APAC is the fastest-growing market, in terms of both production and demand. Higher domestic demand, easy availability of raw materials, and low-cost labor make APAC the most preferred destination for the manufacturers of cosmetic pigments. The use of cosmetic pigments as an important additive in various applications such nail products, lip products, eye makeup, facial makeup, hair color products, special effect & special purpose as is driving the market in China. APAC is emerging as a leading consumer of cosmetic pigments due to the increasing demand from domestic as well as international markets.

The cosmetic pigments market is projected to grow from USD 698 million in 2019 and expected to reach USD 1,019 million by 2024, at a CAGR of 7.9%. The global market for cosmetic pigments is driven primarily by the increasing demand for cosmetic products. Cosmetic pigments are used for manufacturing cosmetic and personal care products for color enhancement. With the growing demand for various cosmetic & personal care products, the use of cosmetic pigments is also increasing. Cosmetic pigments are used in the production of cosmetic colors, along with various other ingredients. A pigment is a colored or colorless insoluble chemical compound, that gives an added richness of color to the product. Most cosmetic and personal care products use fine dry powdered cosmetic pigments. Pigments used for manufacturing color cosmetic products are termed as cosmetic pigments. Pigments are classified into organic and inorganic based on their chemical composition. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=179525453 Cosmetics products were traditionally made of chemical compounds; however, recently, there has been a significant demand for cosmetic products derived from natural sources. The application of cosmetic pigments includes nail products, lip products, eye makeup, facial makeup, hair color products, special effect & special purpose, and others (toothpaste, hair shampoo & conditioner, and sunless tabbing products). Facial makeup accounts for the largest application of cosmetic pigments market. The increasing demand for root makeup products such as foundations and face powders is expected to drive the market in this application segment. Increasing demand for root makeup products such as foundations and face powders is expected to drive the market in this application. Cosmetic pigments are used in facial makeup applications such as foundations, blushers, and powders, where titanium dioxide is used to add brightness. The key players in the cosmetic pigments market include Sun Chemical (US), Sensient Cosmetic Technologies (France), Merck (Germany), BASF (Germany), ECKART (UK), Sudarshan (India), Kobo Products (US), Clariant (Switzerland), and Geotech (Netherlands). These players have established a strong foothold in the market by adopting strategies such as expansion, new product launch, and merger & acquisition. These companies adopted various organic as well as inorganic growth strategies between 2014 and 2019 to strengthen their position in the market. Expansion was among the key growth strategies adopted by these leading players to enhance their regional presence and meet the growing demand for cosmetic pigments from emerging economies. Don’t miss out on business opportunities in Cosmetic Pigments Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 Comments

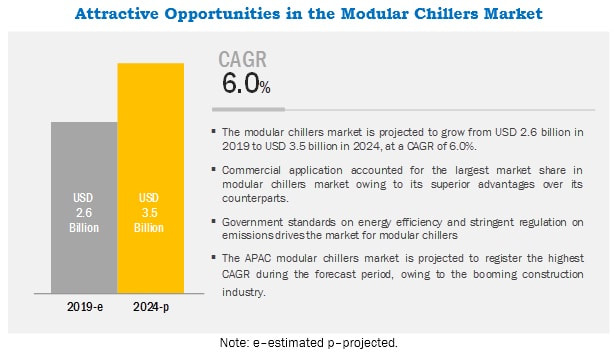

The modular chillers market is projected to grow from USD 2.6 billion in 2019 to USD 3.5 billion by 2024, at a CAGR of 6.0% during the forecast period. The growth of the modular chillers can be attributed to the stringent government regulations on energy efficiency and emissions, globally. In addition, the competitive advantages of modular chillers over its substitutes has increased its demand in the HVAC and refrigeration systems.

The demand for modular chillers has been gaining momentum in the HVAC industry as it is lighter, efficient, and lowers the required refrigerant volume as compared to other heat exchangers. Modular chillers are widely used in AC systems and heat pumps for efficient heat transfer between refrigerant and air. In the recent years, owing to the growing demand for lightweight systems and rising copper prices, the demand for modular chillers has increased in various HVAC applications. Moreover, because of compact design, lightweight, and lower hold-up volume, modular chillers are used in the residential and commercial cooling applications. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=75609903 Competitive advantages as compared to other alternatives, drives the demand for modular chillers in the commercial application. Modular chillers have a compact design, which is ideal for buildings where space is limited. It has control systems, which can be operated from remote places. Also, the biggest advantage of modular chillers is ‘modularity’, which means, operators can shut down any unit when cooling requirements are low and switch on any number of units when the requirement is high. Therefore, the modular chiller operators, can reduce the downtime to zero hours, as it is highly unlikely that all modules malfunction. In addition, modular chillers offers superior expandability, when operators plan infrastructure expansion. The modular chiller system capacity can be increased by adding parallel modules with the currently installed chiller system. These overall advantages of modular chillers have increased their demand. Recent Developments In May 2019, Frigel Firenze launched new modular chillers; 3FX chillers. These chillers are available in 12 models. Seven models come with screw compressors and the remaining five come with scroll compressors. These chillers cater to industrial applications. In March 2018, Mitsubishi Electric Hydronics & IT Cooling Systems acquired chillers distributor Topclima of Climaveneta in Spain. This acquisition of Topclima helps the company to use the assets efficiently for business development. APAC has the most populous countries, namely, China and India. China, Japan, South Korea, and India are the key markets for modular chillers in APAC. In 2018, China accounted for the largest share of the APAC market, owing to the presence of huge HVAC and construction industries. According to the World Bank, India is expected to be one of the world’s fastest-growing economies with an estimated annual GDP expansion rate of more than 7.0% during the forecast period. In addition, the overall demand for ACs across APAC countries witnessed high growth in 2018. Thus, the overall economic scenario in APAC is favorable for the growth of the modular chillers market. Carrier Corporation (US), McQuay Air-Conditioning (Hong Kong), Johnson Controls- Hitachi Air Conditioning (Japan), Midea Group (China), Ingersoll Rand (Ireland), Gree Electric Appliances (China), Frigel Firenze (Italy), Mitsubishi Electric Corporation (Japan), Multistack (US), and Haier Group (China) are a few active players in the modular chillers market. Don’t miss out on business opportunities in Modular Chillers Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The propylene glycol market is projected to reach USD 4.7 billion by 2024, at a CAGR of 4.4% from USD 3.8 billion in 2019. The eco-friendly production process of bio-based propylene glycol has led to the growth of the global propylene glycol market. The growing automotive industry in APAC is also driving the market as propylene glycols are widely used in engine coolants and sheet molding compounds, among others.

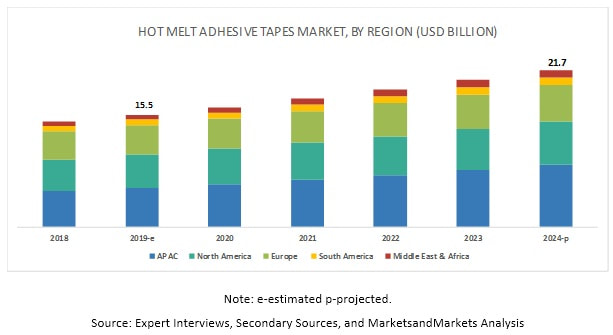

Browse 128 market data Tables and 54 Figures spread through 176 Pages and in-depth TOC on “Propylene Glycol Market by Source (Petroleum-based, Bio-based), Grade (Industrial, Pharmaceutical), End-use Industry (Transportation, Building & Construction, Food & Beverage, Pharmaceuticals, Cosmetics & Personal Care), Region – Global Forecast to 2024” Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=264488864 “Bio-based propylene glycol to register the highest CAGR in the global propylene glycol market” The global propylene glycol market is segmented by source, into petroleum-based and bio-based propylene glycol. The market for bio-based propylene glycol is expected to grow at the highest CAGR from 2019 to 2024. This is because the production of propylene glycol from the bio-based source has less impact on the environment. In addition, increasing demand from the pharmaceuticals, food & beverage, and cosmetics applications is also driving the growth of the bio-based propylene glycol market. “Transportation to be the fastest-growing end-use industry of the global propylene glycol market” Transportation is projected to be the fastest-growing end-use industry in the global propylene glycol market during the forecast, period mainly due to the rising demand for propylene glycols in automotive coolants, aircraft wings, pleasure boats, and ships application. The transportation industry is estimated to witness the highest CAGR in the APAC region. Improving standards of living and increasing disposable income in emerging countries such as India, China, and South Korea are also driving the growth of the transportation industry. China, Korea, Japan, and India are witnessing high demand for new ships for both military and commercial purposes. The propylene glycol market in APAC is expected to witness the highest CAGR between 2019 and 2024. Stable economic growth in the region, coupled with rising disposable income, is driving the market. In addition, increased demand for propylene glycol, in key countries such as China and India, is contributing to the growth of the propylene glycol market in the region. The key market players profiled in the report include as The Dow Chemical Company (US), LyondellBasell Industries N.V. (Netherlands), BASF SE (Germany), Archer Daniels Midland Company (US), Global Bio-chem Technology Group Co., Ltd. (China), DuPont Tate & Lyle Bio Products Company, LLC (US), Huntsman Corporation (US), SKC Co., Ltd. (South Korea), Temix Oleo S.R.L. (Italy), and Ineos Oxide (Switzerland). Don’t miss out on business opportunities in Propylene Glycol Market. Speak to our analyst and gain crucial industry insights that will help your business grow. About MarketsandMarkets™ MarketsandMarkets™ provides quantified B2B research on 30,000 high growth niche opportunities/threats which will impact 70% to 80% of worldwide companies’ revenues. Currently servicing 7500 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions. Our 850 fulltime analyst and SMEs at MarketsandMarkets™ are tracking global high growth markets following the “Growth Engagement Model – GEM”. The GEM aims at proactive collaboration with the clients to identify new opportunities, identify most important customers, write “Attack, avoid and defend” strategies, identify sources of incremental revenues for both the company and its competitors. MarketsandMarkets™ now coming up with 1,500 MicroQuadrants (Positioning top players across leaders, emerging companies, innovators, strategic players) annually in high growth emerging segments. MarketsandMarkets™ is determined to benefit more than 10,000 companies this year for their revenue planning and help them take their innovations/disruptions early to the market by providing them research ahead of the curve. MarketsandMarkets’s flagship competitive intelligence and market research platform, “Knowledgestore” connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets. Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : 1-888-600-6441 [email protected] Rising demand from emerging economies is expected to drive the hot melt adhesive tapes market7/19/2020  The market size of hot melt adhesive tapes is projected to grow from USD 15.5 billion in 2019 to USD 21.7 billion by 2024, at a CAGR of 7.0%, during the forecast period. The global hot melt adhesive tapes market is witnessing high growth on account of increasing applications, technological advancements, and growing demand in the APAC region. Growing packaging market in emerging economies is a key factor providing growth opportunities to the market.

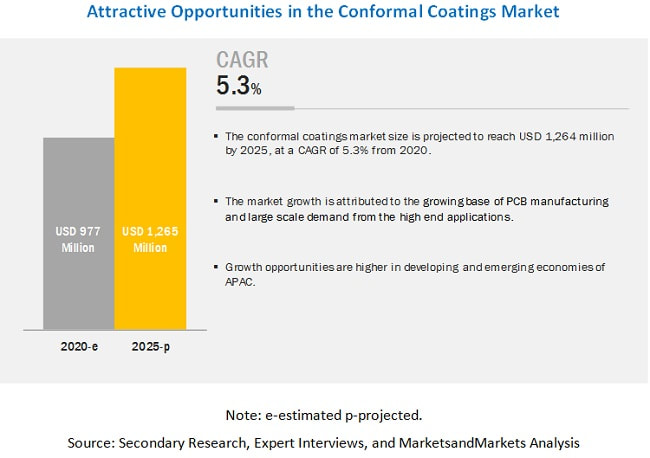

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=138739970 APAC is expected to be the largest and fastest-growing hot melt adhesive tapes market. The demand for hot melt adhesive tapes has increased in other APAC countries, such as South Korea, Singapore, India, and Indonesia, as the application activities in these countries have risen. China has been the driving force for the rapid expansion of the adhesive tapes market, not only in APAC, but also worldwide. In several countries, the factors affecting the packaging, which is a major application of hot melt adhesive tapes, are the increasing level of disposable income and population growth. This growth is driven by rapidly rising household income and the fast-growing middle-class population, which has boosted the demand in packaging and DIY, among other applications, in the hot melt adhesive tapes market. These factors are positively influencing the hot melt adhesive tapes market growth. Increasing public awareness for DIY is fueling the use of these tapes in different activities, such as gardening, crafting, and small construction & furniture projects. A majority of these tapes are used for different office and household applications. The consumer & DIY applications of hot melt adhesive tapes include temporary repairing of rips on any kind of surface, sealing of leaks and holes, temporary mounting of damaged components of cars and automobiles, jointing of broken components of various tools, sealing, and packaging. Hence, the demand for consumer & DIY applications is high in the hot melt adhesive tapes market. Key players profiled in the hot melt adhesive tapes market report include The 3M Company (US), Nitto Denko Corporation (Japan), tesa SE (Germany), Avery Dennison Corporation (US), Intertape Polymer Group Inc. (Canada), Shurtape Technologies, LLC (US), Scapa Group plc (UK), LINTEC Corporation (Japan), ACHEM Technology Corporation (Taiwan), and TE Connectivity Ltd (Switzerland). Read More: https://www.marketsandmarkets.com/ResearchInsight/hot-melt-adhesive-tapes-market.asp  The Conformal coatings market is estimated to be USD 977 million in 2020 and is expected to reach USD 1,265 million by 2025 at CAGR of 5.3%. Conformal coatings are a type of protective coatings of 25-75µm thickness, which are applied to printed circuit boards (PCBs) and other electronic components to protect them from harsh environments such as dust, solvents, moisture, humidity, and high temperature. Conformal coatings increase the operational performance of PCBs assemblies by maintaining long-term surface insulation.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=216347388 The automotive industry has grown at a fast pace in the last decade, which led to the rapid evolution and increased consumption of electronics used in the vehicles. Currently, an average mid-range vehicle is loaded with technological features such as lane sensors, adaptive cruise control, in-car entertainment, and navigation. Also, the emergence of electric vehicle (EV), connected cars, and autonomous vehicles have resulted in a rapid surge in the advancement of electronics installed in these vehicles. From the industry point of view, the challenge is to protect these huge volumes PCBs and ICs used in the electronics system over a long period while meeting the specifications required by the automotive industry. This creates an attractive opportunity for conformal coatings manufacturers in the automotive and transportation industry. It is also the go-to-market for PCB manufacturers. APAC is the largest market of conformal coatings, and this dominance is expected to continue till 2025. China is the key market in the region, consuming more than half of the demand for conformal coatings, followed by Taiwan, South Korea, and Japan. These countries are expected to witness a steady increase in consumption from 2020 to 2025. The region contributes close to 90% of PCB production in the world, and market is mainly driven by the presence of a large number of leading global electronics companies. PCB industry is quite fragmented as there are more than 100 companies that constitute close to 90% of overall PCB revenues and most of them belong to APAC, more so in China & Taiwan. Recent years have seen a lot of PCB manufacturing shifts to APAC due to cost-effectiveness and closer access to customers in the region, hence the increase in consumption of conformal coatings. North America is projected to be the second-largest market in the overall market. The conformal coating market in the region will be driven by the PCB demand from the electric vehicle (EV) manufacturers. But in recent years, PCB manufacturers are looking to capture the aerospace and defense industry which will create opportunities for conformal coatings as this PCB should be protected for them to work in full capacity during operations. The leading players in the global conformal coatings market include Henkel (Germany), Chase Corporation (US), Illinois Tool Work (US), Electrolube (UK), Shin-Etsu Chemicals (Japan), Dow (US), HB Fuller (US). These players account for significant market shares. The companies adopted expansion and new product developments as key strategies to enhance growth in the market. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=216347388  The global phenolic panel market size is expected to grow from USD 1.7 billion in 2020 to USD 2.4 billion by 2025, at a CAGR of 6.5% during the forecast period. The market is growing due to the increase in the demand for phenolic panels in the construction, transportation, and aerospace & defense industries.

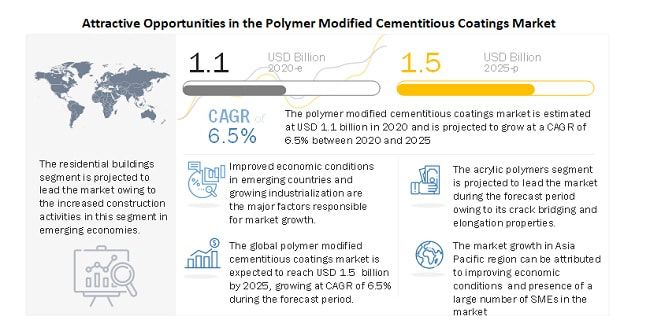

Interior is the largest application of phenolic panel Phenolic panels are used extensively for aircraft interior, railway interior, decorative interior in construction, partitions, and cubicles in various end-use industries. Superior fire-resistance and chemical resistance offered by the phenolic panel is responsible for the high consumption in an interior application. Download PDF Brochure to Know More: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=22703551 The construction end-use industry accounted for the largest share in the market Phenolic panels are used in various end-use industries, such as mining & quarrying, cement & aggregate, steel, and others. The construction industry dominated the global phenolic panel market. The phenolic panel has a large demand for interior applications in the construction industry owing to superior fire resistance characteristics of the phenolic panel, which helps in avoiding fire-related accidents. The phenolic panel market is segmented based on region into Europe, North America, APAC, MEA, and South America. Europe is the major consumer of phenolic panels owing to the high demand from the UK, Germany, and other European countries. The UK is the leading market in the region. Major applications of phenolic panels in the European market include building interior, aircraft interior, exterior cladding, furniture, and air conditioning duct panels, among others. The growth of the market is also attributed to the presence of established manufacturers and technological advancement related to the development of phenolic panel products. The key players in the market include Kingspan Group (Ireland), Wilsonart LLC(US), Asahi Kasei Corporation (Japan), Fiberesin Industries Inc. (US), Broadview Holding B.V. (Netherlands), Fundermax GmbH (Austria), Bobrick Washroom Equipment, Inc. (US), Werzalit of America, Inc. (US), ASI Group (US), and General Partitions Mfg. Corp. (US).These companies are adopting various inorganic and organic strategies to increase their foothold in the phenolic panel market. Recent Developments In April 2017, Kingspan Group added two new products to its Kooltherm K100 range; the K112 Framing Board and K107 Pitched Roof Board. These insulation boards deliver low U-values with minimal thickness. In June 2019, Broadview Holding acquired Cincinnati-based Formica Group from Fletcher Building Ltd. This acquisition has helped Broadview Holding to increase its presence in Europe, North America, and Asia. Get in-depth analysis of the COVID-19 impact on the Phenolic Panel Market Benchmarking the rapid strategy shifts of the Top 100 companies in the Phenolic Panel Market Request Now: https://www.marketsandmarkets.com/RequestCOVID19.asp?id=22703551  The polymer modified cementitious coatings market in 2020 is estimated at USD 1.1 billion and is projected to reach USD 1.5 billion by 2025, at a CAGR of 6.5% from 2020 to 2025. The growth of this market can be attributed to the increasing demand for polymer modified cementitious coatings from the residential buildings sector. In addition, government initiatives to support infrastructural developments in the Asia Pacific region are anticipated to drive the growth of the polymer modified cementitious coatings market. Furthermore, outbreak of COVID-19 pandemic is anticipated to hamper the consumption of polymer modified cementitious coatings which affects the market growth.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=251464560 The acrylic polymers segment is estimated to lead the polymer modified cementitious coatings market in 2020, due to the rising demand due to increasing use of acrylic-based polymer modified cementitious coatings in residential buildings applications. Further, acrylic-based polymer modified cementitious coatings are low in alkali content, fast-setting, and high strength properties. These are also used for patching small cracks, holes, honeycombs, and surface defects over half-inch in depth. They are used in waterproofing floors, columns, beams, slabs, loading docks, and precast walls. They are also used for the protection of concrete structures from vapor, chloride ions, acidic gas, and alkali attacks. The growth of the residential buildings segment can be attributed to the increasing use of polymer modified cementitious coatings in various residential applications, such as exterior walls, driveways & sidewalks, and floorings. Furthermore, the growth of the real estate market in emerging countries of Asia Pacific and the Middle East & Africa has contributed to the growth of the polymer modified cementitious coatings market in the residential buildings segment. The polymer modified cementitious coatings market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific polymer modified cementitious coatings market in 2019. The Asia Pacific region is an emerging and lucrative market for polymer modified cementitious coatings, owing to industrial development and improving economic conditions. This region constitutes approximately 60% of the world’s population, and thus leads to the wide-scale use of polymer modified cementitious coatings for waterproofing applications in residential and non-residential buildings, and public infrastructure. Outbreak of COVID-19 from China and the impact of coronavirus in Japan, South Korea, Autralia, and India has caused a decrease in the consumption of polymer modified The polymer modified cementitious coatings market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific polymer modified cementitious coatings market in 2019. The Asia Pacific region is an emerging and lucrative market for polymer modified cementitious coatings, owing to industrial development and improving economic conditions. This region constitutes approximately 60% of the world’s population, and thus leads to the wide-scale use of polymer modified cementitious coatings for waterproofing applications in residential and non-residential buildings, and public infrastructure. Outbreak of COVID-19 from China and the impact of coronavirus in Japan, South Korea, Autralia, and India has caused a decrease in the consumption of polymer modified cementitious coatings. Read More: https://www.marketsandmarkets.com/ResearchInsight/polymer-modified-cementitious-coating-market.asp  The mining industry utilizes chemicals in all stages of production. These chemicals are used to increase the efficiency and productivity of mining processes such as extraction and recovery of minerals from ores. A wide variety of general and specialty chemicals are utilized for mining. The mining chemicals market has generally been characterized by fluctuations in commodity prices, low profit margins, and increased competition from producers in less developed countries, especially China which has aggressively been manufacturing and exporting mining chemicals. Continuous changes in the landscape of ores have shifted the focus of mining chemical providers towards innovations in the technology that can ensure economical treatment of ores. Advancements in terms of product innovations and technologies are expected to create substantial investment opportunities for mining chemicals.

The mining chemicals market size is estimated to grow from USD 6.02 Billion in 2017 to USD 7.54 Billion by 2022, at a CAGR of 4.60%. The mining chemicals market is witnessing considerable growth due to the rise in industrialization and infrastructural development. High demand for mining chemicals is primarily attributed to increasing complexity of ores and decreasing ore grades. The mining chemicals industry has come across new opportunities due to the growing stringent government regulations on wastewater pollution, coupled with the rising demand for quality minerals. Download PDF Brochure to Know More: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=205253671 Asia-Pacific market accounted for the largest share of the global mining chemicals market, followed by Europe and North America. Countries such as China and Japan are expected to witness high growth in the mining chemicals market due to rapid economic expansion. The region has vast mineral resources of copper, zinc, aluminum, coal, limestone, and rare earth & precious metals. The positive outlook of the economies is attracting huge investments from global mining companies. As a result, the mining capacity of various metals and minerals is increasing, thereby boosting the demand for mining chemicals. The demand is primarily met by domestic players of the nations in this region. High demand for mining chemicals in the country can be credited to the continuous exploration and beatification of ores. Additionally, high foreign investments in China’s mining industry are expected to support the application for mining chemicals in the country. The major players in the Mining chemicals market include AkzoNobel N.V. (Netherlands), BASF SE (Germany), Clariant AG (Switzerland), Cytec Industries Inc. (U.S.), Kemira OYJ (Finland), The Dow Chemical Company (U.S.), Huntsman International LLC (U.S.), Orica Limited. (Australia), ArrMaz Products, L.P. (U.S.), and SNF Floreger (France). Read more: https://www.marketsandmarkets.com/PressReleases/specialty-mining-chemical.asp  The hexamethylenediamine market is estimated to be USD 5.35 Billion in 2017 and is projected to reach USD 6.82 Billion by 2022, at a CAGR of 5.0% from 2017 to 2022. The demand for hexamethylenediamine is mainly driven by the growing consumption of nylon 66 in different end-use industries, such as automotive and textile. The automotive industry is shifting from traditional materials toward engineering plastics to attain better productivity and efficiency of components. The growing use of nylon 66 products and components in the automotive industry is anticipated to drive the market for hexamethylenediamine in the coming years.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=109635705 Hexamethylenediamine is majorly used in the synthesis of nylon 66, which is widely used in the automotive industry to manufacture various products and components, such as connectors & housings, under-the-hood components, wheel well, and lighting components, such as headlamp structural housings, headlamps & fog lamps, and reflectors & lighting sockets, among others. Nylon is extensively used in automotive products and components as it offers excellent chemical and physical properties, along with design flexibility, as compared to metal. The growing automotive industry is anticipated to drive the nylon market, which will further drive the hexamethylenediamine demand in the coming years. Nylon has superior mechanical property, rigidity, and chemical & heat resistivity and is widely used as fiber in textiles, carpets, and molded parts. Nylon is used to manufacture various products & components in the automotive and electrical & electronics end-use industries. The growing usage of nylon across various industries, such as automotive, textile, consumer goods, and electrical & electronics is anticipated to boost the hexamethylenediamine market across regions. The Asia-Pacific hexamethylenediamine market is projected to grow at the highest CAGR during the forecast period. China, India, Japan, Taiwan, and South Korea are the key countries contributing to the high demand of hexamethylenediamine in the Asia-Pacific region. Increasing demand for hexamethylenediamine from the nylon 66 application market is the major growth driver for the hexamethylenediamine market in this region. Some of the key players in the hexamethylenediamine market are BASF SE (Germany), E. I. du Pont de Nemours (DuPont) (US), Asahi Kasei Corporation (Japan), Toray Industries, Inc. (Japan), Merck KGaA (Germany), Evonik Industries AG (Germany), Solvay S.A. (Belgium), Ashland Global Holdings, Inc. (US), Invista (US), Ascend Performance Materials (US), Rennovia, Inc. (US), and Compass Chemical (US). Read More: https://www.marketsandmarkets.com/PressReleases/hexamethylenediamine.asp |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed