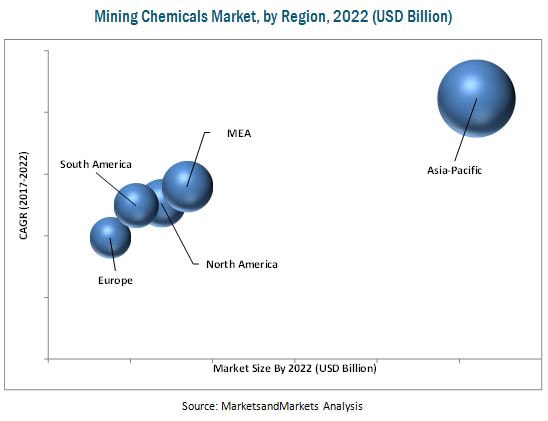

The mining chemicals market size is estimated to grow from USD 6.02 Billion in 2017 to USD 7.54 Billion by 2022, at a CAGR of 4.60%. The mining chemicals market is witnessing considerable growth due to the rise in industrialization and infrastructural development. High demand for mining chemicals is primarily attributed to increasing complexity of ores and decreasing ore grades. The mining chemicals industry has come across new opportunities due to the growing stringent government regulations on wastewater pollution, coupled with the rising demand for quality minerals.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=205253671 Mining chemicals also finds wide application in mineral processing. This is due to the rising demand for concentrated grade minerals. As per International Mining Equipment (IME) 2017, mineral processing will witness a significant rise due to the high growth of the mining sector, in terms of production of minerals. Mining chemicals are consumed in the wastewater treatment application for intercepting, diverting, and recycling the water. High demand for mining chemicals in water & wastewater treatment can be attributed to the stringent environment and legislative regulations on toxic discharge in water bodies initiated by governments of countries such as the U.S. In 2016, the Asia-Pacific market accounted for the largest share of the global mining chemicals market, followed by Europe and North America. Countries such as China and Japan are expected to witness high growth in the mining chemicals market due to rapid economic expansion. The positive outlook of the economies is attracting huge investments from global mining companies. As a result, the mining capacity of various metals and minerals is increasing, thereby boosting the demand for mining chemicals. The major players in the Mining chemicals market include AkzoNobel N.V. (Netherlands), BASF SE (Germany), Clariant AG (Switzerland), Cytec Industries Inc. (U.S.), Kemira OYJ (Finland), The Dow Chemical Company (U.S.), Huntsman International LLC (U.S.), Orica Limited. (Australia), ArrMaz Products, L.P. (U.S.), and SNF Floreger (France). Speake to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=205253671

0 Comments

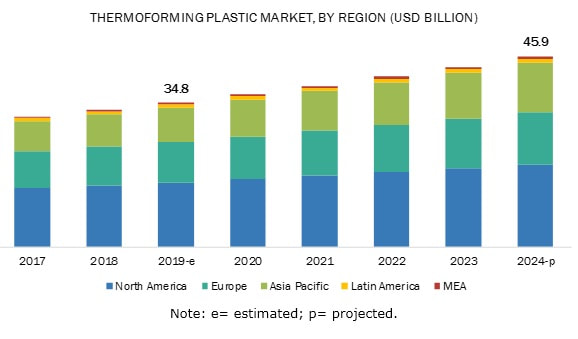

The thermoforming plastic market size is growing due to the rising healthcare & pharmaceuticals and food & agriculture packaging industries and increasing manufacturing activities. Factors such as changing demographics and lifestyles have shifted the market toward e-retailing channels and convenient packaging, which in turn will drive the demand for thermoforming plastic. The thermoforming plastic industry is expected to grow from USD 34.8 billion in 2019 to USD 45.9 billion by 2024, at a CAGR of 5.7% during the forecast period.

Download PDF Brochure to Know More Food & agriculture packaging industry dominated the thermoforming plastic market in terms of value in 2018. This growth is attributed mainly to the huge demand for packaged and branded products. Thermoforming plastic provides better protection during transportation and uses safe packaging materials; hence, they are preferred in the food & agriculture packaging industry. North America is expected to lead the thermoforming plastic market Technological advancements in the packaging industry primarily drive the market in this region. The demand for thermoforming plastic will be driven by factors such as increasing electronic goods sales, high disposable income, increasing demand for packaged foods, and demographic changes. The region is characterized by continuous technological advancements in the thermoforming plastic industry with the presence of some key regional players such as Pactiv LLC, Sonoco Products Company, D&W Fine Pack LLC, Fabri-Kal Corporation, Sabert Corporation (US) and Dart Container Corporation. Sabert Corporation (US) is one of the prime manufacturers of thermoforming plastic in the North American region. Sabeart Corporation is a leading manufacturer of innovative food packaging products and solutions for food distributors, restaurants & caterers, grocery stores, national food chains, and consumer entertaining. The company provides a variety of food packaging for displaying, serving, & storing fine food. The company also recycles plastics going to landfill in Riverside, CA facility. The main products provided by the company include Catering Collection Packaging, Green Collection Packaging, Hot Collection Packaging, Cold Collection Packaging, and Bakery Collection Packaging. It is involved in implementing business strategies such as expansion, and acquisition to increase its market share around the globe. For instance, in February 2018, Sabert Corporation expanded its manufacturing facility, located in Greenville, Texas, for manufacturing 100% compostable packaging made from plant-based materials. This helped the company to deliver more options to its customers. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=97181143  Increasing demand for pneumatic tools in the construction and manufacturing end-use industries is fueling the growth of the compressor rental market. Even though, the mining equipment market was experiencing a lull over the past few years, it began to witness a positive trend, in terms of demand for mining equipment since 2015. Air compressors are best suited for heavy duty applications in mining operations. The revival of the mining equipment market is expected to have a positive impact on the growth of the compressor rental market during the forecast period. The compressor rental market is projected to reach USD 5.53 Billion by 2026, at a CAGR of 6.4% from 2016 to 2026.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=23430927 In the chemical industry, air compressors are used for transporting liquids under pressure. They are also used in pressurizing tanks, aeration tanks, and culture vessels for spot cooling and molding plastics. Air compressors find application in the automatic control systems used in the chemical industry. Besides air compressors, screw compressors are also commonly used in the chemical industry. Rapid growth of the chemical industry in the Middle East & Africa and Asia-Pacific regions is fueling the growth of compressor rental market. Technologically advanced air compressors are preferred as pneumatic power tools in commercial applications. They are used as jackhammers, pneumatic drills, pneumatic nail guns, and air saws, among others. Increasing demand for these pneumatic tools in the construction and manufacturing end-use industries is driving the demand for compressors, thereby fueling the growth of the compressor rental market. These key players operational in the compressor rental market are focusing on new product launches, expansions, and acquisitions to cater to the increasing demand for compressor rental from varied industries. Atlas Copco reported the largest number of developments in the compressor rental market between 2011 and 2016. In August 2016, Atlas Copco acquired Schneider Druckluft GmbH, a leading manufacturer of professional compressed air solutions with a large network of retailers. This acquisition is expected to strengthen position of Atlas Copco in the Germany compressor rental market. In May 2016, Atlas Copco acquired compressor business of Kohler Druckluft, which operates in Austria, Switzerland, and Liechtenstein. This acquisition resulted in Kohler Druckluft becoming part of the compressor technique business of Atlas Copco. This acquisition aims at improving customer interaction of the company in the central Europe. The company launched GA VSD+, which are oil-injected and oil-cooled rotary screw compressors. These new compressors are capable of reducing energy consumption to half as compared to traditional compressors. Consult with analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=23430927  The floor adhesive market is projected to grow from USD 8.54 Billion in 2017 to USD 11.01 Billion by 2022, at a CAGR of 5.2% from 2017 to 2022. The growth of the floor adhesive market is driven by advancements in flooring materials used in the residential, commercial, and industrial sectors. Epoxy and polyurethane floorings are widely used due to their high resistance to chemicals, temperature, and abrasion. These floorings are widely used in the healthcare, food, and automotive industries.

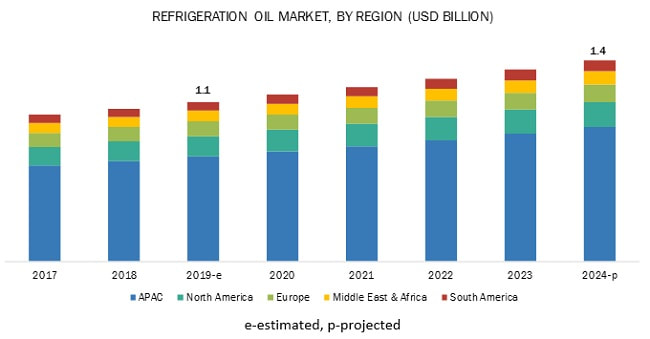

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=37475603 Epoxy adhesives consist of an epoxy resin and hardener. These adhesives are available in one-part, two-part, and film form. Epoxy adhesives form an extremely strong and durable bond with most materials. Toughened epoxy adhesives contain a dispersed physically separated but chemically attached rubber phase to improve fracture and impact resistance. The major reason for the increasing adoption of epoxy adhesives in the flooring industry is their capacity to provide a good balance of handling characteristics and superior physical properties. They adhere well to a wide variety of substrates. Based on application, the floor adhesive market has been segmented into tile & stone, carpet, wood, vinyl, and sports & rubber, among others. The growth of the tile & stone application segment is driven by the increasing infrastructural development in emerging countries across the globe. The floor adhesive market in Asia-Pacific expected to witness the highest growth during the forecast period. Emerging economies, such as China, India, South Korea, and various Southeast Asian countries are attracting several global players to establish their manufacturing base in Asia-Pacific. These manufacturers are competing to reach an extensive customer base in countries, such as China and India to cater to the increasing demand for adhesives from the residential and industrial sectors in these countries. Increased investments in infrastructural development in the region are expected to fuel the growth of the floor adhesive market in Asia-Pacific. Speak with analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=37475603  The refrigeration oil market size is projected to reach USD 1.4 billion by 2024 from USD 1.1 billion in 2019, at a CAGR of 4.7% between 2019 and 2024. The increasing demand for refrigerators & freezers from the food and pharmaceutical industries to preserve packaged food items and drugs is one of the major factors to drive the demand for the refrigeration oil market. Stringent regulations to limit the use of fluorocarbon refrigerants is restraining the growth of the refrigeration oil market.

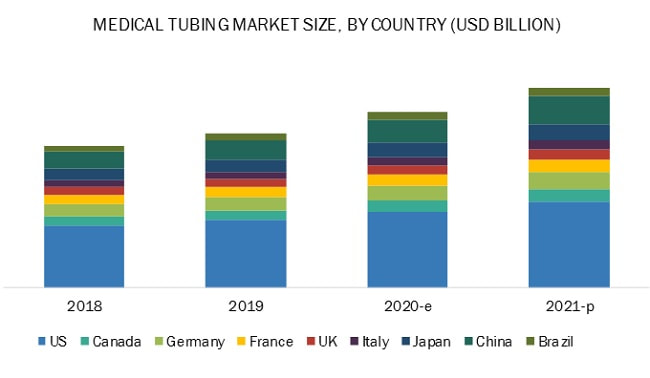

The APAC region is estimated to lead the refrigeration oil market in 2018 in terms of value and volume. The increasing population in the region and the rising demand for refrigerators, freezers, air conditioners, and automobiles in the emerging markets of APAC, such as China and India, are some of the major factors projected to drive the demand for refrigeration oil in the region. Furthermore, the improving lifestyle, increasing employment rate, rising disposable income of the people, and mounting foreign investments in various sectors of the economy are some of the other factors that make APAC an attractive market for refrigeration oil manufacturers. To know about the assumptions considered for the study download the pdf brochure On the other hand, increasing demand for consumer appliances drives the demand for refrigeration oil. The players in the refrigeration oil market are mainly concentrating on expansions, new product launches, and partnership & agreements to meet the growing demand in various applications. New product launches help companies strengthen their product portfolio and meet the specific requirements of customers. The growth of the refrigeration oil market has been influenced mainly by expansions, new product launches, and partnership & agreement that took place between 2016 and 2019. JXTG Group (Japan), BASF (Germany), and Idemitsu Kosan Co. (Japan), ExxonMobil Corporation (US), and Royal Dutch Shell plc. (Netherlands) adopted expansions, new product launches, and agreements to remain competitive in the refrigeration oil market. BASF is one of the world’s largest chemical companies and one of the world’s largest players in the refrigeration oil market. It engages in manufacturing and selling a wide range of chemicals and intermediate solutions. The company offers POE and PAG refrigeration oils. It focusses on joint ventures and expansions to remain competitive in the refrigeration oil market. In May 2019, the company expanded its production capacity of antioxidants for lubricants in China and Mexico due to the increasing global demand for long-life lubricant additives, which, in turn, will increase the demand for refrigeration oil. Idemitsu Kosan Co. is a petroleum refining and manufacturing company in Japan. The company has a major presence in APAC and manufactures and sells petrochemical and oil products. It offers PVE and PAG refrigeration oils to global customers. Idemitsu focuses on joint ventures, agreements, and expansions to remain competitive in the refrigeration oil market. In October 2017, the company started operating a service station business in Hanoi, Vietnam, that helped it strengthen its businesses ranging from production and procurement of petroleum products to the sale of such products in the overseas market of the Pacific Rim. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=126068118  The US medical tubing market size is projected to reach USD 2.9 billion by 2021, at a CAGR of 13.2%.The increase in demand for medical tubes in ventilators is the key factor driving the use of medical tubing. The rising demand for medical devices that incorporate medical tubing and the growing demand for ventilators in this pandemic are propelling the growth of the medical tubing market globally. However, factors such as restricting counterfeit products and fighting time for supply chain and logistics could affect the market growth.

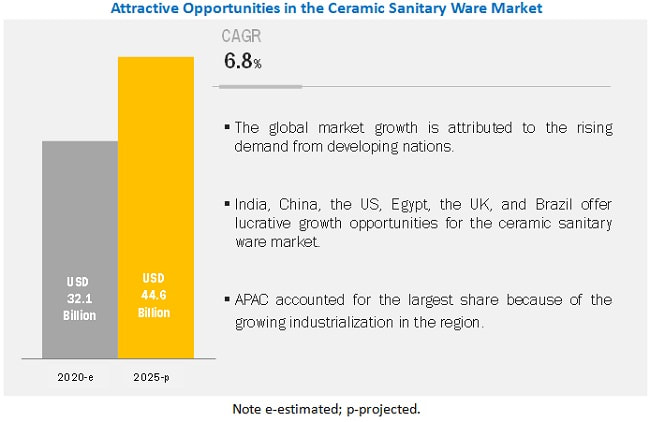

Zeus Industrial Products (US), Saint Gobain Performance Plastics (France), Teleflex (US), Optinova (US), and Lubrizol Corporation (Vesta) (US), among others, are the leading medical tubing manufacturers, globally. These companies have established their brands, and medical tubings produced by these companies are consumed domestically. They are also supplied to various countries such as China, Japan, UK, Italy, France, and others within the Asia Pacific region. To know about the assumptions considered for the study download the pdf brochure In February 2020, Teleflex Medical OEM acquired HPC Medical Products to strengthen its medical tubing & wire components and catheters portfolio. With this acquisition, the company is able to meet the growing demand in this pandemic situation. Now, the company is able to supply more products to the impacted countries with immediate effect to meet the growing demand. Lubrizol announced the continuous supply of flexible and biocompatible materials for vascular catheters, IV tube sets, and medical components used in ventilators, valves, and infusion pumps. In order to attain this, it has altered its production process to deliver more products which can serve the purpose during this COVID-19 pandemic. The company also ramped up the supply of ESTANE thermoplastic polyurethane (TPU) for a multitude of applications in this crucial time. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=165863042  The global ceramic sanitary ware market size is projected to reach USD 44.6 billion by 2025 from USD 32.1 billion in 2020, at a CAGR of 6.8%, during the same period. The changing lifestyle and increasing purchasing power of the middle-class population of developing countries are expected to support the growth of the ceramic sanitary ware market. However, fluctuation in housing demand is restraining the growth of the market. Technological advancements have created opportunities for manufacturers. LIXIL Group Corporation (Japan), TOTO Ltd. (Japan), Roca Sanitario SA (Spain), and Kohler Co. (US) are the major players in the ceramic sanitary ware market.

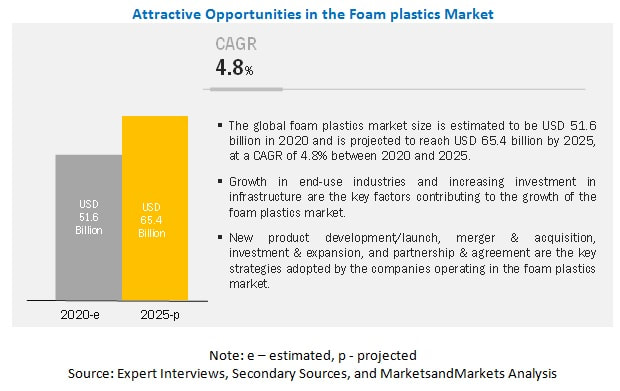

APAC is the largest market of ceramic sanitary ware, followed by Europe and North America. The massive industrial growth in APAC has been fueling the growth of the ceramic sanitary ware market over the past few years, which is expected to continue during the next five years. Domestic and foreign investments in key sectors, such as energy, manufacturing, construction, and mining, have been consistently growing over the past decade. It is expected to result in the growth of the industrial sector and the demand for ceramic sanitary ware in the country. To know about the assumptions considered for the study download the pdf brochure Over the past decade, India has been witnessing a moderate GDP growth. The country has attracted heavy investments in key industrial sectors, such as construction, cement, and energy. The economic outlook for India has been very optimistic. The Government of India is focused on the manufacturing sector by liberalizing policies and providing additional incentives, such as land at cheap rates and faster clearances from all the concerned departments. As a result, the overall economy is rapidly growing. This is expected to drive the sale of ceramic sanitary ware in the region during the forecast period. LIXIL Group Corporation (Japan) is one of the leading producers of ceramic sanitary ware. Expansion and new product development are the main strategies adopted by this organization. In August 2018, the company opened a new ceramic sanitary ware production plant in India with an investment of USD 65 million. Approximately 80% of the plant’s production will cater to the Indian market, and the remaining 20% will be exported to the global market. This development helped the company to expand its presence in the Indian market. In April 2019, the company launched two new bathroom collections under the brand name of INAX at Milan Design Week. This helped the company to meet the increasing demand from the global market. TOTO Ltd. (Japan) is another leading player in this market. The company launched high-end washlet bidet toilets in the global market. This new product is sold under the brand name or NEOREST NX. This helped the company to attract more customers. Roca Sanitario SA (Spain) is also a leading producer of ceramic sanitary ware. The company launched a new bathroom collection made from innovative designs. This collection offers sanitary wares with bold colors. This helped the company to strengthen its product portfolio. Kohler Co. (US) is also one of the leading producers of ceramic sanitary ware. In January 2020, the company introduced five new products, which include touchless faucets and touchless toilet technology, among others. This touchless technology provides flushing with sensors placed near the flush tank. These smart products provide comfort and hygiene to the user. Speak to Analyst : https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=581 Building & construction segment accounted for the largest share of the foam plastics market5/11/2021  Foam plastics are resins used in manufacturing polymer foams, which are used in various end-use industries such as building & construction, furniture & bedding, packaging, and automotive among others. The Foam plastics market size for is projected to grow from USD 51.6 billion in 2020 to USD 65.4 billion by 2025, at a CAGR of 4.8%. Foam plastics are largely used in building & construction, packaging, and furniture & bedding. The polyurethane segment is estimated to account for the largest share of the overall market due to its properties such as low heat conduction coefficient, low density, low water absorption, relatively good mechanical strength, and good insulating properties.

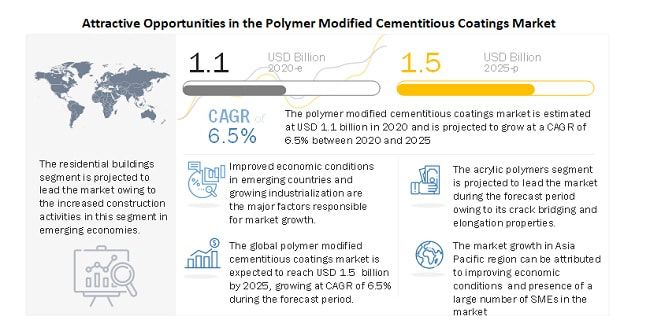

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=260352983 Foam plastics are used to make foams used in the building & construction industry for forging, doors, roof board, and slabs. PU is the dominant resin used in the building & construction industry for insulation. It has low heat conduction coefficient, low density, low water absorption, and relatively good mechanical strength and insulating properties, which are helpful in the building & construction sector. The COVID-19 pandemic has affected various end-use industries, and almost all divisions of the supply chain continue to be affected, which also includes the construction industry. According to the National Association of Home Builders (NAHB), US, the GDP growth rate during the first two quarters is expected to be negative. This decline can be compared to the aftermath of the global performance of the 2008 Great Recession. However, the fourth quarter of 2020 is expected to be a rebound period. Recent Developments In February 2020, Huntsman Corporation announced that it completed the acquisition of Icynene-Lapolla, a leading North American manufacturer and distributor of spray polyurethane foam (SPF) insulation systems for residential and commercial applications. Huntsman acquired the business from an affiliate of FFL Partners, LLC, for USD 350 million, subject to customary closing adjustments, in an all-cash transaction funded from available liquidity. APAC is the largest foam plastics market, globally. APAC is the leading market for foam plastics. The growth in the region is fueled by the booming economies of China, India, Indonesia, and Vietnam. PU resin based foams are preferred choice in the building & construction industry in APAC. It is in high demand, as it is a low-cost material that provides low heat conduction coefficient, low density, low water absorption, relatively good mechanical strength, and good insulating properties. APAC is a rapidly developing region with growth opportunities for companies willing to invest in high-growth markets. The key players profiled in the foam plastics market report are BASF SE (Germany), Covestro (Germany), Huntsman International LLC (US), The Dow Chemical Company (US), and Wanhua Chemical Group Co., Ltd. (China). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=260352983  The polymer modified cementitious coatings market is estimated at USD 1.1 billion in 2020 and is projected to reach USD 1.5 billion by 2025, at a CAGR of 6.5% from 2020 to 2025. The residential segment is estimated to lead the polymer modified cementitious coatings market in 2020, owing to The growing urbanization and migration of people from rural areas to urban cities are important factors driving the housing sector. Rising government initiatives to support infrastructure development and construction activities in emerging countries of the Asia Pacific region offer lucrative growth opportunities to manufacturers of polymer modified cementitious coatings. The recent outbreak of the COVID-19 pandemic and its rapid spread across the world has led to economic disruption and has brought down construction activities. Trade, travel, retail, and manufacturing activities have been affected, and the production of construction chemicals has come to a standstill during the first three months of 2020 and is expected to continue till the second quarter of 2020.

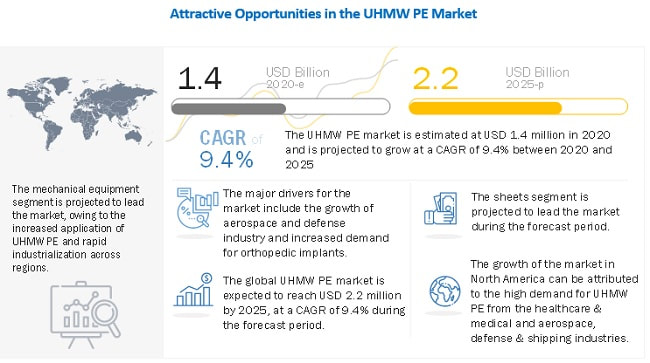

Major companies such as Arkema S.A. (France), Sika AG (Switzerland), Akzo Nobel N.V. (Netherlands), MAPEI S.p.A. (Italy), Compagnie de Saint-Gobain S.A. (France), and Fosroc International Limited (UAE) , Dow, Inc. (US) and H.B. Fuller Company (US) The Lubrizol Corporation (US), Organik Kimya Sanayi Ve Ticaret A.S. (Turkey), Pidilite Industries Limited (India), GCP Applied Technologies Inc. (US), Berger Paints India Limited (India), W. R. Meadows, Inc. (US), Evercrete Corporation (US), Indulor Chemie GmbH (Germany), The Euclid Chemical Company (US) and others are key players in the polymer modified cementitious coatingsmarket. These players have been focusing on developmental strategies, such as expansions, acquisitions, partnerships, joint veture, and new product developments, which have helped them expand their businesses in untapped and potential markets. To know about the assumptions considered for the study download the pdf brochure Arkema S.A. (France) is one of the leading producers of specialty chemicals and advanced materials in the world. The company offers its products to various industries, such as construction, packaging, chemical, automotive, electronics, food, and pharmaceuticals. It offers cementitious coating products through its subsidiary, Bostik. The subsidiary provides construction products based on polymer modified cementitious binders including tile adhesives and grouts, floor screeds, and leveling compounds. The company adopts growth strategies to increase its market share. For instance, in Decemer 2018, The company acquired LIP Bygningsartikler AS (LIP), the Danish leader in tile adhesives, waterproofing systems, and floor preparation solutions through its subsidiary, Bostik. With this acquisition, the company is able to meet customer demand in the Nordic countries. Akzo Nobel N.V. (Netherland) is a leading producer of paints & coatings and specialty chemicals. The company operates through two segments, namely, Performance Coatings and Decorative Paints. It offers cementitious coating products under its Performance Coatings segment which produces automotive and aerospace; industrial; marine and protective; and powder coatings. The company offers products for various end-use industries, such as building & infrastructure, transportation, and consumer goods. . The company has halted its production lines and suspended their financial expectations for 2020 due to significant market disruption resulting from the Covid-19 pandemic. This has impacted the company’s operations across the globe and is expecting improvements from the second quarter in most of the countries. Compagnie de Saint-Gobain S.A. is one of the major players in the construction chemical industry with a strong foothold in Europe and North America. The company currently focuses on strengthening its position of polymer modified cementitious coatings in the Asia Pacific region by adopting growth strategies. For instance, the company partners with SCG Cement-Building Materials in Thailand to develop a modular bathroom solution that incorporates Saint-Gobain Weber tiling and waterproofing solutions. This has helped the company to establish its presence in Thailand and strengthen its position in the Asia Pacific region. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=251464560  The ultra-high molecular weight polyethylene (UHMW PE) market is estimated at USD 1.4 billion in 2020 and is projected to reach USD 2.2 billion by 2025, at a CAGR of 9.4% from 2020 to 2025. Ultra-High Molecular Weight Polyethylene (UHMW PE) is a simple linear background polyethylene possessing unique properties. Due to its ultra-high molecular density, it provides high abrasion resistance and impact strength in comparison to other engineering polymers. Apart from this, the material can also be optimized for more application specific requirements such as noise resistance, low coefficient of friction, excellent chemical resistance, self-lubrication, bio-compatibility, wear resistance, and electric insulation resistance.

The UHMW PE market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific UHMW PE market in 2019. The Asia Pacific region is an emerging and lucrative market for UHMW PE, owing to industrial development and improving economic conditions. In addition, the growth of the medical industry in Asia Pacific is one of the reason leading to an increase in the demand for UHMW PE. UHMW PE is also being used in mechanical equipment. The presence of a number of mechanical component manufacturing plants in China and rapid industrialization in Asia Pacific are expected to drive the UHMW PE market in the coming years. To know about the assumptions considered for the study download the pdf brochure Major companies such as Celanese Corporation (US), Koninklijke DSM N.V. (Netherlands), LyondellBasell Industries N.V. (Netherlands), Braskem S.A (Brazil), Asahi Kasei Corporation, (Japan) Du Pont De Nemours Inc. (US), Saudi Arabia Basic Industries Corporation (Saudi Arabia), Mitsui Chemicals, Inc. (Japan), Honeywell International, Inc. (US), and Teijin Limited (Japan) and others are key players in the UHMW PE market. These players have been focusing on developmental strategies, such as expansions, acquisitions, partnerships, joint veture, and new product developments, which have helped them expand their businesses in untapped and potential markets. Celanese Corporation is engaged in the provision of technology and specialty materials business. It operates through the following segments: Engineered Materials, Acetate Tow, and Acetyl Chain. The Engineered Materials segment includes the engineered materials business, food ingredients business, and certain strategic affiliates. The company adopts growth strategies to increase its market share. For instance, in April 2018, Celanese Corporation announced the addition of a new GUR ultra-high molecular weight polyethylene (UHMW PE) production line at its Nanjing, China manufacturing facility to support the growth in its engineered materials business, specifically the electric vehicle market Koninklijke DSM N.V. has a major business of nutritional and pharmaceutical ingredients and industrial chemicals. The business segments offered by the company include nutrition, materials, innovation center, and corporate activities. The company has a presence in all the major regions, including North America, Europe, Asia Pacific, the Middle East, Africa, and South America. The performance materials segment produces synthetic fibers, engineering plastics, and resins used in coatings, and include engineering plastics, DSM Dyneema, and DSM Resins. DSM acquired majority shares of ICD, a UHMW PE fiber manufacturer in China. The acquisition of the majority share in ICD will bring complementary manufacturing and technology assets to DSM and will strengthen the company’s presence in this UHMW PE market. DSM introduced Dyneema Purity Black fiber, the first black medical-grade UHMW PE fiber. Further the company also fouses on the new product development. For instance, in July 2019, the fiber builds are expected to be 15 times stronger than steel, has a small profile, high pliability, and biocompatibility. Braskem S.A is considered as a major player in the petrochemicals market, owing to its comprehensive product portfolio, and serviceability. It has 29 production plants in Brazil, four in Mexico, five plants in the US, and two plants in Germany. The company adopts several growth strategies to expand its presence in the international market. For instance, the company partnered with Pegasus Polymers for the distribution of UTEC in 2017. With this partnership, the company was not only been able to expand its geographical reach but also penetrate deeper into the Chinese market by increasing the sales network. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=257883188 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed