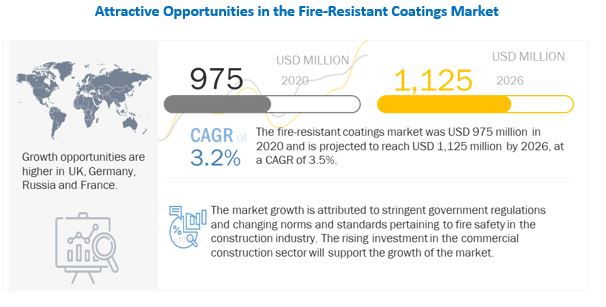

Akzo Nobel (Netherlands) and PPG (US) are the Leading Players in the Fire-resistant Coatings Market3/29/2022  The fire-resistant coating market was USD 975 million in 2020 and is projected to reach USD 1,125 million by 2026, at a CAGR of 3.5%. Europe accounted for the largest share of the market. It is projected to reach USD 490 million by 2026, at a CAGR of 3.0%, between 2021 and 2026. The growing building & construction sector in the region is projected to drive the market. Due to stringent government regulations and fire safety norms in developed regions, fire-resistant coatings have become an indispensable part of the buildings & construction industry as well as the oil & gas, chemical, and other industries wherein the chances of fire hazards are high.

The fire-resistant coating is applied to surfaces to protect them against fire and to reduce the loss incurred due to fire hazards in buildings & construction as well as in the manufacturing sector. Industrially, intumescent coating and cementitious coatings are applied on the surface of steel, wood, plastics, and other materials to evade the propagation of fire and to maintain structural integrity by resisting fire, which, in turn, helps to save lives and minimize the damage. The selection of fire-resistant coatings depends on construction types, fire safety norms, international building standards and regulations, and potential fire. These coatings are used in commercial and residential buildings and industrial applications. They are also used for exterior and interior steel applications, walls, and steel frameworks. To know about the assumptions considered for the study download the pdf brochure The leading players in the fire-resistant coating market include Akzo Nobel (Netherlands), PPG (US), Jotun (Norway), Sherwin-Williams (US), and Hempel (Denmark). The key industry players are adopting strategies to expand their presence and enhance their product portfolio through investments in R&D. Due to the rise in the number of fire accidents at residential, public places, and workplaces, the number of deaths and damage to assets is also increasing. In view of this, end-users are increasingly adopting safety measures to protect people and property. Governmental agencies are also making rules regarding the addition of fire-resistant coatings in buildings to reduce these fire accidents. AkzoNobel N.V., AkzoNobel is engaged in the manufacturing and sales of paint and coating products. It operates its business through two major segments⎯Decorative Coatings and Performance Coatings. The company has over 28 manufacturing facilities and has sales activities in more than 150 countries across the globe. The Performance Coatings segment is divided into marine and protective coatings, automotive and specialty coatings, industrial coatings, and powder coatings. Under the protective coatings sub-segment, the company offers intumescent coating products, i.e., passive fire resistance coating products under the trademarks “Interchar” and “Chartek.” The company offers 23 types of passive fire protection coatings products for building & construction, oil & gas, and other industrial applications. PPG Industries, Inc., PPG Industries is a global supplier of paints, coatings, optical products, and specialty materials. It serves customers in industrial, consumer products, transportation, and construction markets. PPG has headquarters in Pittsburgh. The company has 156 manufacturing facilities worldwide. It caters to North America, South America, Asia Pacific, Europe, the Middle East, and Africa. The company has two major segments: Performance Coatings and Industrial Coatings. Performance coating is further segmented into Automotive Refinish Coatings, Aerospace Coatings, Protective and Marine Coatings, and Architectural Coatings. Fire-resistant coating comes under the Protective and Marine Coatings segment. Companies have initiated the following developments:

0 Comments

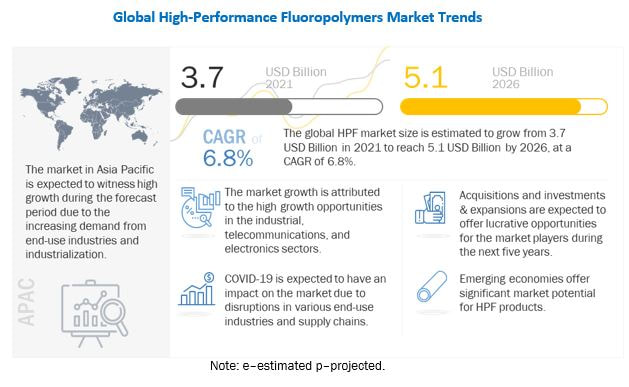

The high-performance fluoropolymer (HPF) market is projected to grow from USD 3.7 billion in 2021 to USD 5.1 billion by 2026, at a CAGR of 6.8% during the forecast period. The growth of the high-performance fluoropolymers industry can be attributed to its high demand from various end-use industry and growing demand from renewables.

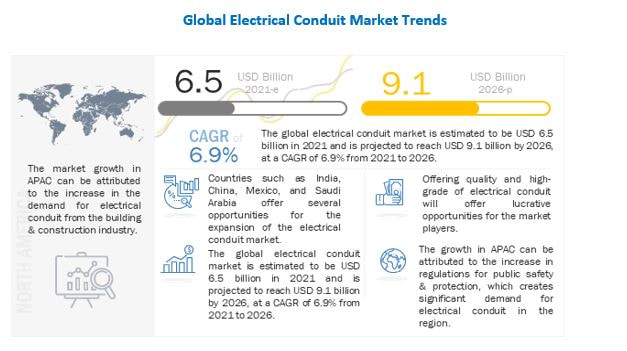

The transportation (automotive and aerospace), electrical & electronics, industrial processing, and medical industries extensively use HPF due to their advantages over other polymers and versatile properties. These industries are growing rapidly, which is boosting the demand for HPF. High heat resistance, low weight, high dimensional stability, and good chemical resistance are increasing the demand for HPF in the automotive industry. HPF are used in various parts of engines to improve the performance and durability of vehicles. They are used to manufacture different interior and exterior components in the automotive and aerospace sectors. The growth opportunities of the HPF market in the automotive industry are primarily linked to lower emissions and increased fuel efficiency. In the aerospace industry, it is important to use a material, which is fire-retardant and emits low smoke and toxic gases. The various applications in this industry require HPF that can withstand aggressive application conditions under a broad range of temperatures. In aerospace engineering, lightweight materials are highly used, and thus, the aerospace industry is dependent on HPF that have the perfect combination low weight; temperature, flame, abrasion, and chemical resistance; and flexibility, and non-leaching capabilities. To know about the assumptions considered for the study download the pdf brochure Effective dielectric property, biocompatibility, and lubricity of HPF are leading the way for their adoption in medical surgeries and other procedures. HPF are used in the production of multi-lumen tubing, which is required for the manufacturing of minimally-invasive devices. Because of high-resistance toward chemicals and heat, they are used in implants for the hip, ear, skull, nose, and knee parts. The growing use of HPF in various applications, such as catheters, syringes, sutures, and bio-containment vessels, is driving the market. Some industries are entirely dependent on HPF, for instance, the semiconductor industry. This is because a fluoropolymer is the only material that can hold and transport the chemicals used in the semiconductor production process. APAC is expected to be the fastest-growing market for HPF, owing to the presence of large manufacturing and highly populated countries, such as China and India. China, India, Japan, Indonesia, and South Korea are some of the key countries in the HPF market in this region. In 2020, China accounted for the largest share of the APAC market, owing to the presence of huge chemical, automotive, medical, and electronics industries. The growing production of automobiles, consumer households, medical disposables, and their increasing demand across the region boosts the demand for HPF. Growth in the manufacturing of automobiles and electronics hardware across the region is expected to grow further with changing demographics. Owing to which APAC is projected to be the fastest-growing HPF market. The Chemours Company (US), Daikin Industries (Japan), 3M (US), Solvay (Belgium), AGC, Inc. (Japan), The Dongyue Group (China), GFL Limited (India), Fluoroseals SpA (Italy), Halopolymer (Russia), and Hubei Everflon polymer (China) are a few active players in the HPF market. Read More: https://www.marketsandmarkets.com/PressReleases/fluoropolymers.asp  An electrical conduit is an electrical piping system used for the protection and routing of electrical wiring. It is used for protecting cables, wires, and data links against heat, cold, tensile stress, pressure stress, and other external influences in the mechanical and electrical engineering industry. Many different brands/manufacturers offer various types of conduits for diverse applications with various technical requirements.

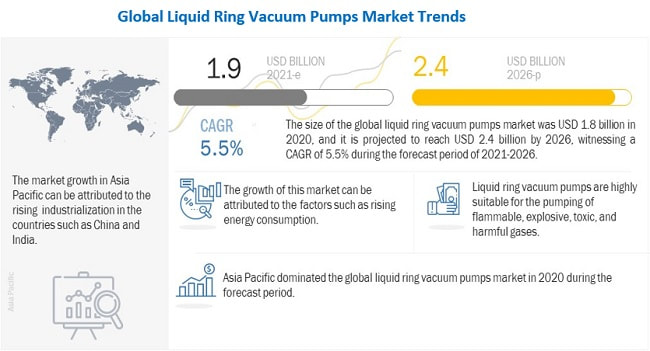

These electrical conduit systems have been one of the most reliable & popular wiring systems in the market and are primarily used for safety purposes. Electrical conduit is one of the safest wiring systems and offers an aesthetic view of electrical wiring. These conduit systems are experiencing a boost in demand as it protects the enclosed conductors from impact, moisture, and chemical vapors. Furthermore, it offers durability and can be used for many years. In addition to this, an electrical conduit prevents accidental damage to the insulation. When installed with proper sealing fittings, a conduit will not permit the flow of flammable gases and vapors, which protects from fire and explosion hazards in areas handling volatile substances. These properties of electrical conduit make it a preferred wiring system. The global electrical conduit market size is projected to reach USD 9.1 billion by 2026, at a CAGR of 6.9% from 2021 to 2026. The global electrical conduit market is estimated to be USD 6.5 billion in 2021 and is projected to reach USD 9.1 billion by 2026, at a CAGR of 6.9% from 2021 to 2026. The driving factors for the electrical conduit market are the rapid pace of industrialization and urbanization and the rise in demand for electricity or power generation across the globe. The growth of the electrical conduit market is supported by increasing awareness regarding public safety and the implementation of safety regulations by governments. To know about the assumptions considered for the study download the pdf brochure Flexible electrical conduit is expected to be the fastest-growing type in the electrical conduit market The flexible segment is projected to be the fastest-growing segment in the electrical conduit market. This electrical conduit is lightweight, typically less expensive than other options, and versatile & easy to install. Flexible electrical conduit is much easier to work with than rigid metal or plastic conduit. This is because there is no bending involved. However, flexible electrical conduit will not offer quite as much protection as rigid electrical conduit. It is flexible and can snake through walls and other structures. This electrical conduit is used owing to its advantages such as lightweight conduit, typically less expensive than other options, and versatile & easy to install. APAC is the largest market for electrical conduit. APAC led the global electrical conduit market, accounting for a share of 37.8% in 2020. APAC is segmented into China, Japan, India, South Korea, and the Rest of APAC. Factors such as ready availability of raw materials and manpower, along with sophisticated technologies and innovations, have driven economic growth in the APAC region. According to the World Bank, the two economic giants of the APAC region, China and Japan, were the world’s second and third-largest economies as of 2020. APAC was the largest market for electrical conduit, in terms of value, in 2020. Emerging economies in APAC are expected to have significant demand for electrical conduit due to the growth of the construction industry led by the rapid economic development and government initiatives in infrastructural developments. In addition, the rising population in these countries represents a strong customer base. APAC is expected to be the fastest-growing market for electrical conduit globally during the forecast period. Significant consumer base, rising urban population, low labor costs, and easy availability of raw materials are attracting international companies to shift their production facilities to the region, thus creating a high demand for electrical conduits in these industries. The increase in demand for electrical conduit can be largely attributed to the growing infrastructure and building & construction industries. The demand for electrical conduits is rising rapidly in the region owing to the high demand from the infrastructural sector. The electrical conduit market comprises major solution providers, Atkore International Group Inc. (US), Hubbell Incorporated (US), Legrand S.A. (France), Schneider Electric SE (France), and Sekisui Chemical Co., Ltd. (Japan) among others. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=116259711  The liquid ring vacuum pumps market size was USD 1.8 billion in 2020 and is projected to reach USD 2.4 billion by 2026, at a CAGR of 5.5% from 2021 to 2026, owing to the rising gas transportation sector. The oil & gas segment is the biggest application for liquid ring vacuum pumps. The growing investments in the crude oil industry are expected to drive the use of liquid ring vacuum pumps.

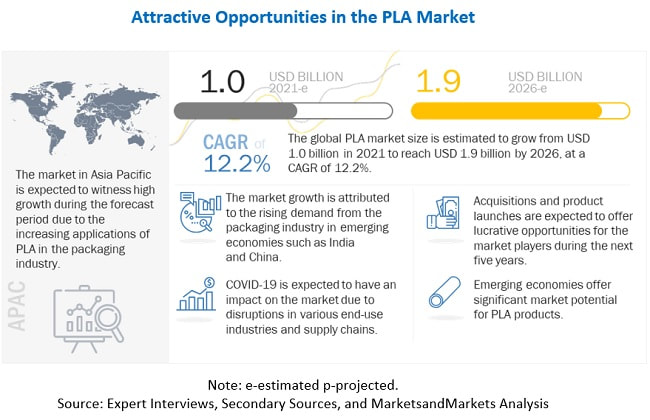

Liquid ring pumps can be employed for vacuum as well as compression jobs, which makes them popular across various industries. As with liquid, the pump uses its impeller to compress the gas. These pumps can be employed for applications such as vacuum distillation, moisture extraction, vacuum condensation, air or ash handling, evaporation, mineral beneficiation, and for separating water from paper pulp. Compared to other mechanical pumps, liquid ring vacuum pumps need minimal maintenance because they are driven by the liquid ring technology and have only one rotating part, the impeller, which reduces the need for regular maintenance. To know about the assumptions considered for the study download the pdf brochure By flow rate, 3000-10,000 m3/h segment is projected to grow at the highest CAGR during the forecast period The liquid ring vacuum pumps with a flow rate of 3,000-10,000 m3/h are considered medium capacity liquid ring vacuum pumps. Medium capacity liquid ring vacuum pumps are used in diverse applications across industries such as oil & gas and petrochemical & chemical. High demand from pulp & paper, oil & gas, power generation, and chemical industries is expected to fuel the growth of this segment. North America is expected to be the second-largest market in 2020, in terms of value North America is expected to be the second-largest market for liquid ring vacuum pumps during the forecast period. There is an increasing demand for liquid ring vacuum pumps from water and wastewater treatment plants in the region. Also, industries such as food & beverage, chemical processing, and pharmaceutical are driving the demand for liquid ring vacuum pumps in the region. The key market players include Busch Vacuum Solutions (Germany), Flowserve Corporation (US), Atlas Copco (Sweden), Ingersoll Rand (US), Tsurumi Manufacturing Co., Ltd (US), DEKKER Vacuum Technologies, Inc. (US), Vooner (US), Graham Corporation (US), Cutes Corp. (China), Zibo Zhaohan Vacuum Pump Co., Ltd (China), OMEL (Brazil), PPI Pumps Pvt. Ltd. (Mexico), Samson Pumps (Denmark), and Speck (Germany). These players have adopted product launches, agreements, acquisitions, mergers & acquisitions, and expansions as their growth strategies. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=231761054  The global PLA market size is projected to grow from USD 1.0 billion in 2021 to USD 1.9 billion by 2026, at a CAGR of 12.2% between 2021 and 2026. The major factors driving the market are the rising demand for PLA in packaging industry, stringent waste management regulations in Europe, increased focus of government on green procurement policies, and shift in consumer preference toward eco-friendly and biodegradable plastic products. Moreover, development of new applications, high potential in emerging countries of APAC, and multi-functionalities of PLA is expected to drive the market during the forecast period.

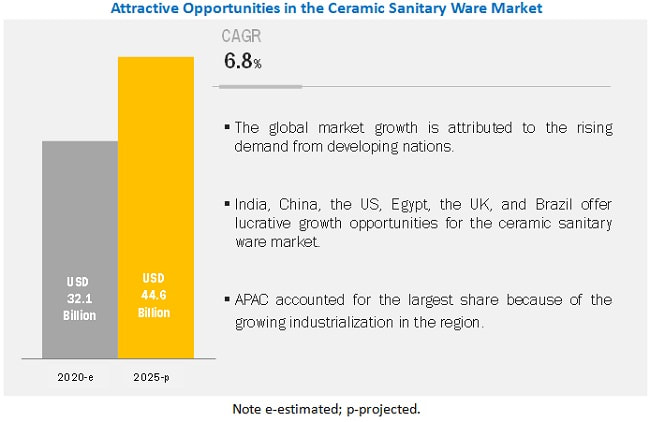

The major players in the market include NatureWorks LLC (US), Total Corbion PLA (Netherlands), BASF SE (Germany), Futerro (Belgium), COFCO (China), Mitsubishi Chemicals Corporation (Japan), Danimer Scientific (US), UNITIKA LTD.(Japan), Evonik Industries (Germany), and TORAY INDUSTRIES, INC (Japan) are some of the leading players in the market. These players have adopted various growth strategies to expand their presence in the market further. New product launch, investment & expansion, and merger & acquisition have been the leading strategies adopted by the major players in the last five years to strengthen their competitiveness and broaden their customer base in the global PLA market. To know about the assumptions considered for the study download the pdf brochure NatureWorks LLC is one of the leading manufacturer of PLA. The company has manufacturing plants in the North America, and Asia Pacific. In recent years, in recent years, NatureWorks LLC has adopted several business strategies to strengthen its position in the market. It has adopted various growth strategies, including investment & expansion, and new product launches, to maintain its position in PLA market. For instance, In June 2021, NatureWorks LLC invested USD 600 million for a PLA facility in Thailand. The company is focusing on increasing its annual PLA production capacity to 75,000 tons for Ingeo PLA grade. Total Corbion PLA is one of the major player operating in PLA market. The company has manufacturing facilities in Asia Pacific, and planning to manufacture a new PLA production plant Europe which is expected to become operational by 2024. The company has adopted new product launch, investments & expansion, and collaboration strategies in order to broaden its product portfolio and maintain its position in the market. For instance, In October 2021, Total Corbion PLA developed a new grade of PLA derived for recycled waste as Luminy rPLA to strengthen its PLA product portfolio. Read More: https://www.marketsandmarkets.com/PressReleases/polylactic-acid-pla.asp  The global ceramic sanitary ware market size is projected to reach USD 44.6 billion by 2025, at a CAGR of 6.8%, from USD 32.1 billion in 2020.

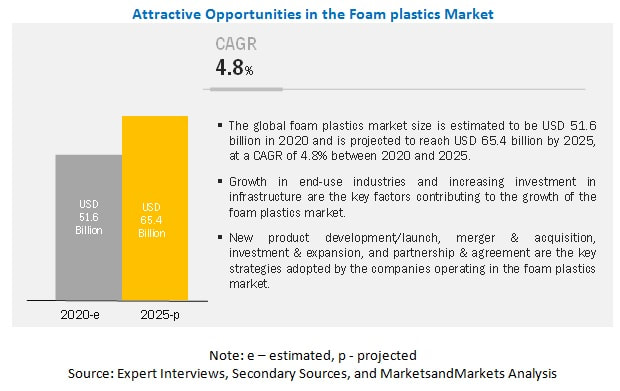

Initiatives by the public sectors of developing nations to improve access to sanitation are a major factor for the growth of ceramic sanitary ware globally. Historically, the awareness regarding personal hygiene was low in developing nations. Therefore, the ceramic sanitary ware market had limited growth and development. However, due to the multiple initiatives taken by the governments of developing countries, the awareness about hygiene and proper sanitation is increasing. According to the latest data by the WHO, 45% of the global population used the safely managed sanitation service in 2017. This number is expected to increase in the coming years due to the rising public awareness, professional marketing of sanitation to those lacking access, and initiative of the private sector in public sanitation. Moreover, the changing lifestyle and increasing purchasing power of the middle-class population are expected to drive the demand for the ceramic sanitary ware market between 2020 and 2025. To know about the assumptions considered for the study download the pdf brochure APAC is the largest market of ceramic sanitary ware, followed by Europe and North America. The massive industrial growth in APAC has been fueling the growth of the ceramic sanitary ware market over the past few years, which is expected to continue during the next five years. Domestic and foreign investments in key sectors, such as energy, manufacturing, construction, and mining, have been consistently growing over the past decade. It is expected to result in the growth of the industrial sector and the demand for ceramic sanitary ware in the country. Over the past decade, India has been witnessing moderate GDP growth. The country has attracted heavy investments in key industrial sectors, such as construction, cement, and energy. The economic outlook for India has been very optimistic. The Government of India is focused on the manufacturing sector by liberalizing policies and providing additional incentives, such as land at cheap rates and faster clearances from all the concerned departments. As a result, the overall economy is rapidly growing. This is expected to drive the sale of ceramic sanitary ware in the region during the forecast period. The demand for ceramic sanitary ware is expected to decline in 2020, mainly due to the economic crisis of COVID-19. The lockdown in countries all over the world has resulted in major construction projects getting stalled, which will negatively impact the market growth in 2020. The key market players profiled in the report include Geberit Group (Switzerland), Kohler Co. (US), TOTO Ltd. (Japan), LIXIL Group Corporation (Japan), Roca Sanitario SA (Spain), Villeroy & Boch AG (Germany), RAK Ceramics (UAE), Duravit AG (Germany), Duratex SA (Brazil), and HSIL (India). Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=581  Foam plastics are resins used in manufacturing polymer foams, which are used in various end-use industries such as building & construction, furniture & bedding, packaging, and automotive among others. The foam plastics market is projected to grow from USD 51.6 billion in 2020 to USD 65.4 billion by 2025, at a CAGR of 4.8% between 2020 and 2025. APAC is the largest consumer of foam plastics. The overall growth of the market is triggered by the growth of major end-use industries of foam plastics and energy sustainability and energy conservation properties of foam plastics.

To know about the assumptions considered for the study download the pdf brochure Recent Developments

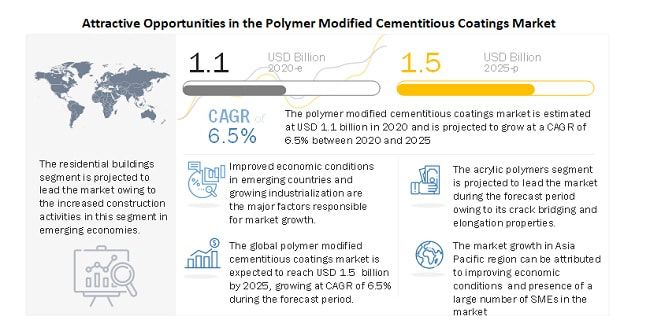

APAC is the leading market for foam plastics. The growth in the region is fueled by the booming economies of China, India, Indonesia, and Vietnam. PU resin based foams are the preferred choice in the building & construction industry in APAC. It is in high demand, as it is a low-cost material that provides low heat conduction coefficient, low density, low water absorption, relatively good mechanical strength, and good insulating properties. APAC is a rapidly developing region with growth opportunities for companies willing to invest in high-growth markets. The key players profiled in the foam plastics market report are BASF SE (Germany), Covestro (Germany), Huntsman International LLC (US), The Dow Chemical Company (US), and Wanhua Chemical Group Co., Ltd. (China).  The polymer modified cementitious coatings market is estimated at USD 1.1 billion in 2020 and is projected to reach USD 1.5 billion by 2025, at a CAGR of 6.5% from 2020 to 2025. The residential segment is estimated to lead the polymer modified cementitious coatings market in 2020, owing to The growing urbanization and migration of people from rural areas to urban cities are important factors driving the housing sector. Rising government initiatives to support infrastructure development and construction activities in emerging countries of the Asia Pacific region offer lucrative growth opportunities to manufacturers of polymer modified cementitious coatings. The recent outbreak of the COVID-19 pandemic and its rapid spread across the world has led to economic disruption and has brought down construction activities. Trade, travel, retail, and manufacturing activities have been affected, and the production of construction chemicals has come to a standstill during the first three months of 2020 and is expected to continue till the second quarter of 2020.

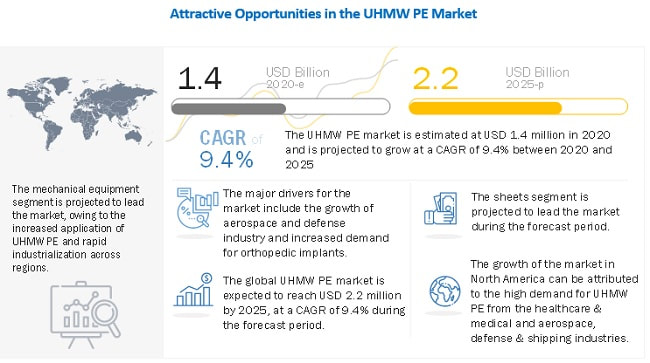

The polymer modified cementitious coatings market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific polymer modified cementitious coatings market in 2019. The Asia Pacific region is an emerging and lucrative market for polymer modified cementitious coatings, owing to industrial development and improving economic conditions. This region constitutes approximately 60% of the world’s population, and thus leads to the wide-scale use of polymer modified cementitious coatings for waterproofing applications in residential and non-residential buildings, and public infrastructure. Outbreak of COVID-19 from China and the impact of coronavirus in Japan, South Korea, Australia, and India has caused a decrease in the consumption of polymer modified cementitious. To know about the assumptions considered for the study download the pdf brochure Major companies such as Arkema S.A. (France), Sika AG (Switzerland), Akzo Nobel N.V. (Netherlands), MAPEI S.p.A. (Italy), Compagnie de Saint-Gobain S.A. (France), and Fosroc International Limited (UAE) , Dow, Inc. (US) and H.B. Fuller Company (US) The Lubrizol Corporation (US), Organik Kimya Sanayi Ve Ticaret A.S. (Turkey), Pidilite Industries Limited (India), GCP Applied Technologies Inc. (US), Berger Paints India Limited (India), W. R. Meadows, Inc. (US), Evercrete Corporation (US), Indulor Chemie GmbH (Germany), The Euclid Chemical Company (US) and others are key players in the polymer modified cementitious coatingsmarket. These players have been focusing on developmental strategies, such as expansions, acquisitions, partnerships, joint veture, and new product developments, which have helped them expand their businesses in untapped and potential markets. Arkema S.A. (France) is one of the leading producers of specialty chemicals and advanced materials in the world. The company offers its products to various industries, such as construction, packaging, chemical, automotive, electronics, food, and pharmaceuticals. It offers cementitious coating products through its subsidiary, Bostik. The subsidiary provides construction products based on polymer modified cementitious binders including tile adhesives and grouts, floor screeds, and leveling compounds. The company adopts growth strategies to increase its market share. For instance, in December 2018, The company acquired LIP Bygningsartikler AS (LIP), the Danish leader in tile adhesives, waterproofing systems, and floor preparation solutions through its subsidiary, Bostik. With this acquisition, the company is able to meet customer demand in the Nordic countries. Akzo Nobel N.V. (Netherland) is a leading producer of paints & coatings and specialty chemicals. The company operates through two segments, namely, Performance Coatings and Decorative Paints. It offers cementitious coating products under its Performance Coatings segment which produces automotive and aerospace; industrial; marine and protective; and powder coatings. The company offers products for various end-use industries, such as building & infrastructure, transportation, and consumer goods. . The company has halted its production lines and suspended their financial expectations for 2020 due to significant market disruption resulting from the Covid-19 pandemic. This has impacted the company’s operations across the globe and is expecting improvements from the second quarter in most of the countries. Compagnie de Saint-Gobain S.A. is one of the major players in the construction chemical industry with a strong foothold in Europe and North America. The company currently focuses on strengthening its position of polymer modified cementitious coatings in the Asia Pacific region by adopting growth strategies. For instance, the company partners with SCG Cement-Building Materials in Thailand to develop a modular bathroom solution that incorporates Saint-Gobain Weber tiling and waterproofing solutions. This has helped the company to establish its presence in Thailand and strengthen its position in the Asia Pacific region. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=251464560  The ultra-high molecular weight polyethylene (UHMW PE) market is estimated at USD 1.4 billion in 2020 and is projected to reach USD 2.2 billion by 2025, at a CAGR of 9.4% from 2020 to 2025. Ultra-High Molecular Weight Polyethylene (UHMW PE) is a simple linear background polyethylene possessing unique properties. Due to its ultra-high molecular density, it provides high abrasion resistance and impact strength in comparison to other engineering polymers. Apart from this, the material can also be optimized for more application specific requirements such as noise resistance, low coefficient of friction, excellent chemical resistance, self-lubrication, bio-compatibility, wear resistance, and electric insulation resistance.

To know about the assumptions considered for the study download the pdf brochure Recent Developments

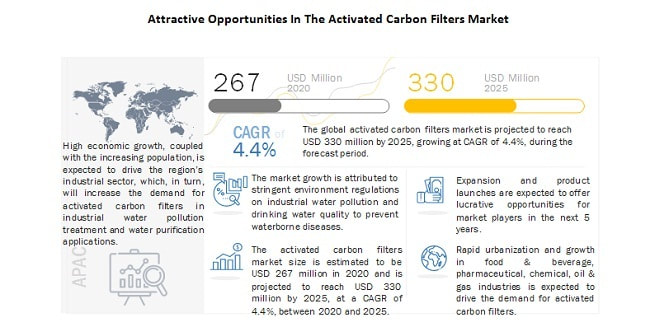

Major companies such as Celanese Corporation (US), Koninklijke DSM N.V. (Netherlands), LyondellBasell Industries N.V. (Netherlands), Braskem S.A (Brazil), Asahi Kasei Corporation, (Japan) Du Pont De Nemours Inc. (US), Saudi Arabia Basic Industries Corporation (Saudi Arabia), Mitsui Chemicals, Inc. (Japan), Honeywell International, Inc. (US), and Teijin Limited (Japan) and others are key players in the UHMW PE market. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=257883188 Activated Carbon Filters Market- Analysis of Potential Market Opportunity Worth $330 million by 20253/16/2022  The activated carbon filters market size is projected to grow from an estimated value of USD 267.3 million in 2020 to USD 330 million by 2025, at a CAGR of 4.4% during the forecast period. The growth in activated cabon filters market is attributed to the stringent regulation on industrial discharge to control water pollution and regulations drinking water quality standards to control water borne dieases. The market growth is also attributed to the rapid urbanization and growth in industrial, food & beverage, pharmaceutical applications. One of the emerging applications of activated carbon filters is gas separation. Activated carbon filters are used to separate components of gas through pressure swing adsorption phenomena (PSA).

Stainless steel shell is the fastest-growing segment of activated carbon filters market Stainless steel shell was the largest segment of the activated carbon filters markets globally in 2019 in terms of value. The stainless steel shell is anticipated to account for the biggest share of the overall activated carbon filters market during the forecast period. The growth of stainless steel shell activated carbon filters is attributed to its durability and less-corrosive properties. Carbon steel shell activated carbon filters are less durable because of its corrosive nature. To know about the assumptions considered for the study download the pdf brochure Industrial water pollution treatment is the largest application of activated carbon filters market The industrial water pollution treatment application is expected to be the largest, and drinking water purification application is expected to be the fastest-growing segment in the overall market. The global activated carbon filters market is mainly driven by the implementation of stringent regulations by regional governments and environmental agencies to control water pollution. Also, activated carbon filters are used to treat industrial discharge to re-use it in the manufacturing rocess again. Re-use of industrial discharge water and water pollution control are the two major making industrial water pollution treatment the largest application in the market. APAC is the largest as well as the fastest-growing market for activated carbon filters market. APAC is estimated to be the largest market for activated carbon filters in 2019. The market for this region is segmented into China, India, Japan, Malaysia, Indonesia, and the Rest of APAC. According to the World Bank, APAC is the fastest-growing region in terms of both population and economy. The region has witnessed significant growth in the past decade, accounting for over one-third of the world’s GDP. High economic growth, coupled with the increasing population, is expected to drive the region’s industrial sector. This is expected to increase the demand for activated carbon filters in water pollution treatment and water purification applications. The key companies profiled in this report on the activated caron filters market include TIGG LLC (US), Puragen Activated Carbons (US), Cabot Corporation (US), Westech Engineering (US), Kuraray Co. Ltd. (Japan), Lenntech B.V. (The Netherlands), Donau Carbon Corporation (Germany), General Carbon Corporation (US), Sereco S.R.L. (Italy), Carbtrol Corp (US). TIGG LLC (US) is one of the leading players in the activated carbon filters market and a subsidiary of Newterra Ltd. The company offers a wide range of standard and custom made granular activated carbon adsorption and filtration systems. It provides filtration equipment for liquid and vapor treatment solutions for industrial manufacturing, municipal water treatment, air filtration, water filtration, environmental remediation application, and activated carbon & media exchange services. It is fully certified with ASME code shop and has both National R and ASME U stamp certifications. Puragen Activated Carbons (US) is one of the major players in the activated carbon filters market. The company provides activated carbon filters under the brand name OxGuard. Its high-grade carbon steel filtration vessel, meets material standards of FDA (Food & Drug Authority), EPA (Environmental Protection Agency), and AWWA (American Water Works Association). The company provides activated carbon filtration equipment to a wide variety of markets and applications, such as water filtration, air filtration, chemical manufacturing, decolorization and impurity removal in food & beverage, and pharmaceutical industries. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=213859954 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed