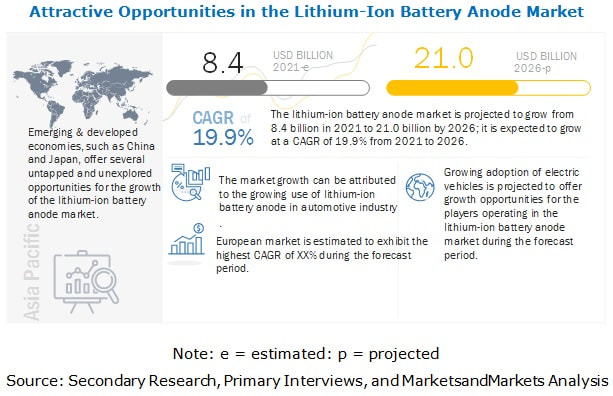

The global lithium-ion battery anode market size is projected to grow from USD 8.4 billion in 2021 to USD 21.0 billion by 2026, at a CAGR of 19.9% from 2021 to 2026. The growing demand for electric vehicles along with the high demand for lithium-ion batteries for industrial applications is driving the market growth. Moreover, strategies such as agreements and plant expansions undertaken by several prominent players in the lithium-ion battery anode industry are further fueling the lithium-ion battery anode industry growth across the globe.

To know about the assumptions considered for the study download the pdf brochure The pandemic is estimated to have an impact on various factors of the value chain of the lithium-ion battery anode market, which is expected to reflect during the forecast period, especially in the year 2020 to 2021. The various impact of COVID-19 are as follows: IMPACT ON LITHIUM-ION BATTERY ANODE: The outbreak of the COVID-19 pandemic has resulted in the temporary shutdown of production plants and related activities in most of the major economies across the globe. Besides, it has slow down the growth of various sectors as most of the countries worldwide have resorted to nationwide lockdown as a measure to control the spread of the virus. This has resulted in disruptions in the global supply chains and consequently affected the growth of the various industries such as automotive, marine, and energy storage attributed to the shortage of raw materials and other inputs. Likewise, limited transportation, travel restrictions, and halt of manufacturing activities have hampered the growth of the lithium-ion battery anode market, and the purchase and usage patterns have changed drastically, which has reduced the sales of various lithium-ion battery materials. The automotive end-use segment is projected to lead the global lithium-ion battery anode market during the forecast period. The automotive end-use industry is expected to be one of the major segments for lithium-ion battery anode market. Battery-driven vehicles such as electric vehicles, e-bikes, and automated guided vehicles, are major consumers of lithium-ion batteries. There is increasing competition between battery models installed in EVs owing to the need for operational excellence. Increasing adoption and awareness of EVs supports the growth of the lithium-ion battery market which in turn enhances the demand for lithium-ion battery anode. Europe lithium-ion battery anode market is projected to grow at the highest CAGR Europe is the second-largest consumer of lithium-ion battery anode and accounted for a share of 6.1% of the global market, in terms of value, in 2020. The region is home to some of the largest battery manufacturers, such as Saft (France) and FIAMM (Italy). Batteries have major applications as clean, sustainable, and compact sources of power in automotive. The region is witnessing significant growth in the demand for EVs which is largely dependent on government incentives and funds. Growth in demand for electric vehicle has increased the demand for lithium-ion battery anode which in return has fueled the demand for lithium-ion battery anode in the region. The key players in the lithium-ion battery anode market include Showa Denko Materials (Japan), JFE Chemical Corporation (Japan), Kureha Corporation (Japan), SGL Carbon (Germany), Shanshan Technology (China), and POSCO CHEMICAL (South Korea). The lithium-ion battery anode market report analyzes the key growth strategies adopted by the leading market players between 2017 and 2021, which include expansions, investments, and mergers & acquisitions. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=147095907

0 Comments

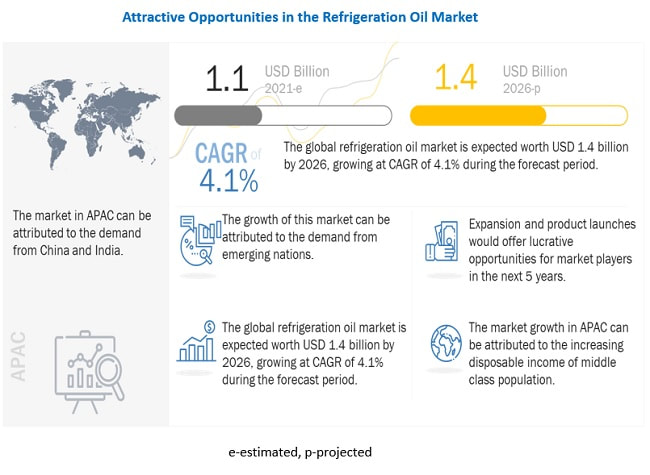

The report “Refrigeration Oil Market by Type (Synthetic Oil (POE, PAG), Mineral Oil), Application (Refrigerators & Freezers, Air conditioner, Automotive AC System, Aftermarket), & Region(APAC, North America, South America, Europe, & MEA) – Global Forecasts to 2026″, is projected to reach USD 1.4 billion by 2026, at a CAGR of 4.1% from USD 1.1 billion in 2021. This growth is primarily triggered by the increasing demand from the refrigerator & freezer, air conditioner, and automotive AC system applications. APAC is the largest refrigeration oil market due to a rise in the manufacturing of consumer appliances and automobiles. Furthermore, the changing lifestyle of consumer and rising income levels have led to higher demand for refrigerators & freezers and air conditioners, which, in turn, drives the refrigeration oil market. The growing demand for perishable food products along with growth in the pharmaceutical industry also drives the demand for refrigerators & freezers, fueling the growth of the refrigeration oil market.

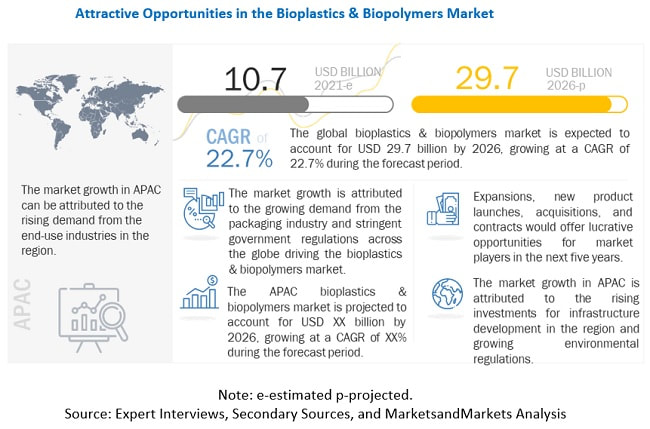

Browse 213 market data Tables and 58 Figures spread through 226 Pages and in-depth TOC on “Refrigeration Oil Market by Type (Synthetic Oil (POE, PAG), Mineral Oil), Application (Refrigerators & Freezers, Air conditioner, Automotive AC System, Aftermarket), & Region(APAC, North America, South America, Europe, & MEA) – Global Forecasts to 2026” View detailed Table of Content here – https://www.marketsandma rkets.com/Market-Reports/refrigeration-oil-market-126068118.html Synthetic oil is the largest oil type of refrigeration oil market. Synthetic oil accounted for the largest share of the overall refrigeration oil market, in terms of value, in 2020. Synthetic oil is manufactured by combining synthetic base oils and additives. It has several advantages over conventional mineral oil due to its high performance in extreme conditions, better viscosity index, higher shear stability, and improved chemical resistance. In addition, its compatibility with low GWP and modern refrigerants gives them an added advantage over mineral oil. Refrigerators & Freezers is estimated to be the largest application of the refrigeration oil market during the forecast period. To know about the assumptions considered for the study download the pdf brochure Refrigerator & freezer is the largest application of refrigeration oil. This growth is attributed to the rising demand for perishable food items and changing the lifestyle of people in developed and developing regions. Refrigeration oil is used in domestic, commercial, and industrial refrigerators & freezers. In addition, the growing demand for refrigerated food products and increasing trade of food products are driving the refrigeration oil market in the refrigerator & freezer application. APAC is estimated to be the largest market for refrigeration oil during the forecast period. APAC is the largest market for refrigeration oil, followed by North America and Europe. APAC dominates the refrigeration oil market due to the rapid economic growth, particularly in the consumer goods and automobile industries in the region. The rapid urbanization in APAC, coupled with the improved living standard is driving the refrigeration oil market. The advantage of shifting production to the Asian region is that the cost of production is low here. Also, it is easier to serve the local emerging market. Also, due to the massive production and demand for consumer appliances and automobiles in countries such as China, Japan, India, and South Korea. This high growth is attributed to the growing manufacturing of consumer goods and automobile in the region. The key market players profiled in the report include Eneos Holdings Inc. (Japan), BASF SE (Germany), Idemitsu Kosan Co. Ltd (Japan), ExxonMobil Corporation (U.S.), Royal Dutch Shell Plc. (Netherlands), Total Energies SE(France), China Petrochemical Corporation (Sinopec Corp), Petroliam Nasional Berhad(Petronas), FUCHS Petrolub SE (Germany), Johnson Controls(Ireland) among others. Don’t miss out on business opportunities in Refrigeration Oil Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The report “Bioplastics & Biopolymers Market by Type (Non-Biodegradable/Bio-Based, Biodegradable), End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture), Region – Global Forecast to 2026″, global bioplastics & biopolymers market size is projected to grow from USD 10.7 billion in 2021 to USD 29.7 billion by 2026, at a CAGR of 22.7% between 2021 and 2026. Bioplastics are plastics derived from renewable sources such as corn, potatoes, rice, soy, sugarcane, wheat, and vegetable oil, while biopolymers are naturally occurring polymers. Bioplastic may or may not be biodegradable. Bioplastics are mainly segmented into biodegradable and non-biodegradable plastics for various applications in packaging, consumer goods, automotive & transportation, agriculture & horticulture, medical, and other end-use industries.

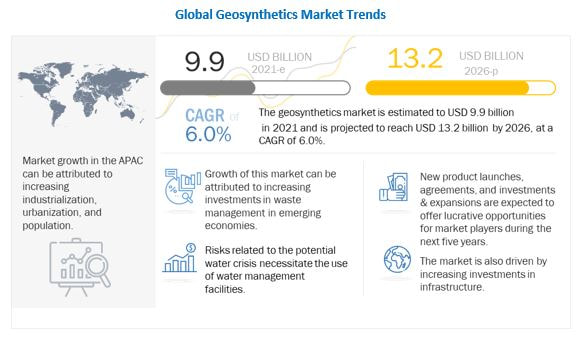

Browse 142 market data Tables and 50 Figures spread through 244 Pages and in-depth TOC on “Bioplastics & Biopolymers Market by Type (Non-Biodegradable/Bio-Based, Biodegradable), End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture), Region – Global Forecast to 2026” View a detailed Table of Content here – https://www.marketsandmarkets.com/Market-Reports/biopolymers-bioplastics-market-88795240.html Biodegradable bioplastics & biopolymers types will account for the major share of the market in terms of value Biodegradable are the largest type segment in terms of value during the forecast period. Biodegradable polymers are high molecular weight compounds that decompose naturally in the environment through bacteria and other microorganisms during a span of time. The process produces natural byproducts, such as biomass, water, gases, and inorganic salts. Biodegradable polymers are made from renewable sources such as corn oil, starch, orange peels, and plant materials and deteriorate into natural by-products. The growing concerns related to environmental pollution and non-renewable finite petroleum resources are leading to the increasing use of biodegradable bioplastics & biopolymers. In terms of value, the packaging segment is projected to account for the largest share of the bioplastics & biopolymers market, by end-use industry, during the forecast period. Packaging is one of the end-use industries that dominate the bioplastics & biopolymers market. Bioplastics, and especially biodegradable bioplastics, have increasing demand to replace conventional plastics to address environmental concerns. The use of bioplastics is increasing in applications such as bottles, films, clamshell cartons, waste collection bags, carrier bags, mulch films, and food service ware. APAC is estimated to be the fastest-growing market for bioplastics & biopolymers between 2021 and 2026. APAC is estimated to be the fastest-growing market for bioplastics & biopolymers between 2021 and 2026. Growth in APAC is primarily attributed to the fast-paced expansion of the economies such as China, India, and Indonesia. Growing population increased consumer spending, and rapid industrial expansion are the major factors responsible for the high growth rate of the region. Growing environmental concern and awareness along with increasing regulations are the key factors driving the demand for bioplastics & biopolymers. The manufacturers focus on the high-growth market to gain market share and increase their profitability. The key players in this market are NatureWorks (US), Braskem (Brazil), BASF (Germany), Total Corbion (Netherlands), Novamont (Italy), Biome Bioplastics (UK), Mitsubishi Chemical Holding Corporation (Japan), Biotec (Germany), Toray Industries (Japan), and Plantic Technologies (Australia). Don’t miss out on business opportunities in Bioplastics & Biopolymers Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  Geosynthetics are largely used in waste management, and infrastructure development applications such as railroads, roadways, soil reinforcement and stabilization, heap leach pads, landfills, and containment sites. The basic functions of geosynthetic materials are separation, reinforcement, filtration, drainage, and barrier. The increasing spending on infrastructural development and demand for waste management is expected to offer opportunities for manufacturers during the forecast period.

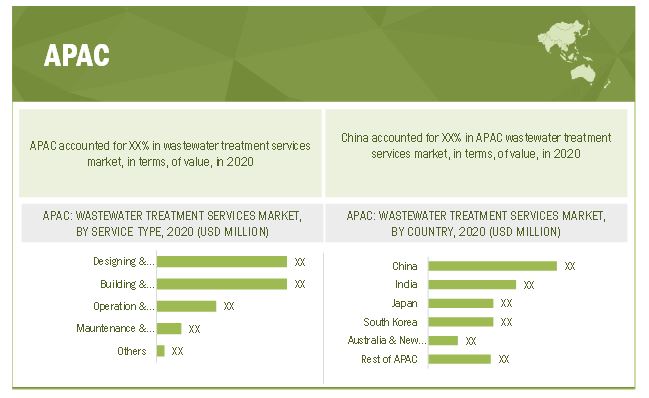

COVID-19 pandemic has significantly disrupted the global construction sector in 2020, with projects being halted due to lockdown restrictions owing to the non-availability of workforces, supply chain disruptions, country-wide lockdowns, and temporary closures of infrastructure projects, and limited availability of raw materials. Companies have witnessed lower demand for new office spaces, shops, and others which resulted in a decline in revenue. However, due to the easing of the norms by the government with preventive measures such as social distancing and relief funds, the end-use industries are recovering. Moreover, the construction sector was exempted from the lockdown restrictions in a few countries such as Australia as it falls under essential services. In Indonesia, preventive lockdown measures hampered supply chains, and delays in infrastructure projects are major reasons for the decline in the construction industry in the country. The US construction industry was affected majorly due to the limited availability of raw materials as the imports from various other countries such as China were restricted due to the pandemic. However, stimulus package by various government globally has helped the countries to support the declining economy, which is also expected to support the construction industry and lead to economic recovery post the COVID-19 crisis by boosting infrastructural growth. To know about the assumptions considered for the study download the pdf brochure The global geosynthetics market is projected to reach USD 13.2 billion by 2026 from USD 9.9 billion in 2021, at a CAGR of 6.0% between 2021 and 2026 The rising demand for geosynthetics is majorly due to Increasing investments in infrastructural developments, and rising concerns over waste and water management globally. Market growth is largely driven by the increasing population and urbanization, coupled with increasing industrial activities in the APAC and South America which is expected to offer opportunities for manufacturers during the forecast period. Developments in the field of material technology, and growing demand for sustainable products are presenting opportunities for the geosynthetics market. Geosynthetics market is dominated by APAC in 2020. The region is growing at a faster rate which accounts for the high growth of the geosynthetics market. The emerging market of India, China, and other countries of the APAC are growing and boosting the regional market growth. Rapidly increasing population, urbanization, and industrialization are expected to drive the geosynthetics market in APAC. Rising investment In the development of public infrastructure and growing demand for solid waste management system are the major factors driving the geosynthetics demand in the region. Key players in the geosynthetics market are SOLMAX (Canada), NAUE GmbH & Co. KG (Germany), Officine Maccaferri Spa ( Italy), Berry Global Inc ( US), and Agru America, Inc ( US) are the major players in the market. Read More: https://www.marketsandmarkets.com/ResearchInsight/geosynthetic-market.asp  The wastewater treatment services market is projected to reach USD 71.6 billion by 2026, at a CAGR of 6.2% from USD 53.0 billion in 2021.

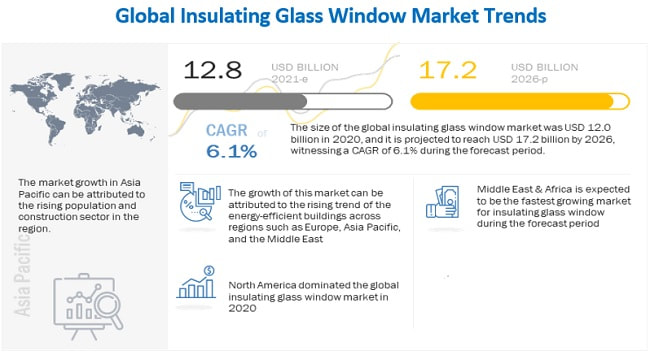

Growing population, expanding manufacturing industry, urbanization, and regulatory requirements are the major drivers of the wastewater treatment services market. Initiatives by manufacturing industries and state bodies for low waste generation and growing awareness about new water treatment technologies are some of the factors which are likely to boost the wastewater treatment services market. The growing population of the world is fueling the demand for new wastewater treatment plants and services. Industrial growth is boosting the demand for new wastewater treatment projects. Collectively, the growth in demand for new wastewater treatment plants is pushing the demand for building and installation services market, globally. Continuous operation of the wastewater treatment plant is a major concern in both the manufacturing as well as other industries. To know about the assumptions considered for the study download the pdf brochure The key players in the market are focusing on strategies, such as new product launches, partnerships & agreements, acquisitions, and expansions, to expand their businesses globally The key players operating in the wastewater treatment services market are trying to increase their scope of services to address the increasing demand. Veolia Water Technologies (France), SUEZ (France), Xylem (US), Evoqua Water Technologies (US), Thermax (India), and Ecolab (US) are the leading providers of wastewater treatment services, globally. Players in the wastewater treatment services market are mainly concentrating on new product launches, acquisitions, and collaborations to meet the growing demand for various end-use industries. New product launches help companies to strengthen their product portfolio and meet the specific demands of customers. The growth of the wastewater treatment services market has been largely influenced by new product launches that were undertaken between 2016 and 2020. Companies such as Xylem Inc and Suez Group have adopted new product launches to enhance their market position. Veolia Group designs and manages water services, wastewater treatment, and recovery services for local authorities and industrial customers. The company operates through three business segments, namely, water, waste, and energy. Veolia Water business segment provides the complete range of services required to design, build, maintain, and upgrade water and wastewater treatment facilities and systems for industrial customers and public authorities. It offers a wide range of solutions for the collection and transport of drinking water and wastewater, which includes operating and maintaining water and wastewater treatment networks, collecting wastewater, and designing and building water and sanitation networks. The company operates in Europe, the Americas, Asia, Oceania, the Middle East, and other regions. In October 2020, Veolia Group acquires 30% shares of Suez’s capital from Engie to enhance its water business segment in France. Ecolab provides water, hygiene, and energy technologies and services across the globe. The company operates through four segments, namely, global industrial, global institutional & specialty, and global healthcare & life sciences and others. Ecolab provides wastewater treatment services through its global industrial business segment. The water unit under the global industrial segment offers water treatment and process applications, and cleaning and sanitizing solutions primarily to industrial customers within the manufacturing, food and beverage processing, chemical, primary metals, power generation, pulp and paper, mining, and commercial laundry industries. Read More: https://www.marketsandmarkets.com/PressReleases/wastewater-treatment-service.asp  The insulating glass window market size was USD 12.0 billion in 2020 and is projected to reach USD 17.2 billion by 2026; it is expected to grow at a CAGR of 6.1% from 2021 to 2026. The increasing demand for energy-efficient buildings in various regions is expected to drive the growth of this market. The commercial segment accounted for the largest share of the insulating glass window market in 2020, owing to the increasing rate of commercial building construction in the countries such as the US, Germany, China, and India.

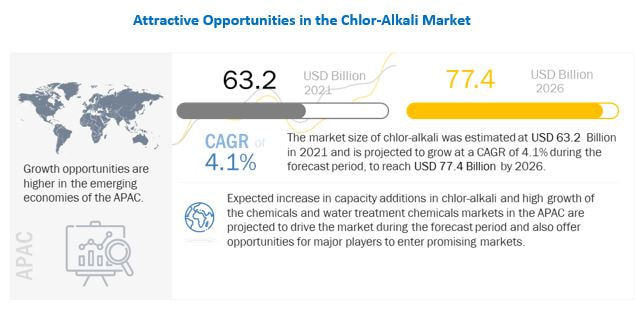

To know about the assumptions considered for the study download the pdf brochure The high energy consumption in buildings is propelling the demand for energy-efficient building materials such as insulating glass windows. The usage of insulating glass windows can help reduce energy losses and result in lower energy consumption, which is a crucial requirement. The heat and light transferred through the glass directly impact the comfort level of the people in the room, apart from affecting the energy costs. Switching to insulating glass windows makes a huge difference in the overall energy consumption. The use of insulating glass windows in residential and commercial buildings can reduce power consumption by almost 50%, thereby proving to be an effective technology for power optimization. Also, the growing trend of rating systems in various countries, such as LEED (Leadership in Energy & Environmental Design) in the US, IGBC Green Ratings in India, and others are likely to contribute to the growth of the insulating glass window market. North America is expected to dominate the insulating glass window market from 2021 to 2026 North America is projected to be the largest regional market for insulating glass windows. The market in North America is driven by moderate growth in the construction industry. Glass insulation is considered a viable option for making buildings energy-efficient. Also, factors such as the high quality of infrastructural construction, reduced environmental impact, climatic conditions, and government regulations are fueling the growth of energy-efficient windows in North America. The key market players include AGC Inc. (Japan), Central Glass Co., Ltd. (Japan), Compagnie de Saint-Gobain SA (France), Dymax (US), Glaston Corporation (Finland), Guardian Glass (US), H.B. Fuller Company (US), Henkel AG & Co. KGaA (Germany), Internorm (Austria), Scheuten (Netherlands), Nippon Sheet Glass Co., Ltd. (Japan), Sika AG (Switzerland), 3M (US), Viracon (US). These players have adopted product launches, acquisitions, expansions, agreements, contracts, partnerships, investments, collaborations, and divestments as their growth strategies. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=36258309  The growing industrialization in emerging economies such as China, India, South Korea, Indonesia, Thailand, Taiwan, Mexico, Brazil, and Argentina is expected to drive the chlor-alkali market during the next five years. The high demand for packaging, building & construction, consumer goods, and automotive applications in these countries increases the need for plastics, aluminum, and others used in these applications. Government policies supporting the growth of industries, low labor costs, skilled workforces, availability of raw materials, and increasing urbanization have enabled domestic and foreign companies to establish their facilities in these countries. The growth of the manufacturing industry in Malaysia, Vietnam, Colombia, and Chile is also expected to fuel market growth.

The market for plastics is dominated by the US, China, India, and Germany, among others. Brazil, China, South Africa, and Argentina, among other emerging countries, offer significant growth opportunities for the chlor-alkali market. Increasing economic activities such as rapid industrialization and urbanization are driving the demand for plastics in emerging countries. For instance, the construction industry contributes 10.0% to India’s GDP. End-use industries including automobile, construction, packaging, consumer goods, and medical & pharmaceutical are rapidly growing in these countries. To know about the assumptions considered for the study download the pdf brochure The GDP of these emerging economies acts as a major indicator for the growth of the chlor-alkali market, as it represents the growth of the economy and per capita consumption. Due to the increase in GDP, the per capita income and spending power of the population also increases, which results in higher per capita plastic consumption in these countries. Thus, the growth of the demand for chlor-alkali can be attributed to the increasing per capita plastic consumption, which, in turn, is providing opportunities to market players in these countries. In recent years, the chemical industry has witnessed high growth in emerging regions and steady growth in developed/mature markets. Industry participants are keen on addressing the needs/demands of growing economies. Global players have adopted expansion strategies to enhance their production capacities. Key market players are adopting expansion and joint ventures strategies to enhance their market competitiveness and increase penetration in different regions. Chemical industries in the US and Europe are mature and their growth is largely influenced by the GDP growth of these regions. The trend in rapid industrialization, supported by strong demand due to improving standards of the living, significant population base, and available pools of workforces in the APAC, Middle East & Africa, and South America has led companies to establish their facilities in these regions and cater to regional demands. The global Chlor-Alkali market size is estimated to be USD 63.2 billion in 2021 and is projected to reach USD 77.4 billion by 2026, at a CAGR of 4.1% between 2021 and 2026. The leading players in the Chlor-Alkali market are Olin Corporation(US), Westlake Chemical Corporation (US), Tata Chemicals Limited (India), Occidental Petroleum Corporation (US), Formosa Plastics Corporation (Taiwan), Solvay SA (Belgium), Tosoh Corporation (Japan), Hanwha Solutions Corporation (South Korea), Nirma Limited (India), AGC, Inc. (Japan), Dow Inc. (US), Xinjiang Zhongtai Chemical Co. Ltd. (China), INOVYN (UK), Ciner Resources Corporation (US), Wanhua-Borsodchem (Hungary), and others. Read More: https://www.marketsandmarkets.com/PressReleases/chlor-alkali.asp |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed