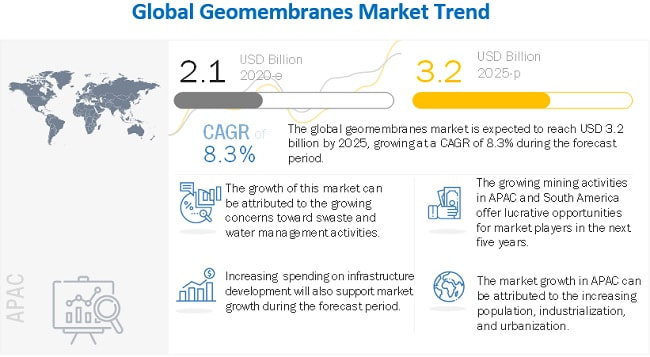

The global geomembranes market size is expected to grow from USD 2.1 billion in 2020 to USD 3.2 billion by 2025, at a Compound Annual Growth Rate (CAGR) of 8.3%. The major driving factors are increasing mining activities in APAC and South America and the growing concerns towards waste and water management activities.

To know about the assumptions considered for the study download the pdf brochure The HDPE is expected to hold the largest market size in the global geomembranes market HDPE, LDPE & LLDPE, PVC, EPDM, and PP are the major types of geomembranes available in the market. HDPE are the largest and fastest-growing segment in terms of value. These membranes are cost-effective and are used widely in all regions. They are designed to be used in applications, which require excellent chemical & UV resistance at an affordable cost. Their robust performance in critical applications is expected to help their high growth during the forecast period. The waste management application is expected to grow at the highest CAGR in the global geomembranes market Mining, waste management, water management, and civil construction are the major applications in the geomembranes market. Of these, waste management is estimated to be the fastest-growing application during the forecast period. Geomembranes are essential for controlling the leakage of contaminated gas and liquid into the surrounding environment. They are ideally used in landfill caps, landfill covers, landfill liners, temporary landfill closures, animal waste containment, and sludge treatment application due to their ability to accommodate differential settlement in the waste pile. North America is expected to hold the largest market size in the global geomembranes market during the forecast period Based on region, the geomembranes market has been segmented into APAC, Europe, North America, the Middle East & Africa, and South America. North America geomembranes market was the largest market in 2019. Market growth is primarily due to enormous potential in mining, wastewater management, and infrastructural activities in the US, Canada, and Mexico. Europe North America was the second-largest market for geomembranes owing to well-established manufacturing and construction sector of the region. Major vendors in the geomembranes market include Solmax (Canada), Raven Industries (US), AGRU (Austria), Carlisle Construction Materials LLC (US), Atarfil (Spain), PLASTIKA KRITIS (Greece), JUTA (Czech Republic), Maccaferri (Italy), Firestone Building Products (US), The NAUE group (Germany), Anhui Huifeng New Synthetic Materials (China), Carthage Mills (US), Environmental Protection (US), Geofabrics (Australia), Geosynthetics Limited (UK), Ginegar Plastic Products (Israel), Global Synthetics (Australia), Layfield Group (Canada), CETCO (US), Nilex (Canada), SOTRAFA (Spain), SOPREMA (France), Texel Industries Limited (India), Titan Environmental Containment (Canada), and US Fabrics (US). Don’t miss out on business opportunities in Geomembranes Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 Comments

The fire-resistant coatings market was USD 933 million in 2020 and is projected to reach USD 1,106 million by 2025, at a CAGR of 3.5% from 2020. Increasing awareness and emphasis on safety measures and preference for lightweight materials, which require additional protection, are expected to drive the market. The stringent regulations and norms are also supporting market growth, as the newly constructed buildings and manufacturing plants need to meet the required safety and fire resistance standards. Increasing urbanization and the growing building & construction industry are expected to provide growth opportunities in the market during the forecast period. The use of low-cost cementitious coatings in developing countries and in dry environments is expected to support market growth.

The leading players in the fire-resistant coating market include Akzo Nobel (Netherlands), PPG (US), Jotun (Norway), Sherwin-Williams (US), and Hempel (Denmark). The key industry players are adopting strategies to expand their presence and enhance their product portfolio through investments in R&D. To know about the assumptions considered for the study download the pdf brochure Due to the rise in the number of fire accidents at residential, public places, and workplaces, the number of deaths and damage to assets is also increasing. In view of this, end-users are increasingly adopting safety measures to protect people and property. Governmental agencies are also making rules regarding the addition of fire-resistant coatings in buildings to reduce these fire accidents. The COVID-19 pandemic has severely impacted North American and European countries. As a preventive measure, construction and industrial activities have been suspended. Several construction projects across the globe have been suspended, which has resulted in a decline in demand for fire-resistant coatings. Also, the disruption in the supply chain has been a major issue faced by the paints and coatings industry, which is expected to lead to a rise in the price of raw materials and other products. Companies have initiated the following developments:

Read More: https://www.marketsandmarkets.com/PressReleases/fire-resistant-coating.asp BASF (Germany) and ), Songwon (South Korea) are the Key Players in the Plastic Antioxidants Market9/23/2021  The plastic antioxidants market size is estimated to be USD 2.0 billion in 2020 and is expected to reach USD 2.6 billion by 2025, at a CAGR of 5.3% during the forecast period. Factors such as plastics replacing conventional materials, increasing demand in medical industry, and rapid urbanization in developing countries will drive the plastic antioxidants market. The major restraint for the market will be adverse effect on health from synthetic plastics antioxidants. However, the untapped demand in the agricultural sector of developing countries will act as an opportunity for the market.

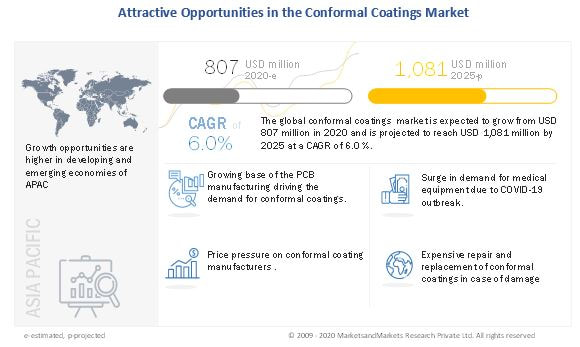

The key market players profiled in the report include BASF SE (Germany), Songwon (South Korea), Adeka Corporation (Japan), Solvay (Belgium), SK Capital (US), Clariant (Switzerland), Sumitomo Chemical (Japan), 3V Sigma S.p.A (Italy), and Dover Chemical Corporation (US). To know about the assumptions considered for the study download the pdf brochure Players in the plastic antioxidants market are mainly concentrating on new product launches, merger & acquisition, and expansions to meet the growing demand for plastic antioxidants for various applications. New product launches help companies to strengthen their product portfolio and meet the specific demands of customers. The growth of the plastic antioxidants market has been largely influenced by new product launches that were undertaken between 2016 and 2020. Companies such as BASF and Sumitomo Chemical have adopted new product launches to enhance their market position. BASF (Germany) is one of the major players in the plastic antioxidants market. In order to expand its business, the company is focusing on enhancing its market reach by opening plants to increase the capacity. For instance, in December 2019, BASF (Germany) opened the second phase of the new antioxidant manufacturing plant in Shanghai, China, to support the fast-growing antioxidants market in the country. Similarly, Sumitomo Chemical expanded its Polypropylene Compounds Business with the acquisition of a Turkish compounder, Emas Plastik A.S., and its affiliated companies (Emas Group). This would encourage the growth of the antioxidant business. The companies also adopted new product launch as a strategy to expand their product portfolio and market presence. For instance, in July 2019, SK Capital launched a new antioxidant product called ULTRANOX 626 for use in PP homopolymers and copolymers. In November 2018, launched a new antioxidant, SONGNOX 5057, for polyols and polyurethanes applications. In October 2018, SK Capital announced its agreement to acquire the SI group. Through this acquisition, the company is projected to unlock the growth in earnings from both commercial and cost synergies. In May 2017, Clariant undertook mergers with Huntsman Corporation (US) to form HuntsmanClariant, in which Clariant holds a 52% share. The combination of strengths of both the companies created a leading global specialty chemical company, with an improved growth profile in highly attractive regions and end markets. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=106598592  The Conformal coatings market is estimated to be USD 807 million in 2020 and is expected to reach USD 1,081 million by 2025 at CAGR of 6.0%. The growth of the conformal coatings market is attributed to the increasing number PCB manufacturers and demand from high end applications that require conformal coatings.

To know about the assumptions considered for the study download the pdf brochure The conformal coating market is impacted by the COVID 19, due to the disruption caused by it in the end-use industries globally:

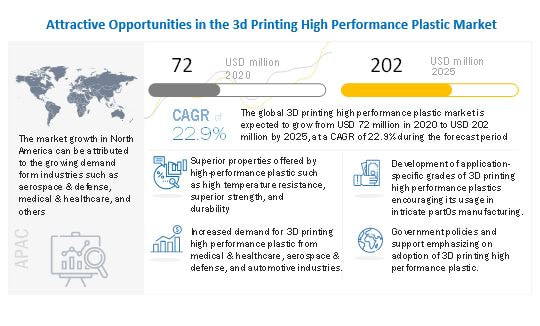

APAC is the largest market of conformal coatings, and this dominance is expected to continue till 2025. China is the key market in the region, consuming more than half of the demand for conformal coatings, followed by Taiwan, South Korea, and Japan. These countries are expected to witness a steady increase in consumption from 2020 to 2025. The region contributes close to 90% of PCB production in the world, and market is mainly driven by the presence of a large number of leading global electronics companies. PCB industry is quite fragmented as there are more than 100 companies that constitute close to 90% of overall PCB revenues and most of them belong to APAC, more so in China & Taiwan. Recent years have seen a lot of PCB manufacturing shifts to APAC due to cost-effectiveness and closer access to customers in the region, hence the increase in consumption of conformal coatings. The key companies in the conformal coatings are Henkel (Germany), Illinois Tool Work (US), Shin-Etsu Chemical (Japan), Dow (US), H.B. Fuller (US), Chase Corporation (US), Electrolube (UK), Dymax Corporation (US), MG Chemical (Canada) and Specialty Coating System (US). Don’t miss out on business opportunities in Conformal Coating Market Speak to our analyst and gain crucial industry insights that will help your business grow.  3D printing is being used in various industries across the globe as it reduces the operating time and cost and enables mass production of goods. Governments of different countries around the world are taking initiatives to support the adoption of 3D printing high performance plastic in various industries. For instance, in 2018, the UK government announced an investment of approximately USD 150 million to the Advanced Manufacturing Research Centre in Rotherham and Sheffield and the Nuclear Advanced Manufacturing Research Centre in Rotherham. Furthermore, in 2016, the South Korean government announced a further investment in 3D printing to adopt it in various sectors. The UK government issued a funding call for about USD 5.5 million for 3D printing in 2016. In December 2020, the Government of India’s Ministry of Electronics and Information formulated a 3D printing policy to develop a conducive ecosystem for local firms.

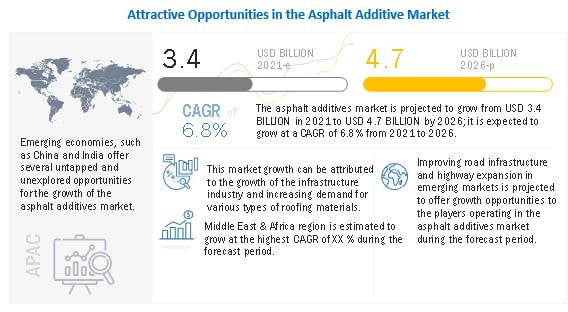

To know about the assumptions considered for the study download the pdf brochure Government initiatives such as reimbursement policies and funding, coupled with various mergers and acquisitions among small and big firms for technological advancement, are boosting the growth of the 3D printing high performance plastic market. Initiatives by governments of different countries of Europe and Asia Pacific regions to carry out improvements in 3D printing technologies have led to the increased demand for these materials in various industries. 3D printing high performance plastic. The global 3D printing high performance plastic market is expected to grow from USD 72 million in 2020 to USD 202 million by 2025, at a CAGR of 22.9% during the forecast period. Increasing demand from high end-use industries, growing novel application in tooling and proptotying, and government supportive activities to promote the usage of 3D printing materials is driving the growth of the market. Medical & healthcare industry dominates the market The medical & healthcare industry led the 3D printing high performance plastic market. The industry is continuously looking to adopt breakthrough technologies and materials to cater to the medical requirements of humans. High compatibility of 3D printing high performance plastic such as polyamide has increased its application in making of medical devices, surgical equipment, prosthetics & implants, and tissue engineering products supporting the growth of the market. North America to continue the similar growing trend in the 3D printing high performance plastic market North America held the largest share in 3D printing high performance plastic market and is projected to continue the similar trend over the projected period. Manufacturers of 3D printing materials in North America are putting efforts by undertaking new product launch, collaboration, and other strategies. For instance, in September 2018, Stratasys Ltd. signed a multi-year technical partnership with Team Penske (US). Team Penske will be using advanced materials, such as Carbon Fiber-filled Nylon 12, in additive manufacturing for advanced car testing, production parts, and prototypes. The partnership is aimed at innovating new materials in 3D printing to increase output and improve vehicle performance. Arkema S.A. (France), Royal DSM N.V. (the Netherlands), Stratasys, Ltd. (US), Evonik Industries AG (Germany), 3D Systems Corporation (US), EOS GmbH Electro Optical Systems (Germany), Victrex plc. (UK), Solvay (Belgium), Oxford Performance Materials (US) , and SABIC (Saudi Arabia) are some of the key players in the 3D printing high performance plastic market.. These players have taken different organic and inorganic developmental strategies over the past five years. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=216044197  The pandemic is estimated to have impact on various factors of the value chain of asphalt additives market, which is expected to reflect during the forecast period, especially in the year 2020 to 2021. The various impact of COVID-19 are as follows:

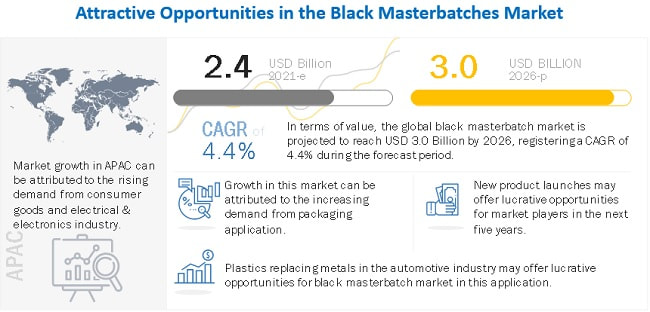

IMPACT ON ASPHALT ADDITIVES: The COVID-19 pandemic resulted in supply chain disruption and delayed construction projects across the world. Strict lockdowns and curfew in most of the countries was imposed to break off the spread of coronavirus. This resulted into economic downfall where construction was one of the severely impacted sectors due to shortage of raw materials, labor force, and government regulation to put to a hold ongoing project. Although in the third quarter of 2020, many local governments took initiatives to resume the construction work related to roads, highways, and buildings. Federal Ministry of Transport and Digital Infrastructure (BMVI) in Germany resumed building construction and road construction since April 2020. Countries such as Romania and India have resumed the construction of highways and roads since the second half of 2020. Thus, the construction sector is expected to witness a high growth in 2021 when compared to the previous year. To know about the assumptions considered for the study download the pdf brochure The asphalt additive market is projected to grow from USD 3.4 billion in 2021 to USD 4.7 billion by 2026, at a CAGR of 6.8% from 2021 to 2026. Increase in road construction projects along with the growing usage of asphalt additives in roofing application are some of the major key factors driving the growth of the asphalt additive market across the globe. Hot mix technology held the largest share of the global asphalt additives market Based on technology, the hot mix technology is expected to lead the asphalt additives market in coming years. Hot mix asphalt is durable, resistant to moisture damage and thermal cracking. It also provides excellent workability and skid resistance. This segment is growing due to developments in the construction of new highways and expressways. The Asia Pacific region was the largest market for asphalt additives in 2020 The Asia Pacific region was the largest market for asphalt additives in 2018, owing to the increasing demand for asphalt additives products in developing economies, such as India and China. China is the leading consumer of asphalt additives products in the Asia Pacific region. The huge growth and innovation, along with industry consolidations, is expected to drive the growth of the Asia Pacific asphalt additives market. Nouryon (Netherlands), DowDuPont (US), Arkema SA (France), Honeywell International Inc. (US), Evonik Industries (Germany), Huntsman Corporation (US), Kraton Corporation (US), Ingevity Corporation(US), and BASF SE (Germany) are some of the leading players operating in the asphalt additive market. Don’t miss out on business opportunities in Asphalt Additive Market. Speak to our analyst and gain crucial industry insighs that will help your business grow.  The black masterbatches market is projected to reach USD 3.0 billion by 2026, at a CAGR of 4.4 % from USD 2.4 billion in 2021. Black masterbatch is manufactured from carbon black pigment. It typically contains 30.0%–50.0% carbon black. Based on the specific plastic product, the carrier of carbon black is decided. For instance, PS products use PS as the carrier of carbon black. Black masterbatch is used in different polymers such as polypropylene (PP), low-density polyethylene (LDPE), linear low-density polyethylene (LLDPE), high-density polyethylene (HDPE), polyvinyl chloride (PVC), polyethylene terephthalate (PET), polystyrene (PS), polyurethane (PUR). Some of the important end-use industries of black masterbatch are packaging, infrastructure, automotive, electrical & electronics consumer goods, fibers, and agriculture.

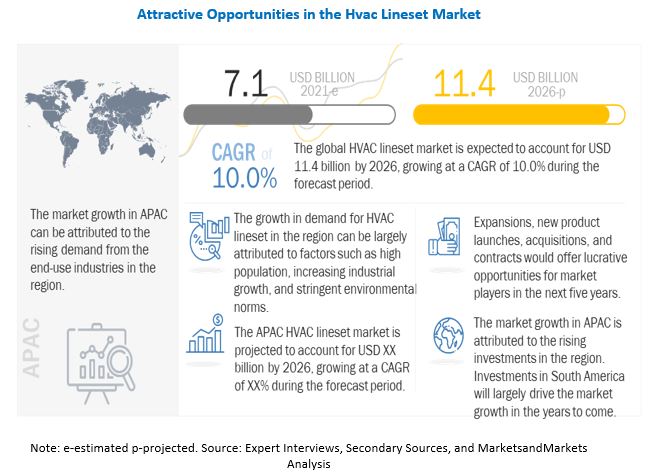

To know about the assumptions considered for the study download the pdf brochure The growing industrialization in emerging economies, such as China, India, South Korea, Indonesia, Thailand, Taiwan, Mexico, Brazil, and Argentina, is expected to drive the black masterbatch market in the next five years. The high demand from the packaging, building & construction, consumer goods, automotive, and agriculture applications in these countries increase the need for black masterbatch, especially for plastics used in these applications. The implementation of government policies supporting the growth of industries, low labor costs, skilled workforce, availability of raw materials, and increasing urbanization have enabled domestic and foreign companies to establish their facilities in these countries. The growth of the manufacturing industry in Malaysia, Vietnam, Colombia, and Chile is also expected to fuel the market growth. Automotive is the largest end-use industry of the black masterbatches market. APAC was the largest market for black masterbatches in 2020, in terms of both volume and value. Factors such as growing demand from packaging industry, rapid industrialization in growing economies like China, India & Thailand and increasing demand for plastic molds in electric vehicles will drive the black masterbatches market. Europe is the second-largest black masterbatches market in the world. Key countries in the region include Germany, France, the UK, and Spain. As the market in Europe is mature, it is projected to grow at a lower CAGR during the next five years. Europe has always been a major black masterbatches market due to presence of developed automotive sector in the region. This market is more growing due to high demand of plastic molds in electric vehicles. Key countries such as Germany and France have shown promising demand for black masterbatches which is expected to continue in the near future. Key players in this market are LyondellBasell (US), Avient Corporation (US), Ampacet Corporation (US), Cabot Corporation (US), Plastika Kritis S.A. (Greece), Plastiblends India Ltd. (India), Hubron International (UK), Tosaf Group (Israel), and Penn Color, Inc. (US). The global and regional players have sizable shares in the black masterbatch market. The key players in the market are focusing on strategies, such as new product launches, partnerships & agreements, acquisitions, and expansions, to expand their businesses globally. Don’t miss out on business opportunities in Black Masterbatches Market. Speak to our analyst and gain crucial industry insights that will help your business grow. Urbanization and increase in residential construction are driving the HVAC Linesets Market9/20/2021  One of the key drivers propelling the HVAC demand on a global level is urbanization. The urbanization rates in industrial countries are above 75%, whereas urbanization is still in a relatively early stage in developing countries. This is particularly true in the case of South Asia, Sub-Saharan Africa, and Southeast Asian regions, where approximately 50% of people live in urban areas. According to Atlantic Council, India, with a population of approximately 1.4 billion, is expected to reach 46% of urbanization by 2040. Indonesia, Malaysia, Thailand, the Philippines, Singapore, and Vietnam are expected to witness strong growth in the residential construction sector. For instance, as per the Construction Outlook for Asia, the Indonesian construction industry, driven mainly by government investment in energy infrastructure, is expected to continue to expand at a healthy rate, with investments in housing, transport, and tourism infrastructure projects continuing to drive growth.

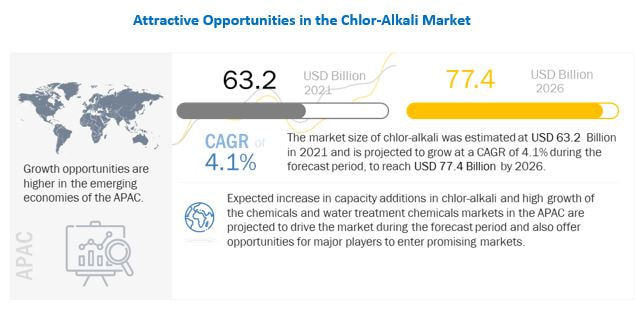

To know about the assumptions considered for the study download the pdf brochure Residential construction is estimated to be the second-largest market in the Indonesian construction industry accounting for 25.8% of the construction sector in the country in 2018. This is followed by energy and utility construction, commercial construction with a 7.8% share in the construction sector of Indonesia, industrial construction with 6.3%, and institutional construction with 3.5%. Additionally, as per the Construction Outlook for Asia, residential construction was one of the primary markets in the construction sector of Singapore and the Philippines in 2018. These factors are expected to support the growth of the HVAC industry in developing countries, thereby propelling the demand for line sets, particularly for the residential and commercial end-use industries. Also, new buildings in urban areas will enhance electricity consumption, especially through demand for air conditioning and ventilation in hot and tropical environments. As per Bloomberg’s New Energy Outlook 2019 estimates, air conditioning use will double in emerging countries by 2050, with air conditioning consumption reaching 5376 TWh or 12.7% of projected global electricity demand. Also, in the US, buildings accounted for nearly 75% of electricity consumption in 2018. Furthermore, as per the US Energy Information Administration (EIA), the US will gain more than 58 million people and 24 million households by 2050, and the total square footage of US residences will expand by 33%. By 2050, 71% of households will be in single-family homes, which typically have more air-conditioned floor space than multifamily or mobile homes. These factors are collectively expected to contribute to the overall growth in the HVAC industry, thereby cascading the growth of the line sets market on a global level. The global HVAC linesets market size is projected to reach USD 11.4 billion by 2026 at a CAGR of 10.0% from USD 7.1 billion in 2021. Urbanization and increase in residential construction, growing trends of smart homes, increasing demand for air conditioners, and significant growth in number of data centers and their power density are driving the HVAC lineset market. Browse 186 market data Tables and 67 Figures spread through 231 Pages and in-depth TOC on “HVAC Linesets Market by Material Type (Copper, Low Carbon), End-Use (Residential, Commercial, Industrial), Implementation (New Construction, Retrofit), and Region (APAC, North America, Europe, MEA, South America) – Global Forecast to 2026” Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=209588791  The global Chlor-Alkali market size is estimated to be USD 63.2 billion in 2021 and is projected to reach USD 77.4 billion by 2026, at a CAGR of 4.1% between 2021 and 2026. The growth in demand for chlor-alkali in the APAC is expected to be driven by the vinyl chain (EDC/VCM/PVC). The demand for chlor-alkali in the APAC is driven by China, which accounts for a major share, globally. China is one of the fastest-growing countries, in terms of chlor-alkali consumption, due to its large chemical and petrochemical industries. India, with its emerging economy is expected to propel the demand for chlor-alkali products during the forecast period.

To know about the assumptions considered for the study download the pdf brochure Chlor-alkali products such as chlorine, caustic soda, and soda ash play a vital role in the chemical industry. These products are necessary raw materials in major bulk chemical industries and utilized in various industrial and manufacturing value chains. The products are used in different applications such as plastics, alumina, paper & pulp, and others and find applications in diverse end-use industries (construction, automotive, and others). Thus, rising chemical output and strong economic conditions in emerging countries are expected to drive the growth of the chlor-alkali market.

The leading players in the Chlor-Alkali market are Olin Corporation(US), Westlake Chemical Corporation (US), Tata Chemicals Limited (India), Occidental Petroleum Corporation (US), Formosa Plastics Corporation (Taiwan), Solvay SA (Belgium), Tosoh Corporation (Japan), Hanwha Solutions Corporation (South Korea), Nirma Limited (India), AGC, Inc. (Japan), Dow Inc. (US), Xinjiang Zhongtai Chemical Co. Ltd. (China), INOVYN (UK), Ciner Resources Corporation (US), Wanhua-Borsodchem (Hungary), and others. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=708  The cost incurred on end-use industries due to corrosion is an important factor driving the demand for corrosion inhibitors. Total costs of corrosion include the design & construction or manufacturing, the cost of corrosion-related maintenance, repair & rehabilitation, and the cost of depreciation or replacement of structures damaged due to corrosion. These costs vary from industry to industry. According to NACE International (National Association of Corrosion Engineers), the annual cost of corrosion to the oil & gas industry in the US alone is estimated at USD 27 billion. The costs can be reduced by the broader application of corrosion-resistant materials and the application of corrosion-related technical practices. Corrosion inhibitors suppress or mitigate the corrosion process of metals. They protect the metals or alloys by acting as a barrier by forming an absorbing layer or by retarding the cathodic, anodic processes causing corrosion. The use of corrosion inhibitors in these industries lowers the maintenance and repair costs, extends the useful life of the equipment, and reduces the production loss from corrosion damage. This directly reduces the corrosive costs and drives the market for corrosion inhibitors.

To know about the assumptions considered for the study download the pdf brochure The growth in the power, oil & gas, mining, and chemical industries, especially in the emerging economies, such as China, Brazil, India, Indonesia, Malaysia, Argentina, Chile, and Vietnam, drives the market for corrosion inhibitors. The exploration and development of new oil fields such as the pre-salt oil fields in Brazil, installation of new and high capacity power plants using fossil fuels, nuclear, or solar power as fuel in China and India, and the growing mining industry as a result of the increasing demand from the construction sector is expected to further drive the corrosion inhibitor market during the forecast period. The global corrosion inhibitors market size is projected to reach USD 10.1 billion by 2026 at a CAGR of 4.9% from 2021. The increasing demand for corrosion protection chemicals in various end-use segments coupled with stringent regulatory and sustainability mandates concerning the environment is driving the market for corrosion inhibitors. Water Treatment application will account for the major share of the corrosion inhibitor market Water treatment accounted for 44.4% of the total corrosion inhibitor market in terms of application, in 2020. Corrosion can cause many concerns such as rusting of pipelines, equipment surfaces, and lowered efficiency of the equipment mainly in the industrial sector. Feed water use in various industries contains carbon dioxide which is corrosive to steel. If this carbon dioxide is left untreated, iron deposits on the boilers. These corrosion inhibitors are fed downstream of the deaerating equipment. It is volatilized and carried out with the steam after reacting with carbon dioxide. Corrosion inhibitors for boiler treatment include neutralizing and filming amines for condensate linings. Morpholine, cyclohexylamine, diethylethanolamine (DEAE), aminomethyl propanol, and aqua ammonia octadecylamine (ODA) are some of the common corrosion inhibitors used to protect boiler systems from corrosion. The Middle East & Africa region is the second fastest-growing region for the corrosion inhibitor market The region has emerging markets, such as Saudi Arabia, the UAE, Iran, Kuwait, and South Africa. The region has established oil & gas and chemical & petrochemical industries due to the abundant availability of natural resources. The oil & gas industry in the region is growing at a steady pace due to rising exports and increased exploration of reserves. Huge investments, rising population, growing disposable income, and integration of production activities are likely to increase output in the form of fuel and feedstock and, in turn, drive the corrosion inhibitors market. Major players operating in the global corrosion inhibitor market include Solenis (US), Nouryon (The Netherlands), Baker Hughes Company (US), Ecolab (US), BASF SE (Germany), SUEZ Water Technologies & Solutions (France), DOW Chemical Company (US), Lubrizol Corporation (US), Lanxess (Germany), and Henkel Corporation (Germany). Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=246 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed