Automotive industry is expected to witness the significant growth in Co-fired ceramics Market4/27/2020  Co-fired ceramics are finding increasing application in the automotive segment. This growing use of co-fired ceramic in the automotive industry is mainly due to the demand for high performance and compact electronic components. The co-fired ceramic is used in the form of LTCC and HTCC in various applications in the automotive industry. The co-fired ceramic is used widely in engine control units, transmission control units, electronic power steering, engine management system, antilock brake systems, airbag control modules, LEDs (automotive lighting), entertainment & navigation systems, pressure control modules, pressure sensor, radar modules, and various sensor modules in vehicles.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=126252032 The LTCC market and HTCC market is projected to grow from USD 916 million in 2019 to USD 1.1 billion by 2024, at a CAGR of 4.5 % between 2019 and 2024. The market is growing due to the high demand from the automotive, telecommunications, aerospace & defense, and medical end-use industries. Co-fired ceramic has good mechanical properties, such as excellent physical, chemical inactivity, hermicity, and high thermal stability properties. The automotive end-use industry requires co-fired ceramics to have more functionality in electronic devices, electronic packaging solutions to be smaller, lighter, more complex, operate at higher frequencies, and accommodate more components per unit area. The thermal stability properties of co-fired ceramic help manufacturers in increasing the overall efficiency of automotive. The Asia Pacific is one of the leading LTCC market and HTCC market. The region has a presence of major co-fired ceramic manufacturers who focus on the adoption of various business strategies to increase the production of co-fired ceramic and meet the growing demand from end users. For instance, KOA Corporation acquired VIA Electronic GmbH to extend its LTCC market and HTCC market in Japan, in June 2017. Key Questions Addressed by the Report

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

0 Comments

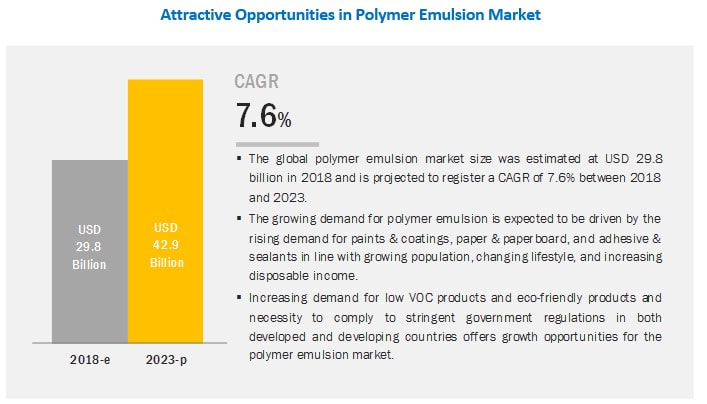

The polymer emulsion market is projected to grow from USD 29.8 billion in 2018 to USD 42.9 billion by 2023, at a CAGR of 7.6%. The global polymer emulsion market is expected to be driven by various factors such as increasing demand from end-use industries, especially in the emerging economies. Stringent government regulations related to VOC emissions also drives the polymer emulsion market.

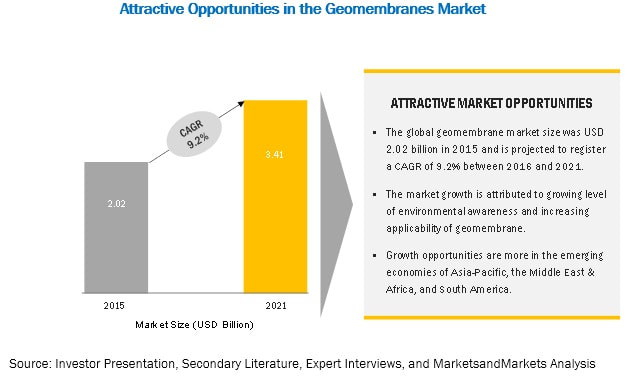

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1269 Based on application, the polymer emulsion market is segmented into paints & coatings, adhesives & sealants, paper & paperboard, and others. The paints & coatings application segment is projected to lead the overall polymer emulsion market during the forecast period. Polymer emulsion is preferred for paints & coatings applications owing to their low VOC content. Moreover, polymer emulsion paints & coatings are not flammable, which reduces its storage & handling charges and fire insurance costs. The manufacturing process of polymer emulsion paints & coatings entails lower carbon footprint as they consume less energy. Other reasons contributing to the use of polymer emulsion paints & coatings are low cost of handling and post painting cleanup cost. Acrylics are one of the most commonly used polymer emulsion, owing to their high durability and lack of VOC content. Furthermore, acrylics are used to prepare polymers with rigid, flexible, ionic, nonionic, hydrophobic, or hydrophilic properties. They are transparent, have resistance to breakage, provide excellent finish gloss, improved adhesion to non-porous surfaces, and good flow and stability. Recent Developments In March 2018, BASF SE (Germany) expanded its production facilities of Joncryl water-based emulsions at its Ludwigshafen site. This will strengthen the company’s position as a leading manufacturer of water-based resin and emulsion which are used in overprint varnishes, printing inks, as well as functional coatings for flexible packaging and paper & board applications. Request for sample report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1269 The APAC region is the largest consumer of polymer emulsion across the globe. Increasing infrastructure development, expansion in industrial & automotive sectors, strong economic growth, and increasing middle-class population are driving the demand for polymer emulsion in different applications. In APAC, countries such as China, Japan, and India are the largest consumers of polymer emulsion due to their increasing manufacturing output and rapid urbanization. The regulatory bodies and the regional governments have started addressing VOC emission issues with the help of stringent rules and regulations, which increases the demand for green products. This is also expected to fuel the demand for polymer emulsion.  The Geomembranes Market is expected to grow from USD 2.2 billion in 2016 to USD 3.4 billion by 2021, at a compound annual growth rate (CAGR) of 9.2% during the forecast period. The increasing environmental awareness and demand for freshwater resources are triggering the use of geomembranes in the water management application, thereby driving the market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=133281673 Market Dynamics Driver: Growing level of environmental awareness Geomembranes can efficiently prevent the leakage of poisonous fluids, harmful gases, among other pollutants at an affordable cost, which reduces damage to the environment. It is widely used in various landfill sites all over the world, owing to its stability and safety during use on landfill sites. Restraint: Fluctuating prices of raw materials The primary raw material required to manufacture geomembranes are HDPE, LDPE/LLDPE, PVC, PP, EPDM, and others. The price and availability of the aforementioned raw materials are directly dependent on crude oil. The prices of materials such as polyethylene and propylene are very volatile, making the price of end products inconsistent. Opportunity: Development of resilient geomembranes to sustain in harsh operational conditions Geomembranes are vital products in protecting water from hazardous solid and liquid waste materials. These act as hydraulic barriers in the purification processes and also as a gas barrier, preventing air pollutants from escaping. They are used in the waste containment projects, landfills, leachate pads during mining, refineries, and many other applications. Challenge: Dependency on government authorizatio Geomembranes are mostly used in public projects such as mining, canals, reservoir, power plants, and others. These projects have involvement of various government organizations and some public-private partnerships (PPP). Such projects are highly prone to delays caused by slack in financial clearances, environmental approvals, and other approvals from the respective authorities. Request for sample report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=133281673 In 2015, North America was the leading geomembranes market. Geomembranes are used extensively in the waste management application in the region. Increased environmental awareness and initiatives related to environmental protection and the use of geomembranes for waste management have helped in the growth of the market. The US is the dominant market in North America. The key players operating in the geomembranes market include GSE Environmental, LLC (US), Agru America, Inc. (US), Solmax International, Inc. (Canada), Atarfil SL (Spain), NAUE GmbH & Co. KG (Germany), Officine Maccaferri S.p.A (Italy), Colorado Lining International, Inc. (US), Firestone Building Products Company, LLC (US), Plastika Kritis S.A. (Greece), and Carlisle SynTec Systems (US).  Plasticizers are the colorless and odorless chemicals mainly phthalate esters, which are used to enhance the elasticity of polymers mainly polyvinyl chloride (PVC). Around more than 90% of plasticizers are used in production of PVC also known as vinyl. Plasticizers are also used in paints, rubber products, adhesives & sealants, printing inks and so on. Without the use of plasticizers in PVC applications, it will be rigid and can be used in limited applications such as wastewater pipelines.

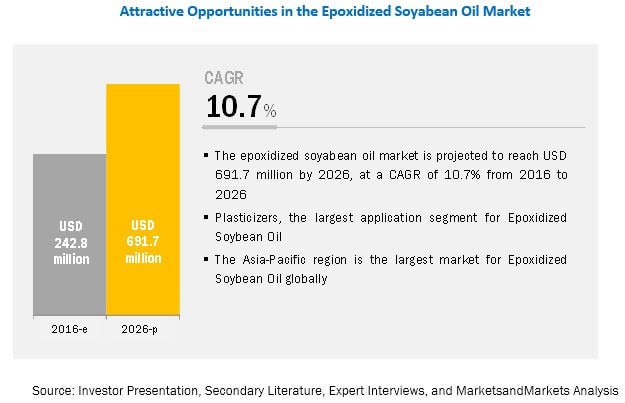

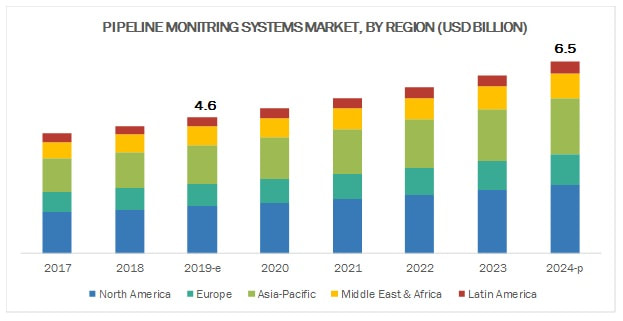

The most commonly used phthalates are hexyl phthalate, dioctyl phthalate, and dibutyl phthalate. This in turn led the plasticizer producers to opt for renewable and safer products. Epoxidized Soybean Oil Market, being environmentally friendly plasticizer, has been considered as most preferred bio-based plasticizer over petrochemical-based plasticizer. Hence, Epoxidized Soybean Oil Market finds high growth opportunities in PVC stabilization process. The global Epoxidized soybean oil (ESBO) market is projected to be valued at USD 691.7 million by 2026, at a CAGR of 10.70%. Further, the global demand for epoxidized soybean oil in the North American, Asia-Pacific, and European regions is growing due to stringent environmental regulations. Epoxidized soybean oil is preferred as against phthalate-free stabilizers in PVC applications, and hence ESBO is used widely as an additive in plasticizers. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=27777113 The North American region is the largest market in the global epoxidized soybean oil market, in terms of value, and this trend is expected to continue till 2026. Countries in this region such as U.S, Canada and Mexico are achieving symbolic increase in the use of epoxidized soybean oil in the plasticizer application industry. This growth is due to the easy availability of raw materials in large quantities and at lower costs, which is driving the demand for epoxidized soybean oil in this region. U.S is the largest market for epoxidized soybean oil and is projected to continue this trend till 2026. Key Market Players The epoxidized soybean oil supply chain includes raw material manufacturers such as Arkema SA (France), CHS INC. (U.S.), Ferro Corporation (U.S.), Galata Chemicals (U.S.), The Chemical Company (U.S.), Hairma chemicals (GZ) Ltd. (China), SHANDONG LONGKOU LONGDA CHEMICAL INDUSTRY CO., LTD (China), Guangzhou Xinjinlong Chemical Additives Co. Ltd. (China) among others. To speak to our analyst for a discussion on the above findings, click Speak to Analyst  Pipeline monitoring is a single system that detects smaller leaks or damages in pipelines securely and more reliably, while, simultaneously, monitoring them for third-party interferences and other external threats to prevent leaks. MarketsandMarkets projects that pipeline monitoring system market size will grow from USD 4.6 billion in 2019 to USD 6.5 billion by 2024, at a compound annual growth rate (CAGR) of 7.1% from 2019 to 2024. The increase in demand for pipeline monitoring systems for crude & refined oil is driving the growth of the pipeline monitoring system market.

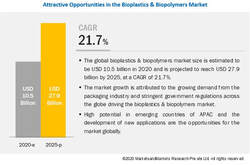

Key players in the pipeline monitoring system market are Siemens AG (Germany), Honeywell International Inc. (U.S.), BAE Systems (U.K), Perma Pipes (U.S), Transcanada (Canada), PSI AG (Germany), Pure Technology (Canada), Orbcomm Inc. (U.S.) and Huawei (China). Other players include Atmos International (U.K.), Clampon AS (Norway), ABB Group (Switzerland), Future Fiber Technologies (Australia), Senstar Inc. (Canada), Syrinix (UK), Radiobarrier (Russia), TTK (France), Krohne Group (Germany.), and Thales Group (France). These players have adopted various strategies to expand their global presence and increased their market share. To know about the assumptions considered for the study download the pdf brochure The pipeline monitoring system market has witnessed several strategies, such as expansions & investments, agreements, and contracts & partnerships, in 2018, by key players, who have used them to expand their product & service portfolio and improve their distribution networks. New product developments, merger & acquisitions, were the second-most adopted key strategies that were followed by market players to expand their product portfolios and for geographical reach to untapped markets. Siemens AG (Germany) provides integrated pipeline monitoring systems that are based on access control, intrusion detection, and video surveillance systems, which help to monitor pipeline systems from remote locations. All systems are controlled by one or more central control rooms, which provide end-to-end pipeline monitoring solutions. In December 2017, Pipeline 4.0 was launched by Siemens to meet the evolving needs of North American midstream operators in the oil & gas industry. Through this launch, the company would provide an integrated approach to the supply of material, pipeline life cycle optimization, and engineering of pipeline assets. Honeywell International Inc. (U.S.) is engaged in the supply and manufacturing of products and services in different sectors, such as industrial process control, transportation, oil & gas, refining, petrochemicals, and biofuels, which include pipeline monitoring systems. In 2018, the company made technology-oriented acquisitions with Ortloff Engineers, Ltd. (Texas), which would develop highly proprietary technology to enable maximum separation of gas and gas liquids. Increasing packaging industry leads to a growing demand for Bioplastics & Biopolymers Market4/14/2020  Bioplastics & Biopolymers market size is expected to grow from USD 10.5 billion in 2020 and USD 27.9 billion by 2025, at a CAGR of 21.7%. The major factors driving the bioplastics & biopolymers industry include the focus of governments on green procurement policies and regulations and increasing use of bioplastics in the packaging end-use industry.

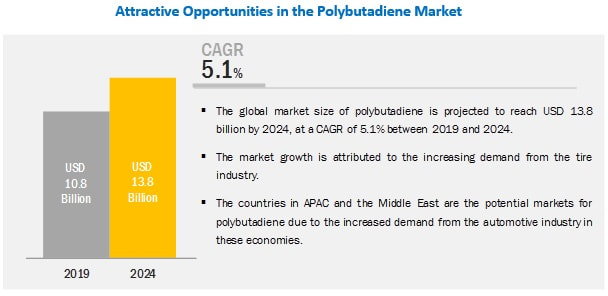

Download PDF Brochure to know More: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=88795240 Packaging is one of the end-use industries that dominate the bioplastics & biopolymers market. Bioplastics, and especially biodegradable bioplastics, have witnessed an increased demand to replace conventional plastics to address environmental concerns. The use of bioplastics is increasing in applications such as bottles, films, clamshell cartons, waste collection bags, carrier bags, mulch films, and food service-ware. APAC is the fastest-growing bioplastics & biopolymers market. APAC is the fastest-growing market for bioplastics & biopolymers, globally. The major end-user industries of bioplastics & biopolymers are packaging, consumer goods, automotive & transportation, and agriculture & horticulture. Industrialization, growing population, and urbanization of APAC are boosting the bioplastics & biopolymers market. The bioplastics & biopolymers market comprises major players such as NatureWorks (Italy), Braskem (Brazil), BASF (Germany), Total Corbion (Netherlands), Novamont (Italy), Biome Bioplastics (UK), Mitsubishi Chemical Holding Corporation (Japan), Biotec (Germany), Toray Industries (Japan), and Plantic Technologies (Australia), Arkema (France), Cardia Bioplastics (Australia), Futerro (Belgium), FKUR Kunstsoff (Germany), Green Dot Bioplastics (US), PTT MCC Biochem (Thailand), Succinity (Germany), Synbra Technology (Netherland), Tianan Biologic Materials (China), and Zhejiang Hisun Biomaterials (China).  The report “Polybutadiene Market by Type (Solid Polybutadiene (High Cis, Low Cis, High Trans, High Vinyl), Liquid Polybutadiene), Application (Tires, Polymer modification, Industrial rubber, Chemical), and Region – Global Forecast to 2024″, The polybutadiene market size is expected to grow from USD 10.8 billion in 2019 to USD 13.8 billion by 2024, at a CAGR of 5.1% during the forecast period. The polybutadiene market is driven by tire, polymer modification, and industrial rubber manufacturing industries. However, the fluctuating raw material prices can hinder the growth of the market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=56692050 Tire application accounts for largest market size during forecast period The tire industry is expanding due to the growing automotive industry. It accounted for the largest share of the overall polybutadiene market. Furthermore, this segment is estimated to grow significantly during the forecast period. Polybutadiene is widely used in tire manufacturing due to its toughness, good abrasion resistance, cold resistance, high tensile strength, high resilience, tear resistance, and durability. Recent Developments In February 2019,SIBUR decided to launch an investment project aimed at enhancing polybutadiene rubber (Nd-BR) production efficiency at its Voronezh facility (Voronezhsintezkauchuk). The project aims for a large-scale upgrade to boost operational efficiency of the existing facility and ensure production of consistently high quality of products. This project will enable SIBUR to produce quality products with improved operational efficiency. ARALNXEO (Netherlands), UBE Industries Ltd (Japan), JSR Corporation (Japan), Kumho Petrochemical Co. Ltd (South Korea), Reliance Industries Ltd. (India), SABIC (Saudi Arabia), LG Chem Ltd (South Korea), Versalis SPA (Italy), PJSC SIBUR Holdings (Russia), Sinopec (China), and Kuraray Co. Ltd (Japan) are some of the major manufacturers of the polybutadiene market. The study includes in-depth competitive analysis of these key players in the polybutadiene market, with their company profiles, recent developments, and key market strategies. To speak to our analyst for a discussion on the above findings, click Speak to Analyst  “Steel Rebar Market by Type (Deformed & Mild), Process (Basic Oxygen Steelmaking & Electric ARC Furnace), End-Use (Housing, Infrastructure, Industrial), Region (North America, EU, APAC, MEA, South America) – Global Forecast to 2025″ The global steel rebar market size is projected to grow from USD 198.7 billion in 2020 to reach USD 246.3 billion by 2025, at a CAGR of 4.4% from 2020 to 2025. The major drivers for the market include the increasing use of higher rebar products, the development of value-added products, capacity expansion by steelmakers all around the world, increasing population, and rapid urbanization. However, the current steel rebar industry is also plagued by the recent outbreak of COVID-19 and its impact on the global economy, which is expected to deter the demand for steel rebar during the forecast period

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=176200687 Recent Developments 1. ArcelorMittal in January 2020, secured a supply contract of rebar for the construction of a new liquefied natural gas (LNG) terminal, located near Kuwait City. 2. In November 2019, Gerdau S.A. agreed to buy 96.4% of Siderúrgica Latino-Americana (Silat) shares from Spanish group Hierros Añón for USD 110.8 million. Silat is located in Caucaia, a city in the northeastern Brazilian state of Ceará, and has a capacity of 600,000 tonnes per year of long rolled steel. The company mainly produces rebar and wire rod. Silat was a close competitor of Gerdau in the rebar market, and with this acquisition, the company has cemented its market position in the rebar market. The Asia Pacific steel rebar market is projected to grow at the highest CAGR between 2020 and 2025. Growth in this market is attributed mainly to the increasing steel rebar consumption in the construction industry coupled with large steelmaking capacities and consumption of steel rebar in countries such as China, India, Japan, and South Korea. Increasing building & construction activities supported by a rapidly growing population, need for new residential housing, and major infrastructure investment projects announced in countries like China is expected to create future market avenues for steel rebar industries. In addition, strong policy initiatives such as the mandatory use of domestic steel in government infrastructural projects, shutting of environmentally hazardous blast furnace capacities and increasing use of electric furnace to produce steel rebar from scrap in China and National Steel Policy introduced in India to make the country self-sufficient in terms of steel production are some of the factors expected to support the growth of the domestic steel rebar market. However, currently, the world is facing a crisis related to the outbreak of coronavirus disease by which the world trade, travel, and even the domestic activities have come to a standstill. This is having a severe impact on the Chinese steel industry, which is home to 60% of the world’s steel rebar production. Major market players covered in the report are ArcelorMittal (Luxembourg), Gerdau S.A (Brazil), Nippon Steel & Sumitomo Metal Corporation (Japan), Posco SS Vina, Co. Ltd (Vietnam), Steel Authority of India Limited (India), Tata Steel Ltd. (India), Essar Steel (India), Mechel PAO (Russia), Nucor Corporation (U.S.), Sohar Steel LLC (Oman), Celsa Steel UK (U.K.), Ansteel Group (China), Hyundai Steel (South Korea), Kobe Steel, Ltd. (Japan), Jiangsu Shagang Group Co., Ltd. (China), JFE Steel Corporation (Japan), Commercial Metals Company (U.S.), Daido Steel (Japan), Barnes Reinforcing Industries (pty) Ltd (South Africa), Jindal Steel & Power Ltd. (India), Steel Dynamics, Inc. (U.S.), Outokumpu Oyj (Finland), Acerinox S.A. (Spain), Hyundai Steel Company (South Korea), Daido Steel Co., Ltd. (Japan), and Byer Steel Group Inc. (U.S.). To speak to our analyst for a discussion on the above findings, click Speak to Analyst |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed