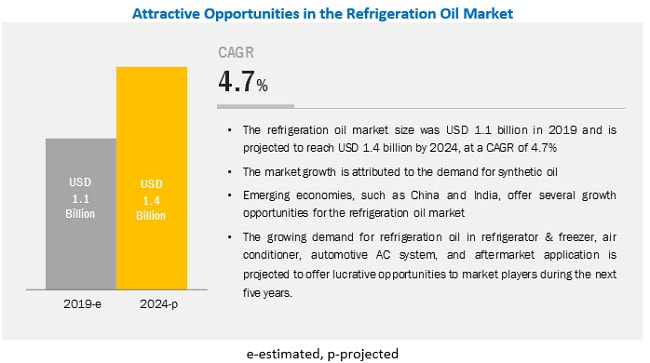

The increase in demand for bioplastics & biopolymers and the growing industrial development in the emerging economies, such as APAC and South America, are driving the market. The key players in this market are NatureWorks (US), Braskem (Brazil), BASF (Germany), Total Corbion (Netherlands), Novamont (Italy), Biome Bioplastics (UK), Mitsubishi Chemical Holding Corporation (Japan), Biotec (Germany), Toray Industries (Japan), and Plantic Technologies (Australia). These players have adopted various strategies such as investment & expansion, merger & acquisition, partnership & agreement, and new product launch in order to strengthen their market position. For instance, in April 2021, NatureWorks announced a new strategic partnership with IMA Coffee, which is a market leader in coffee handling processing and packaging. This partnership aims at increasing the market reach for high-performing compostable K-cup in North America. To know about the assumptions considered for the study download the pdf brochure NatureWorks is jointly owned by PTT Global Chemical (Thailand) and Cargill (US). It manufactures biopolymers derived from renewable resources, such as corn, starch, and vegetable oils. It is among the leading advanced material companies and offers a broad portfolio of renewably sourced polymers and chemicals for the packaging and chemical industries. The company offers Ingeo Biopolymer, which is used in 3D printing, beauty and household, building & construction, food & beverage packaging, medical & hygiene, and other applications. It also offers PLA-based biopolymer performance material designed for use in fresh food packaging and food service ware applications. NatureWorks operates in North America, Europe, and APAC, with manufacturing facilities in the US. In April 2021, NatureWorks announced a new strategic partnership with IMA Coffee, which is a market leader in coffee handling processing and packaging. This partnership aims at increasing the market reach for high-performing compostable K-cup in North America. Braskem was founded in 2002, with the consolidation of six companies, namely, Copene, OPP, Trikem, Proppet, Nitrocarbono, and Polialden. The company operates in the chemical and petrochemical industry and thus, plays an important role in other production chains that are essential to economic development. The company produces polyethylene (PE), polypropylene (PP) and polyvinylchloride (PVC) resins, in addition to basic chemical inputs such as ethylene, propylene, butadiene, benzene, toluene, chlorine, soda, and solvents, among others. The company offers bioplastics through its biopolymers segment. Braskem is the first company that started to produce on a world scale unit BIO- PE which is made out of sugarcane. The company produces 16 million metric tons per year of thermoplastic resins and other chemical products. It exports the products to clients in approximately 100 countries and operates 41 industrial units, which are located in Brazil, the US, Germany, and Mexico as well as 16 regional offices in other countries to provide integrated solutions for clients. the latter in partnership with the Mexican company, Idesa. In August 2019, Braskem and Ledesma (Argentina), manufacturer of natural agroindustrial products, have collaborated to deliver Ledesma + Bio, which is a line of 100% sustainable notebooks made entirely of sugarcane. Such initiatives are expected to cater to the needs of the bioplastics & biopolymers market. Don’t miss out on business opportunities in Bioplastics & Biopolymers Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The refrigeration oil market size is projected to reach USD 1.4 billion by 2026 from USD 1.1 billion in 2021, at a CAGR of 4.1%. Growing demand for frozen food and in the pharmaceutical industry is expected to support the growth of the refrigeration oil market. However, huge investment in R&D and strict rules to limit the use of fluorocarbon refrigerants is restraining the growth of the market. On the other hand, innovation in product development has created opportunities for manufacturers.

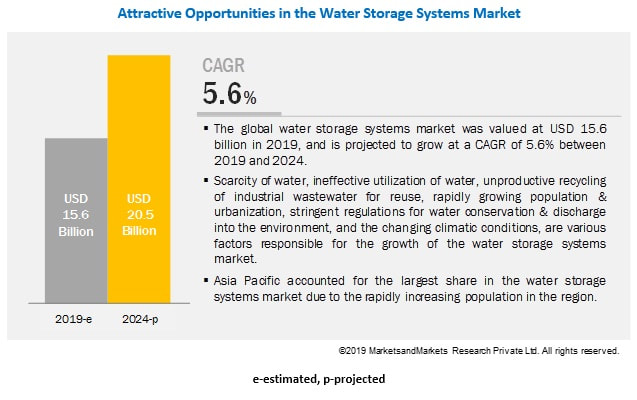

Eneos Holdings Inc. (Japan), BASF SE (Germany), Idemitsu Kosan Co. Ltd (Japan), ExxonMobil Corporation (U.S.), Royal Dutch Shell Plc. (Netherlands), Total Energies SE(France), China Petrochemical Corporation (Sinopec Corp), Petroliam Nasional Berhad(Petronas), FUCHS Petrolub SE (Germany), Johnson Controls(Ireland) are the major players in this market. To know about the assumptions considered for the study download the pdf brochure Eneos Holdings Inc. engages in the development, production, and sale of petroleum, natural gas, and metals. The company operates through four business segments, namely, Energy, Metals, Oil, Natural gas E&P, and Others. The company operates its refrigeration oil business in Japan, China, and other among other countries. On April 1, 2017, JX Group (Japan) and TonenGeneral Sekiyu K.K. Group (Japan) integrated their business and formed JXTG Holdings renamed as Eneos Holdings Inc. in June 2020. BASF SE is one of the largest chemical producers in the world. It engages in manufacturing and selling a wide range of chemicals and intermediate solutions. The company offers various products including chemicals, additives, plastics, functional solutions, performance products, agricultural solutions, and crude oil. It operates through seven different business segments namely: Chemicals, Industrial solutions, Nutrition & care, Materials, Surface technologies, Agricultural solutions and others. The company has a presence in more than 60 countries of Europe, North America, APAC, South America, and the Middle East & Africa In October 2020, BASF SE doubled the capacity of synthetic ester-based stocks in Jinshan, China which helps in production of refrigerant oils, lubricants and other oils and helps in boosting capacity of alkoxylate capacity Idemitsu Kosan Co., Ltd. is a petroleum refining and manufacturing company. The company manufactures and sells petrochemical and oil products. The company operates through its subsidiaries in APAC, Europe, North America, South America, and the Middle East & Africa In August 2020, Idemitsu Kosan Co. Ltd expanded their operations by constructing a new plant in Huizhou, China to increase supply capacity and establish supply of refrigerant oils and lubricants across China. Read More: https://www.marketsandmarkets.com/PressReleases/refrigeration-oil.asp  In terms of value, the global water storage systems market size is estimated to be USD 15.6 billion in 2019 and projected to reach USD 20.5 billion by 2024, growing at a CAGR of 5.6% from 2019 to 2024. Rapidly increasing population, water scarcity, ineffective water management, recycling of industrial wastewater, increasing urbanization, stringent regulation for conservation & consumption of water, and falling levels of rainfall are among major drivers for the growth of the water storage systems industry.

By region, the industry is segregated into Asia Pacific, the Middle East & Africa, North America, Europe, and South America. Among these, Asia Pacific is expected to lead the water storage systems market during the forecast period. This growth is attributed to the scarcity of water, ineffective utilization of water, inefficient recycling of industrial wastewater for reuse, rapidly growing population & urbanization, stringent regulation for water conservation & discharges into the environment, and falling levels of rain, among others. Major companies operating in the water storage systems market include CST Industries, Inc. (US) and McDermott International Inc. (US), Containment Solutions Inc., (US), DN Tanks (US), Caldwell Tanks (US), Balmoral Tanks Limited (UK), and Synalloy Corporation (US), among others. Moreover, these companies hold a potential share in the water storage systems industry. Recent Developments

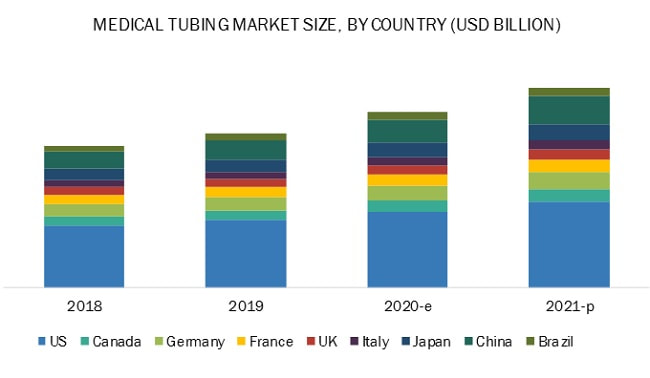

The US medical tubing market size is projected to reach USD 2.9 billion by 2021, at a CAGR of 13.2%.The increase in demand for medical tubes in ventilators is the key factor driving the use of medical tubing. The rising demand for medical devices that incorporate medical tubing and the growing demand for ventilators in this pandemic are propelling the growth of the medical tubing market globally. However, factors such as restricting counterfeit products and fighting time for supply chain and logistics could affect the market growth.

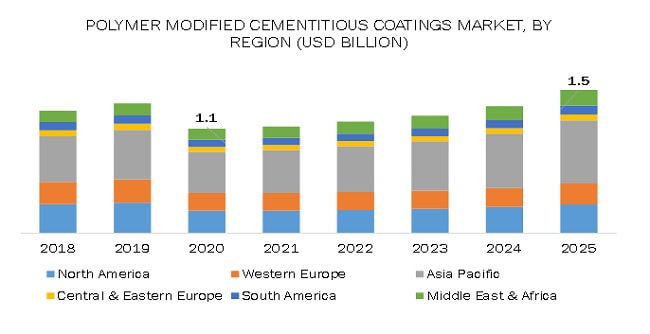

The US is projected to be the leading medical tubing market during the forecast period. The growth in the US can be attributed to the rising demand for medical tubing applications such as drug delivery, catheter & cannulas, bulk disposable tubing, and special application. The presence of a robust industrial base, favorable government policies, and large number of established players for medical tubing in the country are strengthening the medical tubing industry in the country. To know about the assumptions considered for the study download the pdf brochure Zeus Industrial Products (US), Saint Gobain Performance Plastics (France), Teleflex (US), Optinova (US), and Lubrizol Corporation (Vesta) (US), among others, are the leading medical tubing manufacturers, globally. These companies have established their brands, and medical tubing produced by these companies are consumed domestically. They are also supplied to various countries such as China, Japan, UK, Italy, France, and others within the Asia Pacific region. In February 2020, Teleflex Medical OEM acquired HPC Medical Products to strengthen its medical tubing & wire components and catheters portfolio. With this acquisition, the company is able to meet the growing demand in this pandemic situation. Now, the company is able to supply more products to the impacted countries with immediate effect to meet the growing demand. Lubrizol announced the continuous supply of flexible and biocompatible materials for vascular catheters, IV tube sets, and medical components used in ventilators, valves, and infusion pumps. In order to attain this, it has altered its production process to deliver more products which can serve the purpose during this COVID-19 pandemic. The company also ramped up the supply of ESTANE thermoplastic polyurethane (TPU) for a multitude of applications in this crucial time. Read More: https://www.marketsandmarkets.com/PressReleases/covid-19-impact-on-medical-tubing.asp  The polymer modified cementitious coatings market is estimated at USD 1.1 billion in 2020 and is projected to reach USD 1.5 billion by 2025, at a CAGR of 6.5% from 2020 to 2025. The residential segment is estimated to lead the polymer modified cementitious coatingsmarket in 2020, owing to The growing urbanization and migration of people from rural areas to urban cities are important factors driving the housing sector. Rising government initiatives to support infrastructure development and construction activities in emerging countries of the Asia Pacific region offer lucrative growth opportunities to manufacturers of polymer modified cementitious coatings. The recent outbreak of the COVID-19 pandemic and its rapid spread across the world has led to economic disruption and has brought down construction activities. Trade, travel, retail, and manufacturing activities have been affected, and the production of construction chemicals has come to a standstill during the first three months of 2020 and is expected to continue till the second quarter of 2020.

To know about the assumptions considered for the study download the pdf brochure Major companies such as Arkema S.A. (France), Sika AG (Switzerland), Akzo Nobel N.V. (Netherlands), MAPEI S.p.A. (Italy), Compagnie de Saint-Gobain S.A. (France), and Fosroc International Limited (UAE) , Dow, Inc. (US) and H.B. Fuller Company (US) The Lubrizol Corporation (US), Organik Kimya Sanayi Ve Ticaret A.S. (Turkey), Pidilite Industries Limited (India), GCP Applied Technologies Inc. (US), Berger Paints India Limited (India), W. R. Meadows, Inc. (US), Evercrete Corporation (US), Indulor Chemie GmbH (Germany), The Euclid Chemical Company (US) and others are key players in the polymer modified cementitious coatingsmarket. These players have been focusing on developmental strategies, such as expansions, acquisitions, partnerships, joint veture, and new product developments, which have helped them expand their businesses in untapped and potential markets. Recent Development

The polymer modified cementitious coatings market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific polymer modified cementitious coatings market in 2019. The Asia Pacific region is an emerging and lucrative market for polymer modified cementitious coatings, owing to industrial development and improving economic conditions. This region constitutes approximately 60% of the world’s population, and thus leads to the wide-scale use of polymer modified cementitious coatings for waterproofing applications in residential and non-residential buildings, and public infrastructure. Outbreak of COVID-19 from China and the impact of coronavirus in Japan, South Korea, Autralia, and India has caused a decrease in the consumption of polymer modified cementitious. Don’t miss out on business opportunities in Polymer Modified Cementitious Coatings Market. Speak to our analyst and gain crucial industry insights that will help your business grow. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed