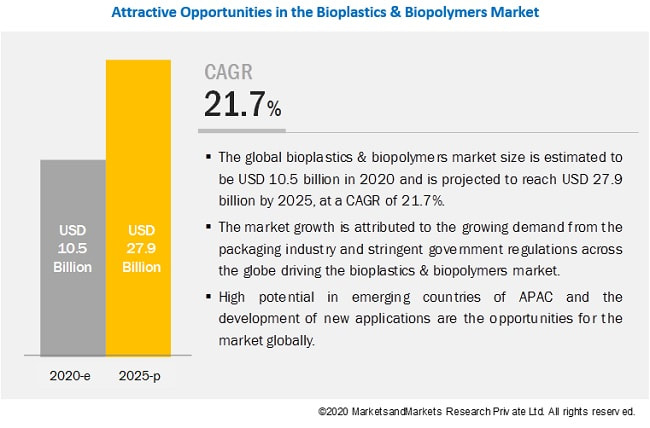

Green procurement policies and regulations to increase the demand for bioplastics & biopolymers9/30/2020  The global bioplastics & biopolymers market size is expected to grow from to grow from USD 10.5 billion in 2020 and USD 27.9 billion by 2025, at a CAGR of 21.7% during the forecast period. The major factors driving the bioplastics & biopolymers industry include the focus of governments on green procurement policies and regulations and increasing use of bioplastics in the packaging end-use industry.

Download PDF to Know More: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=88795240 The growing need to reduce the dependency on conventional fossil fuels is propelling the demand for bio-based products. This is also supported by the new policies and regulations implemented and adopted by the government bodies globally. These regulations include banning or implementing additional surcharges on the use of conventional plastics in applications, such as shopping bags, packaging materials, and disposables. These increasing regulations and prohibitions against plastic bags and other plastic items are driving the market for bioplastics, especially biodegradable plastics worldwide. Packaging is one of the end-use industries that dominate the bioplastics & biopolymers market. Bioplastics, and especially biodegradable bioplastics, have increasing demand to replace conventional plastics to address environmental concerns. The use of bioplastics is increasing in applications such as bottles, films, clamshell cartons, waste collection bags, carrier bags, mulch films, and food service-ware. Based on region, the bioplastics & biopolymers market has been segmented into APAC, Europe, North America, RoW. APAC is the fastest-growing bioplastics & biopolymer market owing to the increasing consumer preferences towards eco-friendly plastic products with the rapidly growing population of the region. Increasing consumer purchasing power has propelled the growth of various end-use industries in this region. These factors are expected to lead to increasing demand for bioplastics & biopolymers in the region during the forecast period. Request For Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=88795240

0 Comments

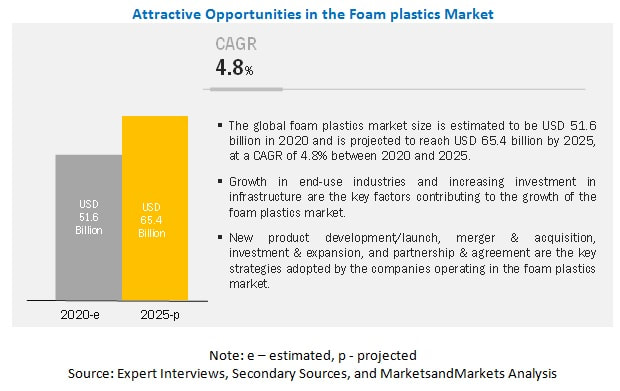

Foam plastics are resins used in manufacturing polymer foams, which are used in various end-use industries such as building & construction, furniture & bedding, packaging, and automotive among others. The market size for Foam plastics is projected to grow from USD 51.6 billion in 2020 to USD 65.4 billion by 2025, at a CAGR of 4.8%. Foam plastics are largely used in building & construction, packaging, and furniture & bedding. The polyurethane segment is estimated to account for the largest share of the overall market due to its properties such as low heat conduction coefficient, low density, low water absorption, relatively good mechanical strength, and good insulating properties.

Browse and in-depth TOC on “Foam Plastics Market” 119 – Tables 38 – Figures 174 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=260352983 Polyurethane resin segment is projected to be the largest segment of the foam plastics market. PU resin-based foam is available in a wide range of rigidity, hardness, and density levels. Low-density flexible resin-based foams are used in upholstery, bedding, automotive and truck seating, and novel inorganic plant substrates for roof or wall gardens. PU foams are mainly used in furniture & bedding and building & construction sectors. It is produced by many leading manufacturers. PU resin-based foam is a good choice for insulation and helps in reducing CO2 emissions. It is a versatile substance in terms of its properties and is, therefore, suitable for use in the construction and automotive industries. As the construction industry is growing rapidly in APAC, PU resin plays a dominant role in the growth of the overall foam plastics market in the region. Footwear, sports & recreational is the fastest-growing segment of the overall foam plastics market. The footwear, sports & recreational segment is projected to be the fastest-growing end-use industry of foam plastics. The properties offered by foam plastics in polymer foams, such as good thermoforming capacity and creep resistance, make it suitable for use in many sporting goods such as skis, hockey sticks, snowboards, surfboards, and racing bicycle wheels. Using foam plastics in sporting goods make the final products lightweight and durable with high mechanical properties APAC is the leading market for foam plastics. The growth in the region is fueled by the booming economies of China, India, Indonesia, and Vietnam. PU resin based foams are preferred choice in the building & construction industry in APAC. It is in high demand, as it is a low-cost material that provides low heat conduction coefficient, low density, low water absorption, relatively good mechanical strength, and good insulating properties. APAC is a rapidly developing region with growth opportunities for companies willing to invest in high-growth markets. The key players profiled in the foam plastics market report are BASF SE (Germany), Covestro (Germany), Huntsman International LLC (US), The Dow Chemical Company (US), and Wanhua Chemical Group Co., Ltd. (China). Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=260352983  Microporous insulation is high-temperature insulation, which provides extremely low thermal conductivity over a temperature ranging from 0.021 w/m.k (watt/meter/Kelvin temperature) to 0.034 w/m.k at a mean temperature of 800°C.

As compared to conventional insulation materials, such as glass-filled foams, fibers, and metals, microporous insulating materials have a thermal efficiency that is four to five times greater. The superior thermal resistance of microporous insulation shows enormous potential in oil & gas applications, where insulation is of prime importance. Besides excellent thermal performance, microporous insulating materials have significant resistance to flame and extreme weather conditions. Also, as per the International Energy Agency, the global oil & gas sector is expected to witness considerable growth until 2020 due to increasing demand from the automotive and aviation industries. The growing oil & gas sector requires advanced insulation materials for transporting oil & gas to distant areas. Download PDF Brochure to Know More: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=129425481 The global microporous insulation market size was USD 125.8 million in 2017 and is projected to reach USD 165.4 million by 2023, at a CAGR of 4.7%. Additionally, the microporous insulation market is expected to grow from 3,800 metric tons in 2018 to 4,608 metric tons by 2023, at a CAGR of 3.9%. Its unique property of space and weight conservation in the aerospace & defense application will drive the growth of this market during the forecast period. The aerospace & defense application segment is projected to register the highest CAGR, in terms of value, between 2018 and 2023. The demand for microporous insulation is increasing in the aerospace application due to increasing demand for light-weight materials, which in turn, saves the fuel consumed during operation of an aircraft. In addition, the use of microporous insulation provides high performance and helps to meet the space and weight specifications in the aerospace sector. It is the most demanding sector in terms of performance & reliability due to operational and safety reasons. The microporous insulation market has been studied for North America, Europe, Asia Pacific, South America, and the Middle East & Africa. The Asia Pacific region is projected to register the highest CAGR, in terms of value, during the forecast period. The growth of the microporous insulation market in the region is attributed to the rising awareness about the benefits of microporous insulation materials and growing industrialization and infrastructure development in the region. In addition, increase in the demand for energy, power, metal, and automobiles is also expected to drive the market. Don’t miss out on business opportunities in Microporous Insulation Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The splicing tapes market size is projected to grow from USD 527 million in 2018 to USD 593 million by 2023, at a CAGR of 2.37% during the forecast period. The global paper & printing industry is undergoing a rapid transformation and plays a significant role in driving the splicing tapes market globally. Splicing tapes are used in the production of paper, films, label, and packaging products (such as corrugated boxes, paperboards, or envelopes). However, the environmental regulations related to the paper & pulp sector could act as a major constraint. The developed countries, in regions such as Europe and North America, are anticipated to cut back on the growth level in the near future, owing to the stagnant nature of their markets.

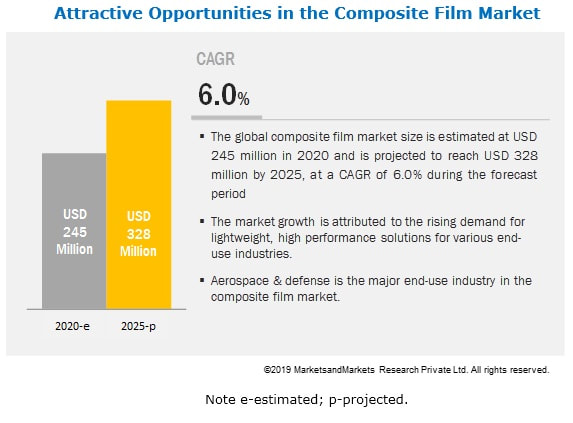

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=11550590 The paper/tissue is the most popular backing material used in the manufacturing of splicing tapes. Easy availability, flexibility, and a high degree of printability are driving the demand for paper/tissue backing splicing tapes. Also, paper/ tissue backing tape comes with many attractive features such as UV resistance, repulpablity, and others. Repulpable paper/tissue tape line can be recycled without contamination of the broke pulp for use in paper mills, converters, newspapers, and web printers for roll closing/tabbing and splicing. The splicing tapes used in the paper & printing industry can be single-sided or double-sided and repulpable and non-repulpable. Splicing tapes are mainly used in the paper industry during production of paper. They are also used for flexographic printing, end tabbing, permanent overlapped splices, paper for packaging application, and others. Splicing tape is particularly characterized by a high tensile strength, high shear strength, and good ageing resistance. APAC is expected to account for the largest market APAC is the largest splicing tapes market, in terms of value and volume, and is projected to be the fastest-growing splicing tapes market during the forecast period. APAC has been a high potential splicing tapes market against the backdrop of an overall slowdown in the global economy. The paper & printing and packaging sectors are growing rapidly in tandem with the rising population which is one of the major factors driving the splicing tapes market. The market in China, India, and other rapidly developing countries is expected to witness the fastest growth, while more developed markets such as the US, Germany, Japan, and the UK, will witness slow or no growth during the forecast period. In APAC, China is the largest and second-fastest growing economy after India. China is currently one of the largest pulp and paper product manufacturers in the world. The Chinese manufacturers have consistently invested in the latest paper manufacturing infrastructure, creating a highly competitive environment for international trade of paper products. Various advanced technologies and machinery are used in the country by manufacturers to come up with the end products of splicing tapes by using different backing materials. Request For Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=11550590 Composite film market is increasing due to the rise in the demand for high-performance materials9/17/2020  The global composite film market size is expected to grow from USD 245 million in 2020 to USD 328 million by 2025, at a CAGR of 6.0%. Due to the increase in the demand for high-performance materials with properties such as high strength to weight ratio, good tensile strength, electrical conductivity among others, the global composite film market is expected to witness significant growth during the forecast period.

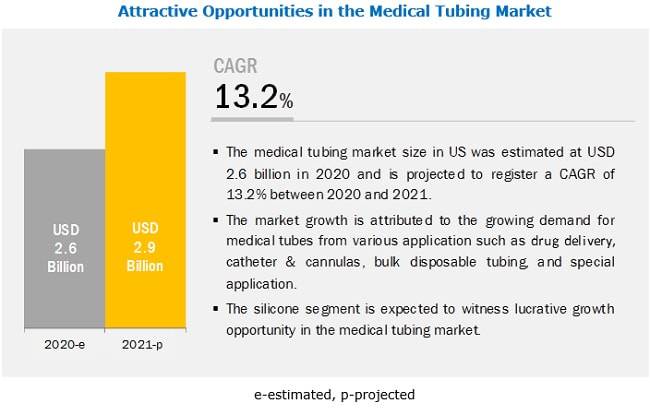

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=232995579 The aerospace & defense industry is a major consumer of composites, which in turn increases the demand for composite films. Leading aircraft manufacturers such as Boeing and Airbus are increasing the use of carbon composites, and composite films in their commercial aircraft. Composite films are also used in fuselage, wings, tail, tail fin, wing box, trailing edge, engine nacelles, engine, and other structural parts of an aircraft. Growing environmental concerns and search for high strength lightweight materials to increase fuel efficiency has put composites and simultaneously composite films under the limelight in the automotive industry. As, the composite structures used on automotive would require Class A protection from extreme climates, and scratches. Epoxy resin film comprises a major share of the composite film market. Epoxy resins are thermoset resins known for their excellent mechanical, electrical, and high-heat resistance properties. They are available in a wide range of curing-agent variations. They have better physical, mechanical, adhesion, and low shrinkage properties in comparison to other resin films. High strength and resistance to moisture are obtained when these epoxy resin films are applied to composite panels. Autoclave curing type produces denser, and void-free molding because high heat and pressure are used for its curing. Autoclaves are in high demand as it helps in producing high-value composite films, and are widely used in the aerospace industry to fabricate high strength-to-weight ratio parts for aircraft. This curing type method generally uses high-temperature matrix resins, such as epoxy, which has higher properties than conventional resins. Thus, autoclave curing is widely used in aerospace & defense, automotive, and other end-use industries. North America holds the largest market for the composite film market. The key reason for this includes the demand for composite films in the aerospace & defense industry in the region. The demand for composite film in aerospace & defense, automotive, and other industries is projected to improve due to product innovation and technological advances made in this sector. According to the 24/7 Wall St. a Delaware corporation, in the US, parts of Florida experience an average of 100 thunderstorm days annually, making Florida the most likely place in the country for lightning strikes. Also, along the US West Coast, annually, an average of 10 thunderstorms is experienced. These factors drive the demand for composite films during the forecast period. Don’t miss out on business opportunities in Composite Film Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  COVID-19 Impact on Medical Tubing Market The US medical tubing market size is projected to reach USD 2.9 billion by 2021, at a CAGR of 13.2%. The major factors driving the medical tubing industry include increasing demand from various applications such as drug delivery and growing usage in ventilators. The rising demand for medical devices that incorporate medical tubing and the growing demand for ventilators in this pandemic are propelling the growth of the medical tubing market globally. However, factors such as restricting counterfeit products and fighting time for supply chain and logistics could affect the market growth.

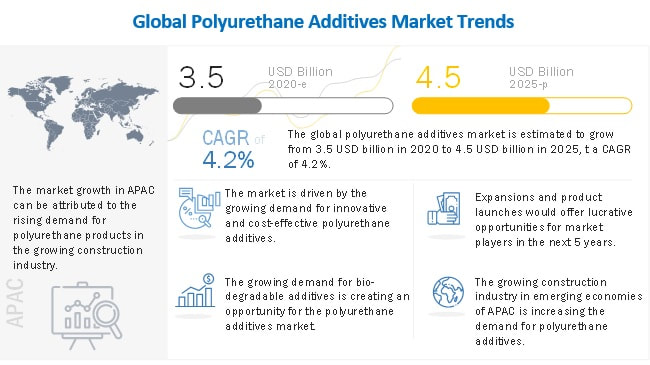

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=165863042 The market has been segmented based on application as drug delivery, catheter & cannulas, bulk disposable tubing, and special application. The drug delivery segment dominates the market in 2020 and is expected to witness significant growth during the forecast period. The growth in this segment is attributed to the growing usage of medical tubes as a device or channel of delivery in drug delivery systems. The demand for drug delivery system is increasing due to the rising incidence of COVID-19 cases, globally. The market is also influenced by growing COVID-19 infection in people having existing medical conditions such as asthma and diabetics. There is considerable growth in the demand for drug delivery devices and equipment such as nasogastric tubes, nebulizers, spacer devices, and others. These factors are expected to drive the demand. The US is projected to be the leading medical tubing market during the forecast period. The growth in the US can be attributed to the rising demand for medical tubing applications such as drug delivery, catheter & cannulas, bulk disposable tubing, and special application. The presence of a robust industrial base, favorable government policies, and large number of established players for medical tubing in the country are strengthening the medical tubing industry in the country. Zeus Industrial Products (US), Saint Gobain Performance Plastics (France), Teleflex (US), Optinova (US), and Lubrizol Corporation (Vesta) (US), among others, are the key players operating in the medical tubing market. In February 2020, Teleflex Medical OEM acquired HPC Medical Products to strengthen its medical tubing & wire components and catheters portfolio. With this acquisition, the company is able to meet the growing demand in this pandemic situation. Now, the company is able to supply more products to the impacted countries with immediate effect to meet the growing demand. Lubrizol announced the continuous supply of flexible and biocompatible materials for vascular catheters, IV tube sets, and medical components used in ventilators, valves, and infusion pumps. In order to attain this, it has altered its production process to deliver more products which can serve the purpose during this COVID-19 pandemic. The company also ramped up the supply of ESTANE thermoplastic polyurethane (TPU) for a multitude of applications in this crucial time. Don’t miss out on business opportunities in COVID-19 Impact on Medical Tubing Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The global polyurethane additives market is projected to grow from USD 3.7 billion in 2020 to USD 4.5 billion by 2025, at a CAGR of 4.2%. The demand for polyurethane additives in emerging economies, such as APAC and South America, is increasing owing to the growing construction industry. The volatility in raw material prices and the recyclability of polyurethanes is hindering the polyurethane additives market. The demand for polyurethane additives is increasing, owing to the growing demand for innovative and cost-effective additives. This increase in demand for bio-based polyurethane additives provides growth opportunities to the market. On the other hand, the increasing regulatory pressure towards the usage of bio-based products is the major challenges for the market.

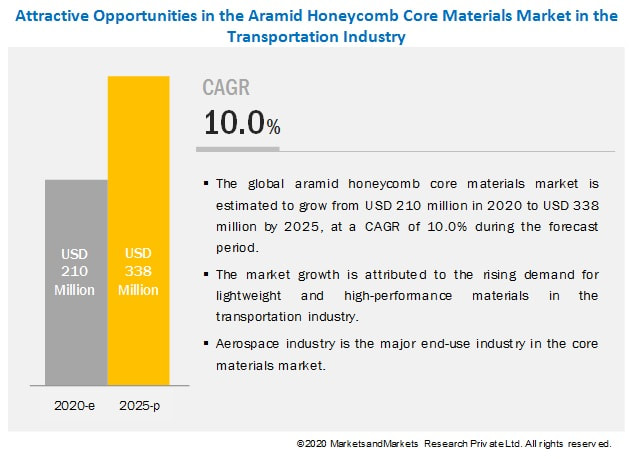

Download PDF Brochure to Know More: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=121317889 Automotive & transportation segment is estimated to lead the overall polyurethane additives market Polyurethanes are used in various parts of an automobile. In addition to the foam that makes car seats comfortable, bumpers, interior “headline” ceiling sections, the car body, spoilers, doors and windows all use polyurethanes. Polyurethane enables manufacturers to provide drivers and passengers significantly more automobile mileage by reducing weight and increasing fuel economy, comfort, corrosion resistance, insulation, and sound absorption. Foams segment is estimated to lead the polyurethane additives market Polyurethane foams are manufactured by reacting polyols and isocyanates in the presence of a blowing agent and an amine catalyst. The blowing agent is carbon dioxide, which is formed as a by-product of the reaction between water and isocyanate. The amine catalyst is known to accelerate the reaction. Polyurethane foams are of two types, namely rigid polyurethane foam and flexible polyurethane foam. Foams offer various properties such as comfort and insulating properties when used in various industries such as automotive and building & construction, which is driving the market. APAC is projected to be the fastest-growing market for polyurethane additives. The rising population, increased demand for automobiles, growing disposable income, rapid industrialization, and increased urbanization are driving the APAC polyurethane additives market. China is the largest market for polyurethane additives in the region. China is also a major producer and consumer of polyurethane additives in the region as it has a huge manufacturing base. Apart from China, India and South Korea are projected to grow at a decent rate during the forecast period. The key players in the non-phthalate plasticizers market include Evonik Industries (Germany), BASF (Germany), Huntsman Corporation (US), Covestro (Germany), Dow Inc. (US), Lanxess AG (Germany), lbemarle Corporation (US), Tosoh Corporation (Japan), Momentive (US), and BYK (US). These players have established a strong foothold in the market by adopting strategies, such as expansion and new product launch. Request For Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=121317889  Aramid honeycomb core materials are used in interior and exterior applications of aircraft, automobiles, ships, and rails. The demand for these materials is increasing at a rapid pace, owing to their lightweight and increase in fuel efficiency of vehicles facilitated by their use. However, amidst the global COVID-19 pandemic, the demand from the aforementioned vehicle types is expected to show a sharp decline until 2021. The global aramid honeycomb core materials market in the transportation industry size is projected to grow from USD 210 million in 2020 to USD 338 million by 2025, at a CAGR of 10.0% during the forecast period.

Companies have strengthened their position in the global aramid honeycomb core materials market in the transportation industry by adopting expansions as the major strategy. From 2015 to 2020, expansion was the key strategy adopted by the market players to maintain growth in the global aramid honeycomb core materials market in the transportation industry. For instance, Plascore Inc. (US) invested USD 6 million to expand its aerospace business unit in Zeeland, Michigan, US. The company built a 73,500-square-feet addition onto its current plant, doubling the size of its facility. This expansion has helped the company to increase its production capacity at a competitive cost to meet the demand for the aramid honeycomb core materials from the aerospace customers. However, due to the outbreak of the COVID-19 pandemic, the demand for aramid honeycomb core materials from two of the major commercial aircraft manufacturers has decreased. The factors such as lockdown situation across national and international borders, closure of manufacturing facilities, disruption in the supply chain, and zero orders for new aircraft for Boeing and Airbus in January and February, respectively have resulted in a decline in the demand for aramid honeycomb core materials in the transportation industry. To know about the assumptions considered for the study download the pdf brochure Recent Developments

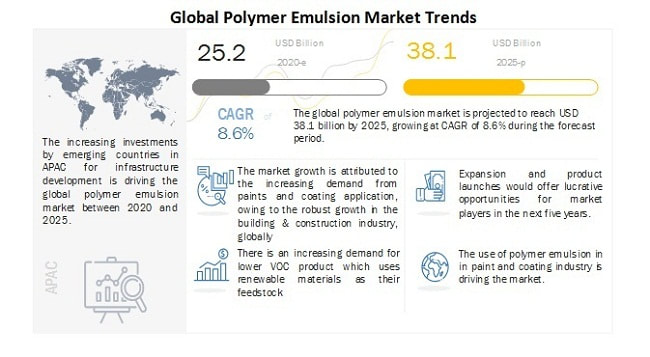

Request For Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=129593005 Company Name: MarketsandMarkets Contact Person: Mr. Aashish Mehra Email: [email protected] Phone: 18886006441 Address:630 Dundee Road Suite 430 City: Northbrook State: IL 60062 Country: United States Increased the demand for water-based paints & coatings drive the growth of polymer emulsions9/7/2020  The global polymer emulsion market size is projected to grow from an estimated value of USD 25.2 billion in 2020 to USD 38.1 billion by 2025, at a CAGR of 8.6% during the forecast period. The growth of the market is driven mainly by the increasing demand from growing end-use industries in emerging markets and stringent regulations regarding VOC emission.

Download PDF Brochure to Know More: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1269 The paints & coatings segment is the largest consumer of polymer emulsion. The growth of the market is attributed to the high demand in industries, such as construction and automotive. Polymer emulsion is used widely in paints & coatings as its manufacturing process has a lower carbon footprint. The high VOC content of solvent-based products and the implementation of government regulations regarding air pollution control has stimulated the development of low VOC paints & coatings. This increased the demand for water-based paints & coatings, which in turn, drive the growth of polymer emulsions in the paints & coatings segment. There is an increasing demand for polymer emulsion from various end-use industries such as paper, construction, textile, transportation, consumer durables, and others due to factors such as rapid urbanization, changing lifestyles, and growing disposable income. The use of polymer emulsion is rapidly increasing in these end-use industries for applications such as paints & coatings, adhesives & sealants, and others. APAC is the largest and fastest-growing market for polymer emulsion. The region is witnessing growth in the polymer emulsion market because of the rapid expansion of building & construction, consumer durables, and transportation sectors. The manufacturers are attracted to the region as skilled labor required for the operation of manufacturing units are available at lower wages. The presence of major polymer emulsion manufacturers and stringent government regulation related to VOC emission are major factors supporting the growth of polymer emulsion in the region. Key Market Players DIC Corporation (Japan), Dow Chemical Company (US), BASF SE (Germany), Arkema Group (France), Celanese Corporation (US), Trinseo (US), The Lubrizol Corporation (US), Wacker Chemie AG (Germany), Synthomer Plc (UK), and Asahi Kasei Corporation (Japan) are the major players in the polymer emulsion market. These companies have adopted several growth strategies to strengthen their position in the market. Expansion, new product development, merger & acquisition, and collaboration are the key growth strategies adopted by these players to enhance their product offering & regional presence to meet the growing demand for the polymer emulsion market from emerging economies. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1269 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed