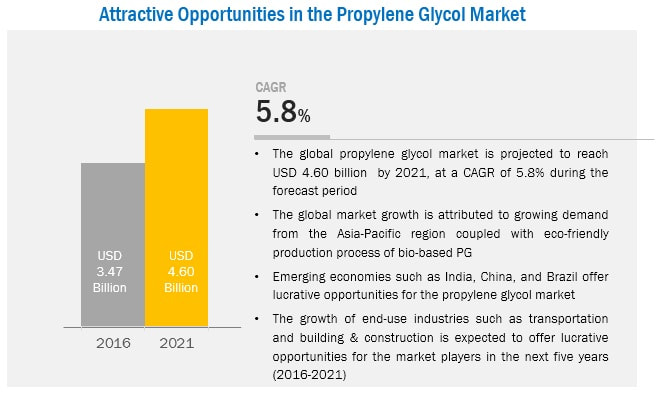

The global propylene glycol market was valued at USD 3.47 Billion in 2016, and is projected to grow at a CAGR of 5.8%, to reach USD 4.60 Billion by 2021. Eco-friendly production process of bio-based propylene glycol has led to the growth of the global propylene glycol market. Also, the growing automotive industry in Asia-Pacific is driving the market as propylene glycol is widely used in engine coolants and sheet molding compounds among others.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=264488864 The economic growth in the Asia-Pacific region is driving the market for propylene glycol. In addition, increased demand for propylene glycol in key countries such as China and India, are contributing to the growth of the propylene glycol market in the region. Currently, the global propylene glycol market is led by various market players such as The Dow Chemical Company (U.S.), LyondellBasell Industries N.V. (Netherlands), BASF SE (Germany), Archer Daniels Midland Company (U.S.), Global Bio-chem Technology Group Co., Ltd. (China), DuPont Tate & Lyle Bio Products Company, LLC (U.S.), Huntsman Corporation (U.S.), SKC Co., Ltd. (South Korea), Temix International S.R.L. (Italy), and Ineos Oxide (Switzerland) among others. Scope of the Report This report categorizes the global market for propylene glycol on the basis of source, application, end-use industry, and region. By Source: Petroleum-based Propylene Glycol Bio-based Propylene Glycol By Application: Unsaturated Polyester Resin Food, Pharmaceuticals & Cosmetics Antifreeze & Functional Fluid Liquid Detergents Plasticizers By End-Use Industry: Transportation Building & Construction Pharmaceuticals & Cosmetics Food & Beverage Request for sample report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=264488864 Transportation is expected to be the fastest-growing end-use industry Transportation is projected to be the fastest-growing end-use industry of the global propylene glycol market, mainly due the rising demand for propylene glycol in the automotive coolants, aircraft wings, pleasure boats, and ships. This industry in the Asia-Pacific region is anticipated to grow at the highest CAGR during the forecast year. The growth is attributed to increasing sales of automobiles in the region. In addition, improving standards of living and increasing disposable income in emerging countries such as India, China, and South Korea are driving the growth of the transportation industry. Also, China, Korea, Japan, and India are witnessing high demand for new ships for both military and commercial purposes.

0 Comments

MarketsandMarkets projects that the market for fiber cement will grow at USD 17.38 billion by 2021, at a CAGR of 4.80%. The market for fiber cement is segmented on the basis of material into Portland cement, sand, cellulosic fibers, and others. Portland cement dominated the market. However, the market for cellulosic fibers is projected to grow at the highest rate. With the emergence of new technologies, manufacturers are looking for advanced techniques to make fiber cement more effective.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=186027265 The siding segment is estimated to account for the largest share in the fiber cement market, on the basis of application and this trend is projected to continue during the forecast period. Fiber cement siding improves the aesthetic appeal of the buildings, making them look more expensive. Other applications such as molding & trim and roofing are projected to show potential growth. In fact, fiber cement roofing is projected to be the fastest growing application during the forecast period. Growing construction industry and strict regulations against the use of asbestos cement are important factors driving the market for fiber cement. On the basis of end use, the residential segment held the largest share, in 2015 and is projected to grow at the highest rate during the forecast period. This is primarily due to favorable and lenient lending policies initiated by governments across all regions. Also, the residential construction spending is estimated to go up, particularly in the emerging Asia-Pacific and Latin American regions. Fiber cement products’ aesthetic appeal, along with properties such as durability and low maintenance, has also driven the residential sector. Among regions, Asia-Pacific is projected to grow at the highest rate during the forecast period. Growing economy and rapid growth in the infrastructure sector in the Asia-Pacific region have significantly impacted the growth of fiber cement. The North American region, which is seeing a rebound in its residential construction sector, is projected to be the second-largest market. Read More: https://www.marketsandmarkets.com/PressReleases/fiber-cement.asp  The mining chemicals market is witnessing considerable growth due to rapid industrialization and infrastructure development. These chemicals are used to increase the efficiency and productivity of mining processes such as extraction and recovery of minerals from ores. Mining chemicals have across new opportunities due to decreasing grades of ores. MarketsandMarkets projects that the mining chemicals market size will grow from USD 6.02 billion in 2017 to USD 7.54 billion by 2022, at a CAGR of 4.60 %.

Please provide your specific interest in this report so as to help you better @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=205253671 On the basis of mineral type, the mining chemicals market is segmented into base metals, non-metallic minerals, precious metals, and rare earth metals. The base metals segment is projected to grow at the highest CAGR from 2017 to 2022. The high demand for mining chemicals in base metal processing is primarily attributed to the increasing complexity of ores and decreasing ore grades. The metals that have witnessed a constant rise in demand in the last few years include copper, aluminum, molybdenum, and tin. Copper has seen an increase in demand from key sectors such as electrical & electronics, automotive, industrial pipes & fittings, and others. On the basis of product type, the market is segmented into grinding aids, flocculants, collectors, frothers, and solvent extractants. These chemicals are used to enhance the metal/mineral recovery rate from ores. The grinding aids segment accounted for the largest share in 2016 and is also projected to grow at the highest CAGR over the next five years. This can be attributed to the deteriorating quality of ores and the increasing utilization of mining chemicals for the passing of complex ores. On the basis of application, the market is segmented into mineral processing, explosives & drilling, water & wastewater treatment, and others. The explosives & drilling segment accounted for the largest share in 2016 and is projected to grow at the highest CAGR during the next five years. The rising demand for deep-surface mining for the action of high-quality minerals is expected to contribute significantly to the growth of the explosives & drilling application. Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=205253671 The Asia-Pacific mining chemicals market is projected to grow at the highest CAGR from 2017 to 2022. Countries such as China and India are expected to witness high growth in the mining chemicals market. The high demand for mining chemicals in the country can be credited to the continuous exploration and beneficiation of ores. Additionally, high foreign investments in China’s mining industry are expected to support the application for mining chemicals in the country.  The market size of waste heat recovery system (WHRS) is projected to reach USD 65.87 billion by 2021, at a CAGR of 6.90% between 2016 and 2021. The focus on cost efficiency and stringent government regulations are expected to drive the demand for the WHR system market.

Waste heat recovery is the process of capturing residual heat from an existing industrial process and using it for other applications. Waste heat refers to the energy generated by various industrial processes. WHR technologies help in reducing the costs of operating facilities by enhancing their energy productivity. The energy recovered during this process is widely used in two major applications, namely, steam & electricity generation and preheating. Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=202657867 Market DynamicsDrivers

Global climate change is the greatest economic, political, developmental, and environmental challenge for counties worldwide. Enhancing energy efficiency is the cheapest and the most reliable method of curbing carbon emissions, thus saving costs. Supplying energy for sustainable economic development is a goal that is shared by both developed and developing countries. A study on trends in global CO2 emissions estimates that in the current global scenario, about 34.5 billion tons of CO2 is released in 2012, and despite several measures it has been increasing year-on-year. The need for energy has been rising steadily and according to the International Energy Agency’s (IEA’s) publication on climate change in 2015, the emissions will increase by 120% by 2050, while oil demand will rise by 65%. Apart from this, global warming is adversely affecting the environment. These environmental concerns have led to the increase in number of WHRS installations worldwide. The use of this system across European industries has increased, which resulted in the reduction of CO2 emissions. According to the DOE National Energy Modeling System (NEMS), by 2030, carbon emissions from power plants can be 84% lower than 2005 levels due to increasing environmental awareness and government regulations to reduce these emissions by installing such systems. This will provide impetus to the WHR equipment that helps in providing energy efficiency, thereby driving the market. Request for sample report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=202657867 Critical questions which the report answers

The market size of bioplastics& biopolymers is estimated at USD 6.95 billion in 2018 and is projected to reach USD 14.92 billion by 2023, at a CAGR of 16.5% from 2018 to 2023.

Growing consumption of bioplastics & biopolymers in the packaging industry, growing demand for bioplastics, and increasing environmental awareness drive the bioplastics & biopolymers market, globally. Download PDF Brochure The use of bio-based products is expected to increase owing to the growing environmental regulations. Thus, the bioplastics & biopolymers market is expected to witness high growth during the forecast period. Moreover, various regulations, such as banning or implementing additional surcharges on the usage of conventional plastics in shopping bags, packaging materials, and disposables applications, discourage the use of conventional plastics. This factor help in promoting bio-based and biodegradable products, thereby driving the bioplastics & biopolymers market. Non-biodegradable bioplastics & biopolymers is the fastest-growing type owing to their low price coupled with durability and robustness. These are used to substitute the plastics in applications such as shopping bags, food packaging, and disposables. Key end users are adopting these bioplastics to enhance their contribution to sustained growth. For instance, Coca-Cola introduced the Plant Bottle technology, where PET had been made from bio-based monoethylene glycol (from sugarcane) and terephthalic acid (from petrochemicals). Request for sample report Packaging is the fastest-growing end-use industry for bioplastics & biopolymers. The high growth in this segment is owing to the increasing use of bioplastics for manufacturing single-use compostable packaging materials including carry bags, food packaging, boxes, and laminating films. Bioplastics are widely used in food packaging, which is expected to witness a high growth potential during the forecast period. APAC is the fastest-growing market for bioplastics & biopolymers. In this region, there has been an increase in the consumption of bioplastics & biopolymers because of new regulations as well as marketplace advertising. Government regulations in APAC regarding the ban on plastic bags and global warming initiatives are also driving the market. In APAC, the market in China is expected to grow rapidly due to new capacity additions and government legislation. The consumer awareness regarding sustainable plastics along with the pressure from retailers contributes to the rising demand for bioplastics. Read More  Steel rebar are long steel products, which are used as reinforcement elements in Reinforced Cement Concrete (RCC). Steel rebars are hot rolled steel products and are used as reinforcement elements, along with concrete to effectively bear tensile, compression, and bending-in in concrete construction.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=176200687 ArcelorMittal (Luxembourg), Gerdau S.A (Brazil), Nippon Steel & Sumitomo Metal Corporation (Japan), Posco SS-Vina, Co. Ltd (Vietnam), Steel Authority of India Limited (India), Tata Steel Ltd. (India), Essar Steel (India), Mechel PAO (Russia), EVRAZ plc (U.K.), Sohar Steel LLC (Oman), Celsa Steel UK (U.K.), Kobe Steel Ltd. (Japan), Jiangsu Shagang Group (China), NJR Steel (South Africa), Commercial Metals Company (U.S.), The Conco Companies (U.S.), Barnes Reinforcing industries (South Africa), Jindal Steel & Power Ltd. (India), Steel Dynamics (U.S.), SteelAsia Manufacturing Corporation (Philippines), Outokumpu Oyj (Finland), Acerinox S.A. (Spain), Hyundai Steel (South Korea), Daido Steel Co., Ltd. (Japan), and Byer Steel (U.S.) are the key players in the steel rebar market. Steel rebar, owing to its heavy consumption in the construction segment, which includes infrastructure, housing, and industrial, is being widely used in the construction industry and in structural engineering. Some of the important strategies adopted by key companies to scale up their activities in the market are expansions, partnerships & joint ventures, acquisitions, contracts, and new product developments. These companies are also investing in R&D activities to strengthen their product portfolios and their positions in the steel rebar market. ArcelorMittal is the world’s leading steel and mining company, and produces approximately 114 million tons of crude steel. ArcelorMittal is the successor to Mittal Steel, a business originally set up in 1976. The company was founded in 2006 through the merger of Arcelor and Mittal Steel and is headquartered in Luxembourg City, Luxembourg. ArcelorMittal manufactures and supplies quality steel products to various industries, which include construction, automotive, packaging, and household appliances. ArcelorMittal produces blooms, rebars, billets, wire rods, sections, sheet piles, rails, and drawn wires, along with seamless and welded tubular products. The company, through its long business segment, serves industries, which include construction and mechanical engineering, automotive, and energy, among others. ArcelorMittal has a presence in 60 countries and an industrial footprint in 19 countries. Request for New Version of Report @ https://www.marketsandmarkets.com/RequestNewVersion.asp?id=176200687 The company focuses on both, organic and inorganic growth strategies for sustainable development. For instance, in Oct 2016, ArcelorMittal Brasil S.A. and Votorantim S.A. signed a definitive agreement for long steel business, which helps the company in increasing the production capacity of its long steel business. As a part of the inorganic growth strategy, ArcelorMittal and Nippon Steel & Sumitomo Metal Corporation have completed the acquisition of ThyssenKrupp Steel USA (U.S.) in February 2014, which helped the company in capacity expansion of hot rolling, cold rolling, coating, and finishing lines. For the growth of the steel segment, ArcelorMittal has engaged in various agreements, acquisitions, and contracts in recent years. Gerdau SA was founded in 1901 in Porto Alegre, Brazil. The company is the largest supplier of special long steel in the world, and is among the leading producers of long steel in the Americas. Gerdau is also the largest supplier to the automotive industry worldwide. For instance, in September 2015, Gerdau supplied 16,500 tons steel including reinforcing steel bars for expansion of the Tampa International Airport. Gerdau SA has a strong footprint across the globe, and presence in countries such as Argentina, Brazil, Chile, Columbia, Dominican Republic, Guatemala, India, Mexico, North America, Peru, Uruguay, and Venezuela. The company engages in the production and supply of steel products worldwide. It has a wide product portfolio, which includes shapes, rebars, drawn products, bars, billets, slabs, blooms, wire rods, and structural shapes. Gerdau SA also offers millions of tons quality steel through recycled scrap and serves industries such as agriculture, construction, automotive, and industrial. The company engages in the inorganic growth strategy through expansions. For example, in May 2013 the company expanded its production capacity for the steel operational facility of Knox County with expansions in the West Knox County. Don’t miss out on business opportunities in Steel Rebar Market. Speak to our analyst and gain crucial industry insights that will help your business grow. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed