The polyurethane additives are used in various end-use industries such as automotive & transportation, building & construction, bedding & furniture, electronics, and others. COVID-19 has impacted these industries.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=121317889

0 Comments

The pandemic is estimated to have huge impact on various factors of the value chain of insulating glass windows, which is expected to reflect during the forecast period, especially in the year 2020-2021. The various impact of COVID-19 are as follows:

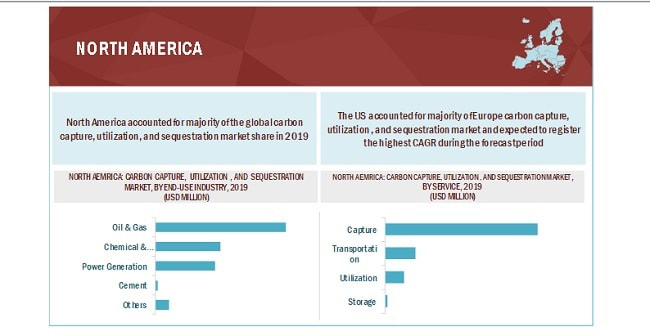

Browse 116 market data Tables and 41 Figures spread through 187 Pages and in-depth TOC on “Insulating Glass Window Market by End Use (Residential & Commercial), Spacer Type (Aluminum, Stainless Steel, Intercept, 4SG Thermoplastic, & Others), Sealant (Silicone, Polysulfide, Polyurethane, Hot-melt Butyl, Others) and Region – Global Forecast to 2025” Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=36258309  The global carbon capture, utilization, and storage market size is expected to grow from USD 1.6 billion in 2020 to USD 3.5 billion by 2025, at a CAGR of 17.0% during the forecast period. The carbon capture, utilization, and storage market are growing due to the increasing usage of CCSU systems in the oil & gas and power generation sector to reduce harmful carbon emissions.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=151234843 Current and upcoming projects of CCUS in the APAC region have created an excellent gateway toward the adoption of CCUS. China and Australia are the early adopters of CCUS in the APAC region. The current line-up of carbon capture and sequestration projects in these countries is expected to create an immense opportunity for the companies operating in the carbon capture, utilization, and sequestration ecosystem. Other than Australia and China, South Korea and India are also focusing on adopting CCUS. For instance, South Korea has already taken a step toward CCUS in the Korea CCS 1&2 project, which is currently in an early development stage and is expected to be operational by 2021. India, in 2016, initiated the operation of a carbon capture and utilization system, which was capable of capturing 60,000 tons of C02 per year from coal-fired power plants. Recent Developments

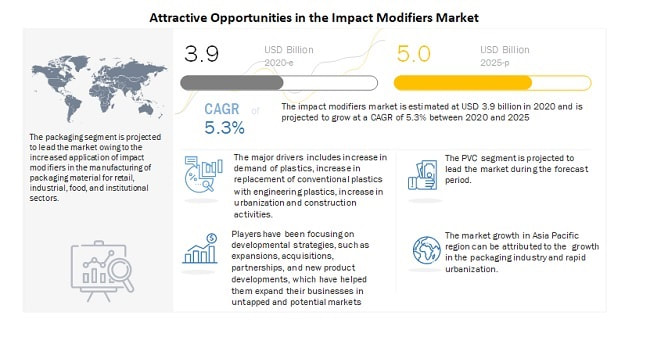

The key players in the global carbon capture, utilization, and sequestration market a Royal Dutch Shell (Netherlands), Aker Solutions (Norway), Mitsubishi Heavy Industries, Ltd. (Japan), Linde PLC (UK), Hitachi, tLd.(Japan), Exxon Mobil Corporation (US), JGC Holdings Corporation (Japan), Honeywell International, Inc. (US), Halliburton (US), and Schlumberger Limited (US). Speak to analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=151234843  In 2020, the global impact modifiers market size is estimated at USD 3.9 billion and projected to reach USD 5.0 billion by 2025, at a CAGR of 5.3% from 2020 to 2025. The major drivers for the market include an increase in demand for plastics, replacement of conventional plastics with engineering plastics, and urbanization & construction activities. Moreover, the demand for plastics in packaging applications and the development of impact modifiers for bio-based polymers are expected to propel the market for impact modifiers.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=58674504 The rising concern for the environment is driving the market for bio-plastic materials. Bio-plastics are made up of biodegradable material and cellulose. These plastics are derived from renewable biomass sources or bio-degradable sources such as PLA. The leading players in the impact modifiers market are focusing on carrying out R&D activities to develop impact modifiers that can be used in different industries for different applications. With the increased demand for bio-based polymers, there is a requirement for developing new and improved impact modifiers. This, in turn, is expected to lead to advancements in the field of impact modifiers. Recent Developments In June 2020, Mitsui Chemicals and Prime Polymer, in which Mitsui Chemicals has a 65% stake, jointly established a company to build a new polypropylene plant in the Netherlands. The plant has a capacity of 30,000 mt/year, and operations had begun in June 2020. This expansion was done with a view of increasing demand for PP to meet light-weighting needs in bumpers, instrument panels, and more. In September 2019, Arkema completed acquired its partner’s stake in Taixing Sunke Chemicals, its joint venture manufacturing acrylic monomers in China. With the acquisition, Arkema has become the sole shareholder of the company. With this transaction, the company would be able to support the growth of its customers in Asia and benefit from greater flexibility to run this business in a region which accounts for more than 50% of the global acrylic acid demand. This would also help in the uninterrupted supply for acrylic monomer for manufacturing acrylic base impact modifiers. Asia Pacific is expected to witness the fastest growth in the impact modifiers market The impact modifiers market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific impact modifiers market in 2019. Moreover, the Asia Pacific region is an emerging and lucrative market for impact modifiers, owing to industrial development and improving economic conditions. The presence of a number of plastic products manufacturing plants in China and rapid industrialization in Asia Pacific are expected to drive the impact modifiers market during the forecast period. Major companies such as Dow Inc. (US), Lanxess A.G. (Germany), Kaneka Corporation (Japan), Arkema S.A. (France), Mitsubishi Chemical Corporation (Japan), LG Chem Ltd. (South Korea), Shandong Ruifeng Chemical Co., Ltd. (China), Mitsui Chemicals, Inc. (Japan), Wacker Chemie AG (Germany), Formosa Plastics Corp. (Taiwan), Sundow Polymers Co., Ltd. (China), SI Group, Inc. (US), Akdeniz Kimya San. ve Tic. Inc. (Turkey), ), En-Door (China), Novista Group (China), and Indofil Industries Limited (India) and among others.  COVID-19 is an infectious disease caused by the newly discovered coronavirus. The spread of this virus is impacting the growth of economies across the globe. The disease was unknown before its outbreak In Wuhan (China) in December 2019.

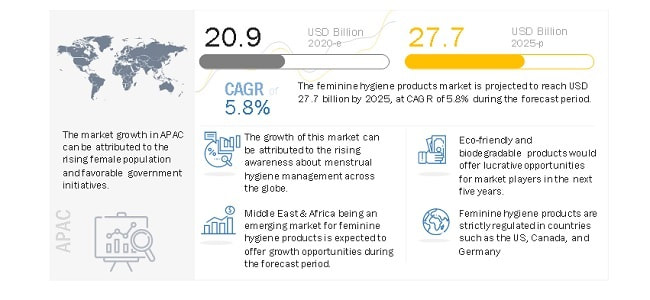

The primary impacts of an outbreak are defined as direct and immediate consequences of this pandemic on human health. However, secondary impacts are those caused by the pandemic indirectly, either through the effect of fear on the population or because of measures taken to contain and control it. The COVID-19 pandemic is expected to have a secondary impact on the feminine hygiene products market. The impact will vary country-wise and with the ability to respond through social protection and medical infrastructure. It is believed that the most affected consumers will be the poorest and most vulnerable to economic and social shocks. According to a survey conducted by the Menstrual Health Alliance India, the COVID-19 pandemic has severely hit access to feminine hygiene products. As per the survey, over 82% of feminine hygiene product manufacturers had to pause operations in India due to social distancing norms and lockdown. With production becoming constrained, the availability of these products, including disposable and reusable sanitary pads at a rural level. Consumers who could access the products at local markets earlier were unable to do so due to the lack of public transport and mobility restrictions under the lockdown. According to the Feminine and Infant Hygiene Association of India, China fulfills approximately 10-15% of India’s requirement of sanitary napkins, and with most of the country’s manufacturing halted, there was a severe shortage of products resulting in black marketing and artificial price rise. However, a different trend was observed in the US. Just as the COVID-19 pandemic disrupted work, school, and social routines, so did hoarding interrupted the supply of feminine hygiene products. Consumers with lower incomes have faced the consequences of hoarding, leading to a price rise during the lockdown period. Women relying on free feminine hygiene products from schools, social service centers, government health centers, and medical facilities also faced shortages due to the COVID-19 pandemic. As a result, non-profit organizations such as Support, The Girls have started taking initiatives to bridge this gap. This organization donated over 900,000 feminine hygiene products in March 2020 alone to Los Angeles, New Jersey, Washington D.C., Maryland, and Virginia. Download PDF Brochure to Know More: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=69114569 The global feminine hygiene products market size is projected to grow from USD 20.9 billion in 2020 to USD 27.7 billion by 2025, at a CAGR of 5.8% during the forecast period 2020 to 2025. Increasing female population & rapid urbanization, rising female literacy and awareness of menstrual health & hygiene, rising disposable income of females, and women empowerment are expected to accelerate the growth of the feminine hygiene products market across the globe. Browse 143 market data Tables and 46 Figures spread through 195 Pages and in-depth TOC on “Feminine Hygiene Products Market by Nature (Disposable, Reusable), Type (Sanitary Napkins, Panty Liners, Tampons, Menstrual Cups), Region (Asia Pacific, North America, Europe, Middle East and Africa, South America) – Global Forecast to 2025” Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=69114569  The global geomembranes market size is expected to grow from USD 2.1 billion in 2020 to USD 3.2 billion by 2025, at a Compound Annual Growth Rate (CAGR) of 8.3% during the forecast period. This high growth is due to the increased mining activities in APAC and South America, the growing concerns towards waste and water management activities, and the increasing spending on infrastructure development.

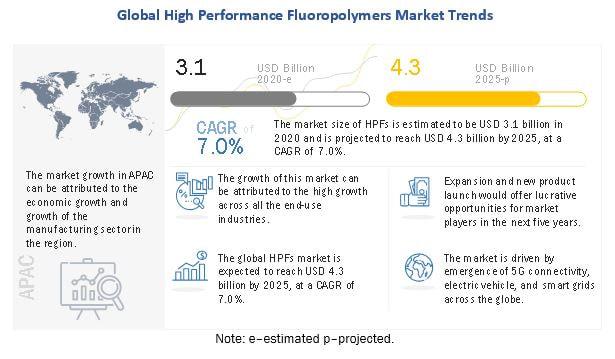

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=133281673 Rapid industrialization and urbanization in key countries such as China and India have spurred the demand for metals and minerals in the past few years. Other countries in APAC that have attracted significant mining investments include Australia, New Zealand, Japan, South Korea, Singapore, Mongolia, and Indonesia. South America is also a high-growth region for the mining industry. It has become a preferred destination for mining investments by major global mining companies. Key countries such as Brazil, Peru, and Chile have large mining capacities and have witnessed increased investments from foreign companies over the past five years. The mining industry is one of the major consumers of geomembranes. Geomembranes are used to help recapture and recycle the harmful chemicals being used in solution to treat ponds and secondary containment applications. This is expected to drive the geomembranes market during the forecast period. Mining, waste management, water management, and civil construction are the major applications in the geomembranes market. Of these, waste management is estimated to be the fastest-growing application. Geomembranes are essential for controlling the leakage of contaminated gas and liquid into the surrounding environment. They are ideally used in landfill caps, landfill covers, landfill liners, temporary landfill closures, animal waste containment, and sludge treatment application due to their ability to accommodate differential settlement in the waste pile. Major vendors in the geomembranes market include Solmax (Canada), Raven Industries (US), AGRU (Austria), Carlisle Construction Materials LLC (US), Atarfil (Spain), PLASTIKA KRITIS (Greece), JUTA (Czech Republic), Maccaferri (Italy), Firestone Building Products (US), The NAUE group (Germany), Anhui Huifeng New Synthetic Materials (China) & more. Solmax (Canada) is a leading geomembranes manufacturer. The company aims to become the global expert in geosynthetics for the environmental containment and civil engineering markets. The company emphasizes the development of innovative products that are more reliable, stronger, resistant to contaminants, and affordable, even in developing countries. AGRU (Austria) is a leading geomembranes manufacturer, boasting a wide product portfolio and application-oriented solutions. It has a global presence and serves various industries through its lining systems product group. It also has a strong sales networks which helps the company supply products in more than 150 countries. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=133281673  The high performance fluoropolymer (HPF) market is projected to grow from USD 3.1 billion in 2020 to USD 4.3 billion by 2025, at a CAGR of 7.0% during the forecast period. The growth of the high performance fluoropolymer industry can be attributed to its high demand from various end-use industry and growing demand from renewables.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=497 Melt-processable fluoropolymers are based on copolymer resins: FEP, ETFE, PFA, MFA, PVDF, ECTFE, and PCTFE, which can be processed into different shapes. The polymerization and fabrication techniques for these fluoropolymers include injection molding, wire, tube, and film extrusion, rotational molding, blow molding, compression molding, and transfer molding. ETFE, FEP, and PCTFE are thermoplastic. Thermoplastics are polymers that liquefy when heated and solidify when cooled down. The cycle of melting and freezing can be recurrent. HPFs are mainly used for extreme temperature applications in various end-use industries, such as industrial processing, transportation, electrical & electronics, medical, and others. They are also useful for a wide range of other applications, which include consumer goods, machine parts, medical equipment, and packaging and storage materials. They are becoming the material of choice and replacing the traditional materials, such as steel, aluminum, and wood, as they are melt processable and thermoplastic. In comparison to other traditional materials, melt-processable fluoropolymers have higher chemical and impact resistance as well as higher strength-to-weight ratios. They also offer greater design flexibility in comparison to traditional materials. The melt-processable thermoplastic fluoropolymers market is projected to witness higher growth than PTFE during the forecast period, owing to the significant demand from emerging applications, such as photovoltaic modules and architectural membranes. When compounded with fillers, pigments, and other additives, these fluoropolymers gain higher functionality and improved characteristics to be suitable for applications, such as wire & cable; semiconductor and electronic components; valves, fittings, and pump housings; tubing and pipe; and specialty films. This will further enhance the growth prospects of the HPFs market worldwide. APAC is expected to be the fastest-growing market for HPF, owing to the presence of large manufacturing and highly populated countries, such as China and India. China, India, Japan, Indonesia, and South Korea are some of the key countries in the HPF market in this region. In 2019, China accounted for the largest share of the APAC market, owing to the presence of huge chemical, automotive, medical, and electronics industries. The growing production of automobiles, consumer household, medical disposables, and their increasing demand across the region boosts the demand for HPF. Growth in the manufacturing of automobiles and electronics hardware across the region is expected to grow further with changing demographics. Owing to which APAC is projected to be the fastest-growing HPF market. Speak with analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=497 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed