The LTCC market and HTCC market size is estimated to be USD 916 million in 2019 and is projected to reach USD 1.1 billion by 2024, at a CAGR of 4.5% between 2019 and 2024. Owing to their superior performance properties such as chemical inactivity, hermicity, and high thermal stability over traditional circuit boards, namely printed circuit boards, co-fired ceramics are gaining increasing demand from various industries such as aerospace & defense, automotive, telecommunications, medical, and industrial.

The major co-fired ceramic manufacturers are KYOCERA Corporation (Japan), DowDuPont Inc. (US), Murata Manufacturing Co., Ltd. (Japan), KOA Corporation (Japan), Hitachi Metals, Ltd. (Japan), Yokowo Co., Ltd. (Japan), NGK SPARK PLUG CO., LTD. (Japan), MARUWA Co., Ltd. (Japan), Micro Systems Technologies (Switzerland), TDK Corporation (Japan), and NIKKO COMPANY (Japan). These players have adopted various growth strategies, such as new product development, partnership, and acquisition, to expand their presence in the market further. New product development was the most commonly adopted strategy by the major players from 2015 to 2018, which helped them to increase their product offerings and broaden their customer base. To know about the assumptions considered for the study download the pdf brochure KYOCERA Corporation (Japan) is a well-established company in the global LTCC market and HTCC market. The company offers a high-quality, co-fired ceramic product. It is continuously engaged in providing high-grade, co-fired ceramic products. As a part of its growth strategy, it is focused highly on new product development and partnership. For instance, in 2018, the company developed an ultra-small ceramic package using Low-Temperature Co-Fired Ceramic for the high-frequency antenna. Murata Manufacturing Co., Ltd. (Japan) is another major manufacturer of co-fired ceramics. It is one of the global leaders in the design, manufacture, and supply of advanced electronic material, leading-edge electronic components, and multi-functional, high-density modules. As a part of its growth strategy, the company strives to increase its profitability and provide quality products to long-term strategic customers. The company is an expert in creating innovative products and solutions for the electronics industry. It offers low-temperature co-fired ceramic multilayer substrates for the LTCC market and HTCC market. The product uses silver or copper for metallization path. It is also recognized as glass ceramics because of the mixture of glass with primary raw material, alumina. It caters to demand from automotive end-use industry. The product has applications in the anti-lock brake system, electronic stability control, electric power steering, and transmission control units. Related Reports: LTCC Market and HTCC Market by Process Type (LTCC, HTCC), Material Type (Glass-Ceramic, Ceramic), End-use Industry (Automotive, Telecommunications, Aerospace & Defense, Medical), Region (Asia Pacific, North America, Europe, MEA, LA) - Global Forecast to 2024

0 Comments

3M Company (US) and Nitto Denko Corporation (Japan) are the Key Players in the Splicing Tapes Market7/31/2019  The splicing tapes market size is projected to grow from USD 527 million in 2018 to USD 593 million by 2023, at a CAGR of 2.37% during the forecast period. The global paper & printing industry is undergoing a rapid transformation and plays a significant role in driving the splicing tapes market globally. Splicing tapes are used in the production of paper, films, label, and packaging products (such as corrugated boxes, paperboards, or envelopes). However, the environmental regulations related to the paper & pulp sector could act as a major constraint. The developed countries, in regions such as Europe and North America, are anticipated to cut back on the growth level in the near future, owing to the stagnant nature of their markets.

The key players of the market include tesa SE (Germany), 3M Company (US), Nitto Denko Corporation (Japan), Avery Dennison Corporation (US), Intertape Polymer Group, Inc. (Canada), Scapa Group PLC (UK), Shurtape Technologies, PLC (US), Echotape (US), and Adhesive Research, Inc. (US). New product launch has been the most dominating strategy adopted by major players between 2015 and 2018, which helped them broaden their customer base. To know about the assumptions considered for the study download the pdf brochure In-line with the rising demand for splicing tapes, tesa has been working to deliver efficient splicing tape products to various applications in the paper & printing industry. This company operates through business segments, namely, Direct Industries and Trade Markets. Direct Industries caters to various end-use industries such as automotive, electronics (mobile phones and laptops), paper & printing, and building & construction. The Trade Markets division is further divided into two segments, namely, General Industrial Markets (adhesive solutions for packaging, tapes required during transporting, assembling, and repairing products) and Consumer & Craftsmen (product solutions required for daily use in homes, offices, and crafts). The company launched a new product called tesa Easy Splice in Feb 2018 which is used in the paper & printing industry to increase output volume and reduce the change over time. Through the strategy of new product launch, the company is able to cater to the demands of a wide range of industries, especially from APAC. This will boost the growth of the company and, also, its splicing tapes business, globally. The second-most active company in the market is 3M Company. The company operates through five business segments, namely, industrial, safety & graphics, electronics & energy, health care, and consumer. It manufactures splicing tapes for varied applications through its electronics & energy segment. Its splicing tapes products in the paper & printings application have global brand recognition. The company has planned to adopt organic and inorganic strategies such as new product launch, investment & expansion, and merger & acquisition in the future which will surely increase its presence and revenue globally. Related Reports: Splicing Tapes Market by Resin (Acrylic, Rubber, Silicone), Backing Material (Paper/Tissue, Pet/Polyester, Non-Woven & Others), Application (Paper & Printing, Packaging, Electronics, Labeling), and Region - Forecast to 2023  The global top 10 plastics market is projected to reach USD 586.24 Billion by 2021, at a CAGR of 6.84%. By volume, the market is projected to reach 332.4 Million tons by 2021, at a CAGR of 4.68%.

Packaging is currently the largest application segment of the top 10 plastics market. Plastics provide a much cleaner, tougher, and aesthetically appealing form of packaging, especially for the food & beverage industry and the electronics industry. This is anticipated to fuel its demand in the packaging application segment. The extensive use of plastics in bags, pouches, and sachets as well as in conventional packaging methods is also expected to drive the growth of the packaging segment. Download PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=91494156 Key Target Audience:

The Asia-Pacific region led the global top 10 plastics market, in terms of both value and volume, in 2015. The growing construction sector, increasing R&D activities initiated by major players, easy availability of raw materials, and urbanization are among the key growth drivers for the top 10 plastics market in this region. The Dow Chemical Company (U.S.), ExxonMobil Chemical Company, Inc. (U.S.), and SABIC (Saudi Arabia) have led the global top 10 plastics market in the last five years. Diverse product portfolios, strategically positioned R&D centers, adoption of various development strategies, and technological advancements are some of the factors that helped strengthen the market position of these companies in the global top 10 plastics market. To speak to our analyst for a discussion on the above findings, click Speak to Analyst  Circuit Materials Market was valued USD 29.83 billion in 2017 and is projected to reach USD 36.85 billion by 2023, at a CAGR of 3.8% during the forecast period. The growing demand for circuit materials due to technological advancements in the electronics sector is projected to drive the market during the forecast period.

Ask for free sample report @https://www.marketsandmarkets.com/requestsampleNew.asp?id=128882477 Based on the substrate, the fiberglass-epoxy segment of the circuit materials market is projected to register the highest CAGR, in terms of value, during the forecast period Circuit materials, manufactured using the fiberglass-epoxy material, have superior mechanical and chemical properties. This raw material can provide a high strength-to-weight ratio. It also can withstand moisture and offers high resistance to fire. This factor is projected to drive the fiberglass-epoxy segment of the circuit materials market. The communications application segment is projected to account for the largest share, in terms of value, in the circuit materials market during the forecast period Circuit materials are increasingly being used in the communications application. In this application, the use of circuit materials is significant in various devices such as mobiles, telephones, and smart tablets. The communications application is projected to account for the largest share of the market between 2018 and 2023, in terms of value. The use of circuit materials has increased in the communications application, owing to the ability to provide enhanced conductivity on compact printed circuit boards of the various communication devices. Key players operating in the circuit materials market include Shengyi Technology (China), Kingboard Laminates (Hong Kong), ITEQ Corporation (Taiwan), DowDuPont (US), Jinan Guoji Technology (China), Eternal Materials (Taiwan), Rogers Corporation (US), Taiflex Scientific (Taiwan), Isola Group (US), and Nikkan Industries (Japan). To speak to our analyst for a discussion on the above findings, click Speak to Analyst  The global market size for blow molding resins is estimated at USD 36.67 Billion in 2017, and is projected to reach USD 51.95 Billion by 2022, at a CAGR of 7.2% between 2017 and 2022. Expansions, acquisitions, and new product developments are the key strategies adopted by the major players to strengthen their footholds in the global blow molding resins market.

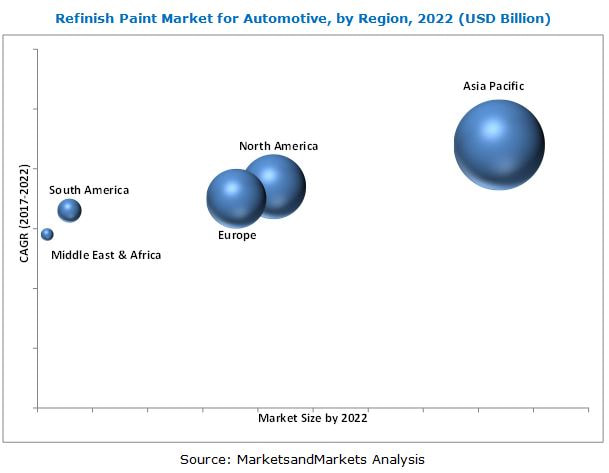

North America, followed by the Asia Pacific, and Middle East & Africa witnessed the maximum number of strategic developments undertaken by various players between 2012 and 2017. Download the PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=8448983 Exxon Mobil (US), LyondellBasell (Netherlands), DowDuPont (US), SABIC (Saudi Arabia), INEOS (Switzerland), Solvay (Belgium), Formosa Plastics (Taiwan), Chevron (US), Eastman (US), China Petroleum (China), and Reliance Industries (India) are the leading blow molding resins manufacturers globally. DowDuPont (US) is one of the leading players in the blow molding resins market. It is a US-based chemical company formed by the merger of Dow Chemical and DuPont in August 2017. The company has been focusing on new product launches and expansions to maintain its leading position in the market. For instance, in October 2016, E. I. du Pont (US) launched polyamide (PA66 and PA6) and glass-filled blow molding resins used for applications in the automotive industry. Also, in November 2014, Dow (US) expanded the production of polyethylene by revamping its production technology in Argentina. It revamped its four production units for Low Density Polyethylene (LDPE). LyondellBasell (Netherlands) and Exxon Mobil (US) are other major players in the blow molding resins market. The company adopted the acquisitions strategy to establish its foothold in the Asia Pacific. For instance, in April 2016, the company acquired polypropylene compounder, Zylog Plastalloys Pvt. Ltd in India. In October 2017, Exxon Mobil (US) started commissioning of the polyethylene production facility in Texas, US. This expansion is expected to increase capacity by 65% or 650,000 tons, which is expected to lead to a new production capacity of 2.5 million tons. The company is focusing on the production of high-performance polyethylene through this expansion. The company has commissioned blow molding resins production facilities closest to its upstream projects to have easy access to raw materials. This has enabled it to produce the resins at low cost. Related Reports: Blow Molding Resins Market by Type (Polyethylene, Polypropylene, Polyvinyl Chloride, Polyvinyl Terephthalate), Application (Packaging, Automotive & Transportation, Construction & Infrastructure), and Region – Global Forecast to 2022  Automotive refinish paint covers all the repainting of vehicles for repair, protection, and decorative purpose. Refinish paint is often carried out after a vehicle is involved in a collision and requires body repair. It is also carried out after a certain period when the vehicle needs to be refurbished to ensure protection from corrosion. Most of the refinish paint are of solventborne, waterborne, and powder technology. These coatings use different resins, including polyurethane, epoxy, acrylic, and others. Different layers of refinish paint are clearcoat, basecoat, primer, and sealer.

Download the PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=9257396 Key players operating in the refinish paint for automotive market have adopted various strategies to strengthen their position in the market. Mergers & acquisition was the key strategy adopted by the leading market players to achieve growth in the refinish paint for automotive market between 2014 and 2017. Key players in the market also adopted strategies, such as new product launches to increase their shares in the refinish paint for automotive market and strengthen their distribution networks. Axalta (US), PPG Industries (US), BASF (Germany), Sherwin-Williams (US), Kansai Paint (Japan), Nippon Paint (Japan), KCC Corporation (Korea), and AkzoNobel (Netherlands) are some of the leading players in the refinish paint for automotive market. Axalta (US) is one of the leading companies in the refinish paint for automotive market. The company offers refinish paint for various layers such as clearcoat, basecoat, primer, and sealer. The company has acquired High Performance Coatings (HIPIC) (Malaysia), and Metalak Benelux (Netherlands) to strengthen its market and enhance its technology portfolio. Similarly, in 2017, PPG Industries (US) acquired Futian Xinshi (China). The acquisition enhances PPG’s position in the growing Chinese refinish paint for automotive market. Futian Xinshi has proven its growth and profitability by leveraging well-positioned brands, mature technology, low-cost operations, and a solid-performing distribution base. Related Reports: Refinish Paint Market by Layer (Clearcoat, Basecoat, Primer, & Sealer), Resin (PU, Epoxy, & Acrylic), Technology (Waterborne, Solventborne & Powder), Vehicle (Passenger Cars, Commercial Vehicles), and Region – Global Forecast to 2022 Pultrusion is a process of manufacturing structural composites parts using polymer matrix and fibers. Properties of products manufactured through pultrusion are good strength, good chemical resistance, non-magnetic, low maintenance and very low thermal expansion.

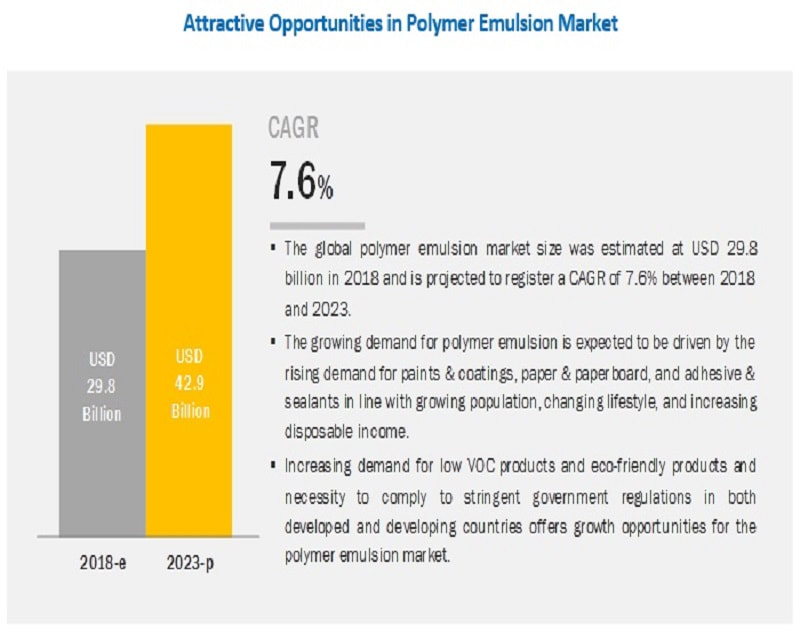

Download PDF Sample @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=220841043 The pultruded parts have applications in construction industry where different pultruded parts are used in form of gratings, rebars and customized profiles. Pultruded products provide manufacturers and designers with the benefits of high strength-to-weight ratios, corrosion resistance, heat resistance, dielectric properties, and dimensional stability. FRP pultrusions are cost effective and versatile alternative to traditional materials, such as steel, aluminum and timber. FRP pultrusions weigh 75% less than steel and are non-corrosive. FRP rebar has also been applied to various aspects of chemical anti-corrosion, and it replaces carbon steel, stainless steel, wood, and non-ferrous metals. Moreover, pultruded structural components used in the cooling towers produce an engineered framework of high quality, reliability and safety. Industrial applications are expected to drive the pultrusion market in next five years due to increase in demand of pultruded parts in cooling towers, offshore oil drilling projects and civil engineering. . Currently, the global pultrusion market is dominated by various market players, such as Exel Composites (Finland), Strongwell Corp. (U.S.), Bedford Plastics (U.S.), Creative Pultrusion (U.S.) and Glasfroms Inc (U.S). The report “Pultrusion Market by type (Glass Fiber, Carbon Fiber and others), by Resin Type (Polyester, Vinyl Ester, Polyurethane and Others) by Application (Industrial, Housing, Civil Engineering, Consumers and others) and by Region — Global Trends and Forecasts to 2020”, The pultrusion end market in terms of value is expected to reach around USD 2,045.2 Million by 2020, at a CAGR of 4.8% between 2015 and 2020. Apart from the market segmentation, this report also makes use of the Porter’s Five Forces Analysis, which provides an in-depth analysis of the market providing a detailed process flow diagram and market dynamics, such as drivers, restraints, and opportunities in the global pultrusion market. Expansion was the Key Strategy Adopted by the Leading Players of the Polymer Emulsion Market7/24/2019  The polymer emulsion market size is expected to grow from USD 29.8 billion in 2018 to USD 42.9 billion by 2023, at a CAGR of 7.6%. The global polymer emulsion market is expected to be driven by growing end-use industries such as automotive & transportation and building & construction, especially in the emerging economies. Stringent governmental regulations such as REACH Europe and the Clean Air Act as well as growing awareness towards green building are also driving the polymer emulsion market.

The polymer emulsion market’s competitiveness is continuously increasing with growing demand from various end-use industries. Major polymer emulsion players have adopted various strategies to capture market share and retain their position in the market. DIC Corporation (Japan), DowDuPont (US), BASF SE (Germany), Arkema Group (France), Celanese Corporation (US), Trinseo (US), The Lubrizol Corporation (US), Wacker Chemie AG (Germany), Synthomer Plc (UK), and Omnova Solutions Inc. (US) are the key players in the polymer emulsions market. To know about the assumptions considered for the study download the pdf brochure DowDuPont (US) is the largest player in the market. In May 2018, The Dow Chemical Company, subsidiary of DowDuPont, opened a new Eastern Canada Regional Sales Center in Toronto. The center will serve as a strategic commercial hub for Dow and will increase collaboration and address the needs of Canadian customers. Furthermore, in May 2017, the company signed two agreements to advance Dow’s strategic innovation agenda in the Kingdom of Saudi Arabia. The company will construct a state-of-the-art manufacturing facility to manufacture a range of water-treatment and coatings products. The new facility will serve the country’s need with an innovative range of acrylic-based polymers for architectural and industrial coatings as well as detergent and water-treatment applications. BASF SE (Germany) is the second-largest player in the market. The company produces a broad range of polymer emulsion for different applications. In March 2018, the company expanded its production facility of Joncryl water-based emulsions at its Ludwigshafen site. This will strengthen the company’s position as a leading manufacturer of water-based resin and emulsion which are used in overprint varnishes, printing inks, as well as functional coatings for flexible packaging and paper & board applications. This is one of the major expansion strategies adopted by the player in the market. Celanese Corporation (US) maintains its key position by adopting expansion as a strategy in the polymer emulsion market. In September 2016, the company started production at its newest VAE production unit in Jurong Island, Singapore. This will meet the growing demand for eco-friendly materials in the Southeast Asia region and will support the company’s strategy to add production facilities close to its customer base. In the same year, the company expanded its vinyl acetate/ethylene emulsion product portfolio with the addition of Celvolit 149HV at its Nanjing, China plant. This positioned the company to deliver greater value in adhesive applications to their customers. To speak to our analyst for a discussion on the above findings, click Speak to Analyst  The plumbing fixtures & fittings market is projected to reach USD 139.4 Billion by 2027. The plumbing fixtures & fittings market size is estimated to grow from USD 86.5 billion in 2018 to USD 139.4 billion by 2027. Factors such as increasing demand in Asia-Pacific due to rapid urbanization, building renovations due to disasters and upgradations, rising construction activities in emerging economies, and large-scale investment in industrial and infrastructure sectors are some of the drivers for the growth of the plumbing fixtures & fittings market.

Download the PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=77394490 Residential buildings to gain maximum traction during the forecast period The residential buildings segment dominated the market in 2018 and is projected to be the fastest-growing end-user industry in the next five years, as a result of the rising urbanization and changing lifestyle inclined toward new designs and better technology in homes. The residential market is projected to grow at the highest rate due to the rise in new and existing housing completions. Furthermore, the non-residential segment is projected to be the second fastest-growing end-use industry due to the rising demand from commercial buildings such as hotels, gyms, and spa resorts. Plastics as a raw material to play a key role in the plumbing fixtures & fittings market The report defines and segments the plumbing fixtures & fittings market on the basis of raw material into vitreous china, metal, and plastics. The vitreous china segment is projected to contribute the largest market share as it is the most economical material for domestic fixtures such as toilet bowls, urinals, and washbasins. Plastic plumbing fixtures & fittings, made from a wide range of polymers such as fiberglass, cast polymer, and acrylic, is projected to grow at the highest rate from 2018 to 2027. Asia-Pacific is projected to have the largest market share and dominate the plumbing fixtures & fittings market from 2016 to 2021. Asia-Pacific offers potential growth opportunities; developing countries such as China and India are projected to be emerging markets, making the Asia-Pacific region the fastest-growing market for plumbing fixtures & fittings. The growth of the plumbing fixtures & fittings market in this region is driven by factors such as the growth in the construction of the residential and non-residential buildings. Also, the growing population and economic development are other factors driving the growth of this market. Factors such as fluctuations in raw material prices act as a restraint for the growth of the market. The global market for plumbing fixtures & fittings is dominated by players such as Geberit AG (Switzerland), Kohler Co. (U.S.), Jacuzzi Inc. (U.S.), Masco Corporation (U.S.), LIXIL Group Corporation (Japan), Fortune Brands Home & Security, Inc. (U.S.), TOTO Ltd. (Japan), and Roca Sanitario, S.A. (Spain). Other players in the market are Elkay Manufacturing Company (U.S.) and MAAX Bath Inc. (Canada). These players adopted various strategies such as new product developments, acquisitions, agreements, partnerships, and expansions to cater to the needs of the plumbing fixtures & fittings market. To speak to our analyst for a discussion on the above findings, click Speak to Analyst BASF (Germany) and Songwon (South Korea) ara the Major Players in the Plastic Antioxidants Market7/23/2019  The plastic antioxidants market is expected to grow at a CAGR of 4.5% from 2017 to 2022, in terms of value. Asia-Pacific was the largest market for plastic antioxidants in 2016. The growing demand for plastics in countries, such as China, Japan, South Korea, and India from the packaging, building & construction, medical, and automotive industries is expected to fuel the growth of plastic antioxidants in the region. The market is evolving with major players playing a crucial role in the development of the new and advanced products. Key players in the market include BASF (Germany), Songwon (South Korea), and ADEKA (Japan).

Download PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=106598592 Players in the plastic antioxidants market are mainly concentrating on expansions, agreements, new product launches, and acquisitions to meet the growing demand from various end-use industries. Expansions help the companies to meet the growing demand for plastic antioxidants in regions such as Asia-Pacific and South America. BASF, Songwon, and ADEKA Corporation have a major share in the plastic antioxidants market. BASF is focused on expansions to meet the growing demand in the market. In March 2017, the company announced plans to build a new plastic additives plant in Shanghai, China to increase the production of antioxidants and associated blends. The expansion helped the company to meet the growing demand for plastic antioxidants in Asia-Pacific. In 2016, the company announced its plans to invest more than USD 212.1 million to increase the capacity of its global plastic additives production network and meet the growing demand for antioxidants and light stabilizers. Songwon is focused on new product launches and agreements to meet the growing demand for plastic antioxidants. In August 2017, the company launched nonylated diphenylamine antioxidants SONGNOX L670 and liquid phenolic antioxidants SONGNOX L135. In February 2017, Songwon signed an agreement with Biesterfeld, a leading distributor of plastics and specialty chemicals in Turkey for the distribution of Songwon’s comprehensive range of polymer stabilizers for the automotive, packaging, appliance, and coatings industries in Turkey. ADEKA focuses on expansions to strengthen its market position in the plastic antioxidants market. In August 2016, the company established a new subsidiary, ADEKA Fine Chemical (Zhejiang) Co., Ltd. in China to manufacture and sell polymer additives. Related Reports: Plastic Antioxidants Market by Polymer Resin (Polyethylene, Polypropylene, Polyvinyl Chloride, Polystyrene, Acrylonitrile Butadiene Styrene), Antioxidants Type (Phenolic, Phosphite & Phosphonite, Antioxidant Blends) – Global Forecast to 2022 Request new version @https://www.marketsandmarkets.com/RequestNewVersion.asp?id=106598592 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed