The MCA market is estimated at USD 762.6 Million in 2017 and is projected to reach USD 908.9 Million by 2022, at a CAGR of 3.6% during the forecast period. Leading market players, such as AkzoNobel (Netherlands), CABB (Germany), and Niacet (US), have adopted several strategies, such as joint venture and acquisition, to efficiently serve customers and increase their market shares.

Joint venture was the key growth strategy adopted by the major players in the MCA market. This strategy accounted for a share of 66.7% of the total growth strategies adopted by the major market players between 2014 and 2017. These players have also adopted acquisition as the second level growth strategy to expand their regional presence. This strategy accounted for a share of 33.3% of the total growth strategies adopted by the players between 2014 and 2017. To know about the assumptions considered for the study, download the pdf brochure AkzoNobel (Netherlands), the largest manufacturer of MCA, adopted joint venture as its primary growth strategy. For instance, in April 2016, AkzoNobel entered into a joint venture with Atul Chemicals (India) to set up an MCA production plant at Atul’s existing business unit in Gujarat, India. The 50-50 joint venture project is expected to start in the first quarter of 2019. From an initial annual capacity of 32,000 tons, the plant has been intended for future expansion of 60,000 tons per year. The joint venture project will utilize chlorine and hydrogen manufactured by Atul and AkzoNobel’s cutting-edge eco-friendly hydrogenation technology to produce MCA. Along with meeting Atul’s MCA requirement, the proposed facility will also serve the MCA market in India. CABB (Germany), ranked as the second largest manufacturer of MCA, has also adopted joint venture as its key growth strategy to strengthen its foothold in the global market. For instance, in April 2016, CABB entered into a joint venture with Jining Gold Power (China) to produce MCA in China. This joint venture was worth USD 16.6 million. The plant, which utilizes the latest German hydrogenation technology, would initially be producing about 25 kilotons per year of MCA flakes. It will also start the production of MCA in the liquid form at a later date. Currently, half of the global MCA demand is from China, with the demand growing at an above-average rate. Therefore, this local production plant will also leverage benchmarks in quality, safety, and sustainability. Related Reports: Monochloroacetic Acid Market by Product Form (Crystalline, Liquid, And Flakes), Application (CMC, Agrochemicals, Surfactants, TGA), and Region (North America, APAC, Europe, Middle East & Africa, and South America) – Global Forecast to 2022

0 Comments

The glass flake coatings market is projected to reach USD 1.80 Billion by 2022, at a CAGR of 4.48% from 2017 to 2022. Glass flake coatings are manufactured by adding glass flakes in anti-corrosive coatings to improve barrier and reinforcement properties, along with wear & tear and abrasion resistance properties. Glass flake coatings are best used in the oil & gas, marine, chemical & petrochemical, water & wastewater systems, power plants, and pulp & paper end-use industries to protect steel and concrete substrates from corrosive fluids and impart resistance against solvents, chemicals, and high-temperature fluids.

To know about the assumptions considered for the study, download the pdf brochure Investments & expansions, new product developments/launches, and mergers & acquisitions were the key strategies adopted by industry players to achieve growth in the glass flake coatings market. Companies are focusing on investments & expansions to expand their businesses and fulfill the growing demand for glass flake coatings from consumers. Besides these strategies, companies are also adopting new product launches and mergers & acquisitions to expand and cater to the rising demand for glass flake coatings from emerging economies. In terms of strategic developments between January 2015 and September 2017, investments & expansions was the most preferred strategy adopted by manufacturers to strengthen their position and product portfolio in the global glass flake coatings market, followed by new product developments/launches and mergers & acquisitions. Chugoku Marine (Japan), KCC Corporation (South Korea), Nippon Paint (Japan), and Kansai Paint (Japan) are some of the key players in the Asia Pacific glass flake coating market. Akzo Nobel (Netherlands), Jotun (Norway), and Hempel (Denmark) are key players in the European region, while PPG Industries (US), The Sherwin-Williams Company (US), and RPM International (US) are key players in the North American region. Key manufacturers including Akzo Nobel (Netherlands), PPG Industries (US), Jotun (Norway), Hempel (Denmark), Chugoku Marine (Japan), The Sherwin-Williams Company (US), KCC Corporation (South Korea), Nippon Paint (Japan), Kansai Paint (Japan), and RPM International (US) have been profiled in this report. Akzo Nobel, PPG Industries, and Jotun were the most active players in the global glass flake coatings market between January 2015 and September 2017. For instance, in May 2017, Akzo Nobel opened a Performance Coatings production facility in Santo André, Brazil. With this development, the company will become more agile in responding to local customer needs and regional market demands. The company will also strengthen its international portfolio of high-performance industrial and marine coatings in South America. PPG Industries is another key manufacturer of glass flake coatings. In February 2016, the company invested USD 7.8 million in its Coatings Innovation Center in Allison Park, Pennsylvania (US). With this investment the company enhanced all three main business segments, namely performance coatings, industrial coatings, and glass coatings. Glass flake coatings are manufactured under its performance coatings business segment. In November 2015, Jotun opened a new marine and protective coating plant in Brazil with a production capacity of 10 million liters per annum. The new plant will help the company become a market leader in marine and protective coatings within Brazil.  The microporous insulation market size is projected to grow from USD 132 million in 2018 to USD 165 million by 2023, at a compound annual growth rate (CAGR) of 4.7%, during the forecast period. The major driving factors in the microporous insulation market are high thermal resistance of microporous insulation material and increasing demand from various applications, such as industrial, oil & gas, energy & power, and automotive.

The major players in the microporous insulation market include Promat International N.V. (Belgium), Morgan Advanced Materials plc (UK), Isoleika S. Coop. (Spain), Unicorn Insulations Ltd. (China), Guangzhou Huineng Environmental Protection Materials Co., Ltd. (SILTHERM) (China), Johns Manville (US), NICHIAS Corporation (Japan), ThermoDyne (US), Unifrax (US), and Elmelin Ltd. (UK). These players have adopted various growth strategies, such as expansion, acquisition, new product launch, and investment, to expand their presence further and increase their shares in the microporous insulation market. Expansion has been the most adopted strategy by major players between 2013 and 2018, which helped them to expand their regional presence. To know about the assumptions considered for the study download the pdf brochure Promat International N.V. is one of the leading manufacturers of microporous insulation, globally. The company focuses on the strategies of expansion and investment to maintain its leading position in the market. For example, the company recently opened a new facility in the Middle East at Dubai Investment Park (DIP). The new facility has significant capacity for Promat boards, fire stopping, and High Performance Insulation (HPI) products, which include microporous insulation. In addition, in October 2013, Etex Group, the parent company of Promat International invested USD 13.27 million in its subsidiary, Microtherm NV (Belgium). This investment helped the company to expand its microporous insulation segment and enter various niche markets using high-temperature insulation products. Morgan Advanced Materials plc is another major player in the microporous insulation market. The company focuses on improving its operational execution and driving its sales by managing its resources, customers, and distribution channels. The company has focused on the strategies of acquisition as part of its growth. For instance, in July 2014, Morgan Advanced Materials acquired Porextherm Dämmstoffe GmbH (Germany), one of the leading manufacturers of microporous insulation panels. This acquisition helped Morgan Advanced Materials to strengthen its product portfolio of microporous insulation and vacuum insulation panels. Thus, the acquisition helped the company to strengthen its microporous insulation business. Related Reports: Microporous Insulation Market by Product Type (Rigid boards & panels, flexible panels, machined parts, moldable products), Application (Industrial, Energy & Power, Oil & Gas, Aerospace & Defense, Automotive), and Region – Global Forecast to 2023  Expansions and mergers & acquisitions were the key strategies adopted by industry players to achieve growth in the global chlor-alkali market between 2013 and 2015. These two strategies together accounted for the largest share of all the strategies adopted by market players.

Some of the leading chlor-alkali manufacturers are Olin Corporation (U.S.), Occidental Petroleum Corporation (U.S.), Axiall Corporation (U.S.), AkzoNobel N.V. (Netherlands), Formosa Plastic Corporation (Taiwan), Hanwha Chemical Corporation (Korea), Tosoh Corporation (Japan), Nirma Limited (India), and Tronox (U.S.). To know about the assumptions considered for the study, download the pdf brochure Besides expansions and merger & acquisitions, companies adopted joint ventures and agreements to expand their market share and distribution network. These strategies accounted for a small share of the total number of growth strategies adopted by the market players in the chlor-alkali market between 2013 and 2015. Solvay, Olin, Tata Chemicals, and AkzoNobel are some of the global market players who expanded their production facilities and entered into various agreements between 2012 and 2015 for expanding their market reach. During the same time period, Tosoh, Tronox, and Olin entered into various mergers & acquisitions. Tronox is also the largest natural soda ash producer globally and with the acquisition of FMC Corporation it is one of the market leaders. Tosoh entered into one merger and one acquisition in 2014 and 2015, respectively. In 2015 it acquired shares of Mabuhay Vinyl Corporation (Philippines) to increase its integrated supply of vinyl isocyanate and also penetrate into the growing Philippines market. The company also engaged with Nippon Polyurethane Co. Ltd. (Japan) to cope up with the domestic challenge. These moves will help the company to mark a greater presence in the Asia-Pacific region. Solavy was very active in expanding its global footprint by expanding its facilities in the U.S. and Thailand. In Thailand, the company has Asia’s largest sodium bicarbonate plant. Solvay also expanded its Wyoming facility in the U.S. for soda ash. The expansion is expected to increase the manufacturing capacity of the plant by 150 kilotons to meet the growing demand from its U.S. export markets. Other developments between 2013 and 2015 include development of new and enhanced membrane plants and expansions by OxyChem, Hanwha Chemical Corporation, and Xinjiang Zhongtai. Related Reports: Chlor-Alkali Market by Products (Caustic Soda, Chlorine, and Soda Ash), Applications (Alumina, EDC/PVC, Glass, Organic Chemicals, Inorganic Chemicals, Food, Pulp & Paper, Water Treatment and Others) & Region – Global Forecast to 2021  The sodium silicate market size is projected to reach USD 11.03 Billion by 2022, at a CAGR of 4.4% between 2017 and 2022. Sodium silicate is a versatile inorganic chemical. It is produced as a white crystalline powder or in the form of lumps that are soluble in water. It is manufactured by melting sand/silicon dioxide (SiO2) and soda ash/sodium carbonate (Na2CO3) at a temperature above 1800 °F in a closed end furnace. Caustic soda/sodium hydroxide is used instead of sodium carbonate for the direct production of liquid sodium silicate. Sodium silicate is a non-toxic, non-flammable, and non-explosive chemical. It is a strong alkaline chemical having high pH ranging from 10 to 13. Its alkaline nature makes it preferable for various applications such as detergents, precipitated silica, construction, pulp & paper, textiles, paints, foundry, and water treatment. The increasing use of sodium silicate in various applications, such as detergents, precipitated silica, and pulp & paper, is expected to drive the market.

Expansions, acquisitions, and mergers were the key strategies adopted by the major players to achieve growth in the global sodium silicate market between 2015 and 2018. The major players in the sodium silicate market are PQ Corporation (US), Occidental Petroleum Corporation (US), Tokuyama Corporation (Japan), Nippon Chemical Industrial (Japan), BASF (Germany), Kiran Global Chem Limited (India), Sinchem Silica Gel (China), Shijiazhuang Shuanglian Chemical Industry (China), IQE Group (Spain), and CIECH (Poland). To know about the assumptions considered for the study, download the pdf brochure Nippon Chemical Industrial used expansions as its major strategy to increase its presence in the Southeast Asian market. In August 2017, Nippon Chemical Industrial established a new company JCI in Thailand through a joint venture with local capital. With this expansion, the company aims to expand its business in Southeast Asia, majorly in Thailand. Tokuyama Corporation used mergers as its major strategy to strengthen its sodium silicate business. In February 2017, Tokuyama Corporation made an absorption-type merger (simplified merger) with its wholly-owned subsidiary Tokuyama Siltech (Japan). The company expects to increase the business of sodium silicate with this merger. IQE Group used acquisition as its major strategy to increase its sodium silicate production capacity. In November 2015, IQE Group acquired the silicate division of PeroxyChem (US) that includes the silicate production line located at the La Zaida plant and the Zamudio factory in Spain. With this acquisition, the company has increased its production capacity and reduced its competition in Spain. Related Reports: Sodium Silicate Market by Form (Solid Sodium Silicate, Liquid Sodium Silicate), Application (Detergents, Precipitated Silica, Construction, Pulp & Paper, Water Treatment, Metal Casting, Food Preservation), and Region – Global Forecast to 2022  The global market for toluene is projected to witness steady growth during the forecast period. The factors contributing towards the growth of this market are, the growth of the end-user base in the emerging economies of the Asia-Pacific and the Middle Eastern & African regions. Countries such as China and India are witnessing a healthy increase in petrochemical industrial activities because of the relocation of manufacturing facilities from the high-cost European and North American markets to the low-cost markets of the Asia-Pacific and Middle Eastern & African regions. Along with these factors, the growing end-user base is driving the market for toluene.

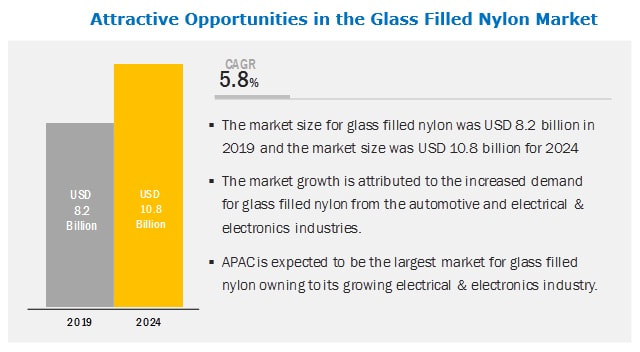

The global toluene market has a large number of market players; however the market is led by some of the major players, such as China Petroleum & Chemical Corporation (China), China National Petroleum Corporation (China), Exxon Mobil Corporation (U.S.), Covestro AG (Germany), and BP P.L.C. (U.K.), among others. Together, these companies account for approximately 34% share of the toluene market. The other major players in the toluene market are, SK Innovation Co., Ltd. (South Korea), BASF SE (Germany), GS Caltex (South Korea), Formosa Chemicals & Fiber Corporation (Taiwan), Royal Dutch Shell PLC (Netherlands), and CPC Corporation (Taiwan), among others. To know about the assumptions considered for the study, download the pdf brochure Most of these companies are leaders in the production of toluene and its derivatives. These companies are focusing on eliminating the supply chain gaps with backward or forward integration, and expansions in the emerging markets of the Asia-Pacific region in order to widen and strengthen their market shares. Market players are concentrating on increasing their production capacities and developing cost effective technologies. The companies are investing in establishing new facilities, mainly in the emerging regions so as to increase their global presence. All these developments are due to the increasing demand for toluene from segments such as, solvents, TDI, and gasoline additives. Expansions and backward or forward integration are the key strategies adopted by the major toluene manufactures in the recent past. The top players in the toluene market are adopting these strategies for better penetration and expansions of their businesses into new emerging regions. These new ventures would help the companies to satiate the growing demand for toluene in several applications. ExxonMobil (U.S.), and BP PLC (U.K.) are the few among the other market players who have adopted these strategies in order to strengthen their shares in the toluene market. Moreover, the leading market players are also focusing on expanding their existing production facilities in order to meet the growing demand for toluene, especially from the Asia-Pacific region. The market players are using this strategy as an excellent strategy to optimize their production facilities in the potential toluene markets. Related Reports: Toluene Market by Application and Derivative (Benzene and Xylene, Solvents, Gasoline Additive, Toluene Di-Isocyanate, Benzoic Acid, Trinitrotoluene, Andbenzaldehyde) – Global Forecast to 2021  The glass filled nylon market size is estimated to grow from USD 8.2 billion in 2019 to USD 10.8 billion by 2024, at a CAGR of 5.8% between 2019 and 2024. The superior properties offered by glass filled nylon and the growing automotive industry are majorly driving the market.

The major glass filled nylon manufacturers are BASF SE (Germany), Asahi Kasei Corporation (Japan), Lanxess (Germany), DowDuPont Inc. (US), Royal DSM N.V. (Netherlands), Ensinger GmbH (Germany), Arkema (France), SABIC (Saudi Arabia), Evonik Industries (US) and Ascend Performance Materials (US). These players have adopted various growth strategies such as acquisition and new product launch to expand their presence in the global market. Acquisition was the dominant strategies adopted by the major players, between 2014 and 2019, which helped them to offer innovate products and broaden their customer base. To know about the assumptions considered for the study download the pdf brochure BASF SE has secured a strong position in the European market. It is also establishing its presence in Latin America and the MEA and is now focusing on APAC. The company is a strong market player in the functional materials & solutions business segment. It has a strong focus on R&D and has acquired Solvay’s global polyamide business. This has helped the company to maintain its market position and expand its glass filled nylon business. Asahi Kasei Corporation has a prominent presence in the glass filled nylon market. The company has a strong brand image, and it caters to the growing demand for glass filled nylon, particularly from the automotive application. It opted inorganic growth strategy through the acquisition of Sage Automotive Interiors, Inc. (US). This will increase the glass filled nylon market, as automotive is a key end-use industry of glass filled nylon. The company mainly focuses on R&D activities to maintain its comprehensive portfolio of glass filled nylon products that have significant growth potential. Related Reports: Glass Filled Nylon Market by Type (Polyamide 6, Polyamide 66),End Use Industry(Automotive, Electrical & Electronics, Industrial), Manufacturing Process(Injection Molding, Extrusion Molding), Glass Filling and Region Global Forecast to 2024  Economizers are mechanical devices that are used to make machines energy efficient by lowering their energy consumption. Economizers, owing to their exceptional characteristic of energy conservation and fuel saving, are been widely used in industrial boilers. Schneider Electric SE (France), Johnson Controls International plc (US), Alfa Laval AB (Sweden), Babcock & Wilcox Enterprises, Inc., (US), Honeywell International Inc. (US), Thermax Limited (India), Cleaver-Brooks, Inc. (US), SAACKE GmbH (Germany), SECESPOL Sp. z o.o. (Poland), STULZ Air Technology Systems, Inc. (US), Kelvion Holding GmbH (Germany), BELIMO Holding AG (Switzerland), Cain Industries (US), Sofame Technologies Inc. (Canada), Cannon Boiler Works (US), Shandong Hengtao Group (China), and MicroMetl Corporation (US) are key players operating in the economizer market.

Acquisitions, contracts, expansions, and collaborations are major growth strategies adopted by leading companies in the economizer market. These companies are also investing in R&D activities to strengthen their product portfolio and enhance their presence in the economizer market. To know about the assumptions considered for the study, download the pdf brochure Schneider Electric SE is a global specialist in energy management and automation solutions. The company was founded in 1836 and is headquartered in Rueil-Malmaison (France). It operates through 4 business segments, namely, building, industry, infrastructure, and information technology. Schneider Electric SE offers energy saving products under its critical power, cooling, and racks segment. The company focuses on sustainable development and has a broad product portfolio, along with a wide industry coverage. The company also specializes in industrial software design, process & machines management, security management, power management, industrial automation and control, IT room management, simulation and optimization, building management, and safety systems and instrumentation. Schneider Electric SE offers EcoBreeze air economizer products. The company focuses on the adoption of both, organic and inorganic growth strategies to expand its geographic reach in the economizer market. For instance, in October 2016, Schneider Electric SE and Panasonic Corporation (Japan) jointly developed HVAC equipment and building management solutions to reduce energy consumption in various applications. Furthermore, in February 2014, AREVA (France) and Schneider Electric SE signed a strategic partnership to develop energy management and storage solutions based on the hydrogen fuel cell technology. Johnson Controls International plc, another key player in the economizer market, was founded in 1885 and is headquartered in Cork (Ireland). In 2016, the company changed its name from Johnson Controls, Inc. to Johnson Controls International plc. The company is engaged in the manufacturing and marketing of building management systems; Heating, Ventilating, and Air Conditioning (HVAC) systems; residential air conditioning and heating systems; security and mechanical equipment; and industrial refrigeration products. It engages in the production and supply of economizer products worldwide. Johnson Controls International plc adopted inorganic growth strategies, such as mergers, to strengthen its foothold in the economizer market. For instance, in September 2016, the company merged with Tyco (Ireland) to provide building efficiency solutions for commercial buildings, large institutions, retail, and industrial markets. Related Reports: Economizer Market by Type (Fluid Economizers and Air-side Economizers), Application (Power Plants, Boilers, HVAC, Refrigeration, and Data Centers), End-use Industry (Industrial and Commercial), Region – Global Forecast to 2022 Key Strategy Adopted by the Leading Market Players to Achieve Growth in the Floor Adhesive Market6/19/2019  Floor adhesive are materials that are used to hold two surfaces together. These adhesives can be of diverse types, including urethane, acrylic, epoxy, silane modified polymer, and others. These adhesives are used in different flooring applications, such as tile & stone, carpet, wood, vinyl, and others.

Key players operating in the floor adhesive market have adopted various strategies to strengthen their position in the market. Mergers & acquisition was the key strategy adopted by the leading market players to achieve growth in the floor adhesive market between 2014 and 2017. Key players in the market also adopted strategies, such as investments and expansions, new product launches, partnerships & collaborations, and agreements to increase their shares in the floor adhesive market and strengthen their distribution networks. To know about the assumptions considered for the study, download the pdf brochure Mapei S.p.A. (Italy), Sika AG (Switzerland), Henkel AG (Germany), Bostik SA (France), H.B. Fuller (U.S.), The Dow Chemical Company (U.S.), Wacker Chemie AG (Germany), Forbo Holdings AG (Switzerland), Pidilite Industries Limited (India), Ardex Group (Germany), and Franklin International (U.S.) are some of the leading players in the floor adhesive market. Mapei S.p.A. is one of the leading companies in the floor adhesive market. The company offers several types of floor adhesive for varied applications, such as ceramic and stone adhesives, timber flooring, resin floor covering, and decorative flooring, among others. Mapei Group acquired the Colombian company Productos Bronco S.A., which specializes in the production of waterproofing products, adhesives, sealants, and finishes. Mapei has strengthened its presence in South America with this acquisition. Mapei Construction Products India Ltd. expanded its presence in the Asia-Pacific by establishing a new production site in Vadodara in Gujarat (India). In 2016, Bostik SA expanded its cementitious products manufacturing capacities at its Seremban plant in Malaysia. The plant specializes in cement-based construction products, such as adhesives and sealants for tiles and expansion joint sealants for flooring. In May 2017, Bostik acquired floor preparation systems of CGM, Inc. The acquisition is a part of Bostiks strategy to expand in the growing US construction market and offer its customers a complete range of innovative solutions in the flooring market. In 2016, Sika AG acquired L.M. Scofield (U.S.) and Ronacrete Ltd. L.M (Hong Kong). Scofield is a leading producer of color additives for ready-mix concrete. The acquisition will help Sika AG in the production of different concrete flooring products. Ronacrete Ltd. is one of the leading suppliers of repair mortars, tile adhesives, and other mortar products in Hong Kong. The acquisition of the company will strengthen the position of the company in the floor adhesive market. Related Reports: Floor Adhesive Market by Type (Epoxy, Urethane, Acrylic, and Vinyl), Application (Tile & Stone, Carpet, Wood, and Laminate), Technology (Water-based, Solvent-based and Hot-melt based), and Region – Global Forecast to 2022 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed