The oxygen-free copper market is projected to grow from USD 19.9 billion in 2020 to USD 25.9 billion by 2025, at a CAGR of 5.3% during the forecast period. Increasing demand for oxygen-free copper from the electronics & electrical end-use industry, especially in the Asia Pacific region, is expected to drive the demand for oxygen-free copper in the near future. The electronics & electrical end-use industry is estimated to account for an 76% share of the oxygen-free copper market, in terms of value, in 2019.

The oxygen-free copper market is dominated by major players such as KGHM Polska Miedz SA (Poland), Hitachi Metals Neomaterials Ltd. (Japan), Zhejiang Libo Holding Group (China), Mitsubishi Materials Corporation (Japan), Metrod Holdings Berhad (Malaysia), Aviva Metals (US), KME Germany GmbH (Germany), and Sam Dong (South Korea). These players have adopted growth strategies, such as acquisitions and expansions to further expand their presence in the global oxygen-free copper market. Aqcuisitions were the most dominating strategy adopted by major players from 2017 to 2020, which helped them to expand their global presence and broaden their customer base. To know about the assumptions considered for the study download the pdf brochure KGHM Polska Miedz SA is a Poland-based company engaged in mining and production of copper and other precious metals. The company operates through various sites under the divisions, such as mining & enrichment, smelting & refining, and downstream processing. Through these divisions, the company manufactures products, such as copper, precious metals, molybdenum, and rhenium. Under the copper product segment, the company provides cathodes, wire rod, Cu- OFE wire, Cu-Ag wire, round billets, and granules. It manufactures oxygen-free copper in Cedynia plant using the UPCAST technology. It exports its products to Germany, the UK, France, China, and the Czech Republic, among other countries. The company has mining and enrichment facilities in Poland, Chile, Canada, and US. Its metallurgy, refinery and processing plants are all located in Poland. The company also has an office located in China to cater to the demands from the region. KGHM is one of the key players among those controlling the world’s copper reserves. The company’s share is estimated at 41.8 million tons (38 million tonnes) of copper in 2020. Neomax Materials Co., Ltd., a predecessor of the company, was founded in 1943 as the Suita branch of Sumitomo Metal Industries, Ltd. Owing to a series of mergers—with Toyo Seihaku Co., Ltd. in October 2015 and Hitachi Metals Nanotech Co., Ltd. in April 2016—the corporate name was changed to Hitachi Metals Neomaterial, Ltd. in 2016. The company also merged with SH Copper Products Co., Ltd. in April 2018. Hitachi Metals Neomaterial, Ltd. has expanded and evolved, integrating the technologies and diverse cultures of each of these companies. It has six production bases and five marketing and sales bases across Japan. The company’s metal materials play a vital role in a wide variety of fields, including home appliances, electronics, automobiles, batteries, and medical equipment. It has an integrated system of production that is one of the most advanced production systems in Japan, covering everything from the melting of metals to rolling, plating, and finish processing, according to customer requests. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=196978298

0 Comments

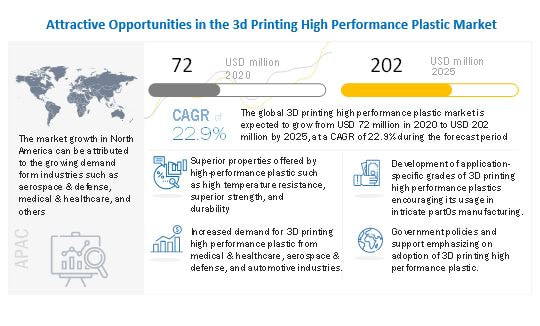

The global 3D printing high performance plastic market is expected to grow from USD 72 million in 2020 to USD 202 million by 2025, at a CAGR of 22.9% during the forecast period. Increasing demand from high end-use industries, growing novel application in tooling and proptotying, and government supportive activities to promote the usage of 3D printing materials is driving the growth of the market.

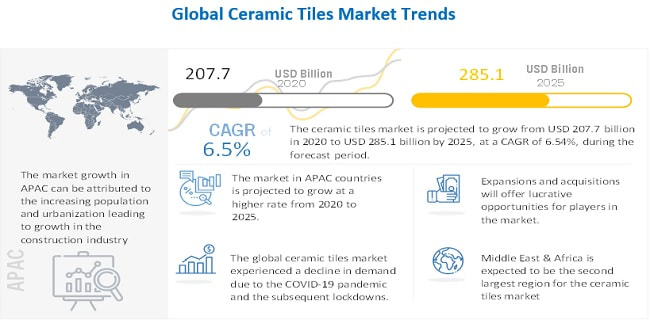

Browse 141 market data Tables and 53 Figures spread through 202 Pages and in-depth TOC on “3D Printing High Performance Plastic Market by Type (PA, PEI, PEEK & PEKK, Reinforced), Form (Filament and Pellet, Powder), Technology (FDM, SLS), Application, End-Use Industry, and Region – Global Forecast to 2025” View detailed Table of Content here – https://www.marketsandmarkets.com/Market-Reports/3d-printing-high-performance-plastic-market-216044197.html Polyamide type comprise a major share in terms of value and volume. Polyamide 3D printing high performance plastic have huge demand from wide end-use industries. Polyamide filaments are useful in several end-use industries ranging from automotive, medical, aerospace, dental, and electrical & electronics. It is available at affordable cost and can be given finishing in multiple ways, including dyed, smoothed spray-printed, and velvet finish making it highly suitable for multiple applications. However, due to pandemic COVID-19, the demand for 3D printing high performance plastic witnessed sharp decline. Factory shutdown, reduced production capacities, and reduced demand from end-use industries has negatively impacted on the growth of the market. This demand would surge with stable economic conditions, uninterrupted supply chain, and growing demand for 3D printing high performance plastic along with innovation of application specific 3D printing material. To know about the assumptions considered for the study download the pdf brochure FDM technology account for the largest market share in the global 3D printing high performance plastic market in terms of value and volume FDM technology is well developed for 3D printing a wide variety of high performance plastics such as PEEK & PEKK, PPSU, and PEI. FDM is the most widely used technology across the world due to its inexpensive nature and excellent compatibility with high performance plastic materials. The technology is highly suitable with high performance plastics in the filament and pellet form and is trusted to produce strong and durable parts with complex geometries. Functional part manufacturing application to grow at the fastest CAGR in the global 3D printing high performance plastic market in terms of value and volume 3D printing high performance plastics used in the Functional part manufacturing application is witnessing high growth across the globe. The superior properties of these plastics such as high-temperature performance, mechanical strength, and excellent chemical resistance are the key factors driving their usage. Various end-use industries, including transportation, healthcare, and aerospace & defense, are early adopters of 3D printing high performance plastics. Medical & healthcare industry dominates the market in the global 3D printing high performance plastic market in terms of value and volume The medical & healthcare industry led the 3D printing high performance plastic market. The industry is continuously looking to adopt breakthrough technologies and materials to cater to the medical requirements of humans. High compatibility of 3D printing high performance plastic such as polyamide has increased its application in making of medical devices, surgical equipment, prosthetics & implants, and tissue engineering products supporting the growth of the market. North America to continue the similar growing trend in the 3D printing high performance plastic market during the forecast period North America held the largest share in 3D printing high performance plastic market and is projected to continue the similar trend over the projected period. Manufacturers of 3D printing materials in North America are putting efforts by undertaking new product launch, collaboration, and other strategies. For instance, in September 2018, Stratasys Ltd. signed a multi-year technical partnership with Team Penske (US). Team Penske will be using advanced materials, such as Carbon Fiber-filled Nylon 12, in additive manufacturing for advanced car testing, production parts, and prototypes. The partnership is aimed at innovating new materials in 3D printing to increase output and improve vehicle performance. Arkema S.A. (France), Royal DSM N.V. (the Netherlands), Stratasys, Ltd. (US), Evonik Industries AG (Germany), 3D Systems Corporation (US), EOS GmbH Electro Optical Systems (Germany), Victrex plc. (UK), Solvay (Belgium), Oxford Performance Materials (US) , and SABIC (Saudi Arabia) are some of the key players in the 3D printing high performance plastic market.. These players have taken different organic and inorganic developmental strategies over the past five years. Don’t miss out on business opportunities in 3D Printing High Performance Plastic Market . Speak to our analyst and gain crucial industry insights that will help your business grow.  The ceramic tiles market is projected to grow from USD 207.7 billion in 2020 to USD 285.1 billion by 2025, at a CAGR of 6.5% during the forecast period. Growth in investments in the construction industry, coupled with a rise in the number of renovation & remodeling activities, further boost the growth of the market for ceramic tiles. The rise in demand from emerging economies and the growth of the organized retail sector create growth opportunities for the market.

The Porcelain segment is projected to dominate the global ceramic tiles market through 2025 The demand for porcelain tiles in recent years has been increasing due to their superior properties, such as low water absorption, slip resistance, and anti-bacterial properties. These properties make porcelain tiles highly popular for kitchens, bathrooms, and hospitals. To know about the assumptions considered for the study download the pdf brochure The flooring segment is projected to grow at the highest CAGR in the ceramic tiles market during the forecast period Ceramic tiles are an ideal and enduring option as a flooring material because of their strength, water-resistance, low maintenance, reliability, and high durability. They find application in healthcare centers, government offices, and sports institutes, where the expected footfall is high, as well as in residential buildings. Being water-resistant and easy to clean, they are the best solution for the kitchen and bathroom floors. The Asia Pacific is projected to hold the largest share in the ceramic tiles market during the forecast period The Asia Pacific is the most attractive market for ceramic tiles due to the rapid socio-economic development in the region. The increasing number of new housing units and huge investments in the infrastructural sector are fueling the demand for ceramic tile materials in this region. The growth of the ceramic tiles market in the APAC region is also driven by increasing demand for ceramic tiles in countries, such as China, India, Thailand, Indonesia, and Vietnam, due to the significant growth in the construction opportunities in these countries. Key players operating in the ceramic tiles market include Mohawk Industries (US), Siam Cement Group (Thailand), Grupo Lamosa (Mexico), RAK Ceramics (UAE), Kajaria Ceramics (India), Grupo Cedasa (Brazil), Ceramica Carmelo Fior (Brazil), Pamesa Ceramica (Spain), Grupo Fragnani (Brazil), and STN Ceramica (Spain). These players have adopted various growth strategies to expand their global presence and increase their market share. Recent Developments

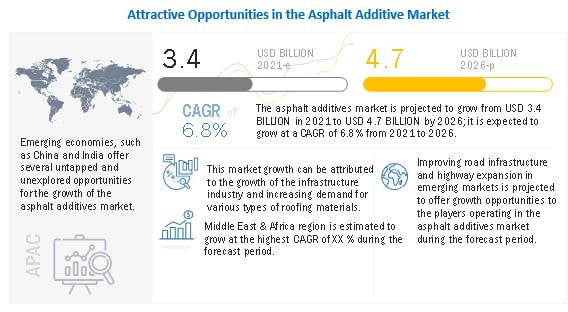

Increased infrastructure spending in China, India, Malaysia, and Indonesia is one of the major factors contributing to the growth of the Asia Pacific asphalt additives market. The increase in government expenditure on infrastructure in the Asia Pacific region can be attributed to the increasing construction of roads and other public infrastructure development projects for improved transportation and enhanced connectivity between important economic centers in these countries.

The Indian government increased its expenditure for the construction of roads and bridges. According to India Brand Equity Foundation, the infrastructure sector has become one of the major focus areas for the Indian government. In the Union Budget 2020-21, the Indian government announced USD 13.14 billion for road and highways construction. Public-private partnerships and foreign investments in road pavement applications are major trends being observed in the economies of the Asia Pacific region, which are expected to drive the road construction market for the next 10 years. To know about the assumptions considered for the study download the pdf brochure Since asphalt additives are used in road pavements, an increase in infrastructure development and road construction projects in the Asia Pacific region are expected to contribute to the growth of the asphalt additives market during the forecast period The asphalt additive market is projected to grow from USD 3.4 billion in 2021 to USD 4.7 billion by 2026, at a CAGR of 6.8%. Roads get damaged due to several factors such as wear & tear, moisture, hot/cold climate, and frost. This damage can be prevented with asphalt additives, as they help increase the durability of pavements by preventing cracking and rutting which leads to an increase in the demand for asphalt additives. Nouryon (Netherlands), DowDuPont (US), Arkema SA (France), Honeywell International Inc. (US), Evonik Industries (Germany), Huntsman Corporation (US), Kraton Corporation (US), Ingevity Corporation(US), and BASF SE (Germany) are some of the leading players operating in the asphalt additive market. These players have adopted the strategies of expansions, new product developments, acquisitions, and collaboration to enhance their position in the market. Recent Developments

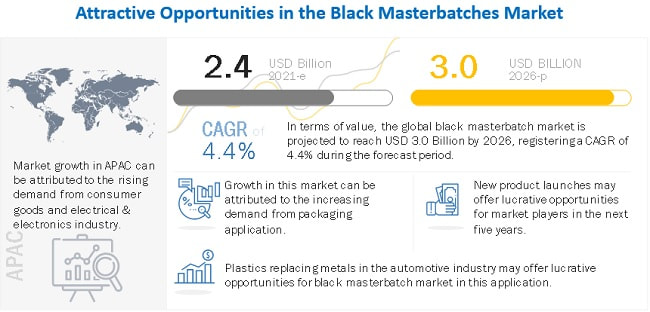

Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=156734514  The black masterbatches market is projected to reach USD 3.0 billion by 2026, at a CAGR of 4.4 % from USD 2.4 billion in 2021.

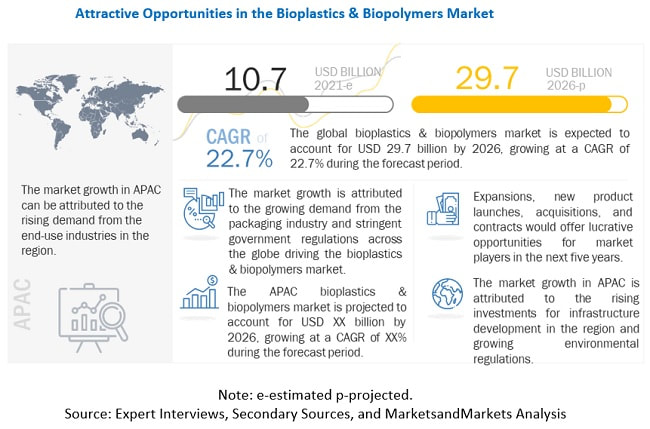

This growth is mainly supported by the increasing need for innovative and attractive plastic products from the packaging industry. Most of the polymer manufacturers have switched the processing method of plastics from compounding to masterbatch. This process is cost-effective and saves processing time as compared to compounded materials. American and European black masterbatch manufacturers are focusing on expanding their manufacturing facilities in emerging economies owing to cost-effective labor, low setup cost, tax benefits, and high demand for black masterbatch. To know about the assumptions considered for the study download the pdf brochure Key players in this market are LyondellBasell (US), Avient Corporation (US), Ampacet Corporation (US), Cabot Corporation (US), Plastika Kritis S.A. (Greece), Plastiblends India Ltd. (India), Hubron International (UK), Tosaf Group (Israel), and Penn Color, Inc. (US). The global and regional players have sizable shares in the black masterbatch market. The key players in the market are focusing on strategies, such as new product launches, partnerships & agreements, acquisitions, and expansions, to expand their businesses globally. Players in the black masterbatches market are mainly concentrating on new product launches, acquisition, and collaboration to meet the growing demand for various end-use industries. New product launches help companies to strengthen their product portfolio and meet the specific demands of customers. The growth of the black masterbatches market has been largely influenced by new product launches that were undertaken between 2016 and 2020. Companies such as Ampacet Corporation and Avient Corporation have adopted new product launches to enhance their market position. PolyOne Corporation, one of the leading manufacturers of specialized polymer materials, acquired Clariant’s masterbatch division in July 2020. The company also changed its name and is now operating as Avient Corporation. In order to strengthen their product portfolio, the company is focusing on organic growth for meeting client’s requirements. The company mainly focused on expansion and new product launch to strengthen its product portfolio. It offers black masterbatch for applications such as packaging, consumer goods, automotive, agriculture, and textile. The company has a strong geographical presence, with operations in five regions, namely, APAC, Europe, North America, South America, and the Middle East & Africa, with more than 50 production plants.In September 2019, the company launched its new black masterbatch colorants—OnColor RC Environmental Black—obtained from the end-of-life tires. This is a sustainable alternative to virgin carbon black. In January 2018, the company expanded its specialty color and additives expertise with the acquisition of a Spanish company named IQAP Masterbatch. Ampacet Corporation is one of the top players in the black masterbatch market. They have a wide range of black masterbatch products. Ampacet black masterbatch has an important role in markets such as agricultural firms and irrigation systems, packaging, electronics, textile, automotive, toys, and construction. The company also offers masterbatches in different segments like color, white, and additive. The company, through its distribution network, sells its products to approximately 90 countries. These products are manufactured at 24 facilities across 17 countries. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=58392794 NatureWorks (US) and Braskem (Brazil) are Leading Players in the Bioplastics & Biopolymers Market2/20/2022  The global bioplastics & biopolymers market size is expected to grow from USD 10.7 billion in 2021 to reach USD 29.7 billion by 2026, at a CAGR of 22.7%.

The increasing demand for bioplastics & biopolymers material in various end-use segments coupled with stringent regulatory and sustainability mandates concerning healthcare safety is driving the market for bioplastics & biopolymers. Additionally, the growing industrial development in the emerging economies, such as APAC and South America along with the rising demand for bioplastics & biopolymers are also driving the market demand. To know about the assumptions considered for the study download the pdf brochure The key players in this market are BASF (Germany), Mitsubishi Chemical Holding Corporation (Japan), NatureWorks (US), Total Corbion (Netherlands), Toray Industries (Japan), Novamont (Italy), Biotec (Germany), Biome Bioplastics (UK), Braskem (Brazil), and Plantic Technologies (Australia). These players have adopted various strategies such as investment & expansion, merger & acquisition, partnership & agreement, and new product launch in order to strengthen their market position. For instance, in April 2021, NatureWorks announced a new strategic partnership with IMA Coffee, which is a market leader in coffee handling processing and packaging. This partnership aims at increasing the market reach for high-performing compostable K-cup in North America. NatureWorks is jointly owned by PTT Global Chemical (Thailand) and Cargill (US). It manufactures biopolymers derived from renewable resources, such as corn, starch, and vegetable oils. It is among the leading advanced material companies and offers a broad portfolio of renewably sourced polymers and chemicals for the packaging and chemical industries. The company offers Ingeo Biopolymer, which is used in 3D printing, beauty and household, building & construction, food & beverage packaging, medical & hygiene, and other applications. It also offers PLA-based biopolymer performance material designed for use in fresh food packaging and food service ware applications. NatureWorks operates in North America, Europe, and APAC, with manufacturing facilities in the US. Braskem was founded in 2002, with the consolidation of six companies, namely, Copene, OPP, Trikem, Proppet, Nitrocarbono, and Polialden. The company operates in the chemical and petrochemical industry and thus, plays an important role in other production chains that are essential to economic development. The company produces polyethylene (PE), polypropylene (PP) and polyvinylchloride (PVC) resins, in addition to basic chemical inputs such as ethylene, propylene, butadiene, benzene, toluene, chlorine, soda, and solvents, among others. The company offers bioplastics through its biopolymers segment. Braskem is the first company that started to produce on a world scale unit BIO- PE which is made out of sugarcane. The company produces 16 million metric tons per year of thermoplastic resins and other chemical products. It exports the products to clients in approximately 100 countries and operates 41 industrial units, which are located in Brazil, the US, Germany, and Mexico as well as 16 regional offices in other countries to provide integrated solutions for clients. the latter in partnership with the Mexican company, Idesa. To know more speak with analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=88795240  Chromatography resins are utilized as stationary matrices with appropriate binding properties in the chromatography column. The different chromatography techniques are IEX, affinity, HIC, SEC, multimodal, and others. IEX and affinity captured the majority shares in the chromatography resin market in 2019. Pharmaceutical & biotechnology (production and academics & research), food & beverage, and water & environmental analysis are the major applications of chromatography resins.

The chromatography resin market size is estimated to be USD 2.2 billion in 2020 and is expected to reach USD 3.3 billion by 2025, at a CAGR of 8.2% during the forecast period. Factors such as increasing demand for therapeutic antibodies, public-private investment in pharmaceutical & life science research, and rising concern for food safety will drive the chromatography resin market. The major restraint for the market will be lack of adequate skilled professionals and presence of alternative technologies to chromatography. However, rise in CROs and CMOs in the pharmaceutical industry, increasing demand for biosimilar, and growing demand for disposable pre-packed columns will act as an opportunity for the market. The demand for chromatography resins is the largest in the pharmaceutical & biotechnology application, driven by the increasing demand for therapeutic monoclonal antibodies. North America is the largest market for chromatography resins. The demand for chromatography is high in the region due to R&D activities, stringent purification standards, and the presence of large research-based biopharmaceutical companies. To know about the assumptions considered for the study download the pdf brochure The key market players profiled in the report include Bio-Rad Laboratories (US), GE Healthcare (US), Merch KGaA (Germany), Thermo Fisher Scientific Inc. (US), Cytiva (US), Tosoh Corporation (Japan), Sartorius Stedim Biotech S.A. (France), Bio-Works Technologies AB (Sweden), Avantor Performance Materials, Inc. (US), Mitsubishi Chemical Corporation (Japan), Purolite Corporation (US), and Repligen Corporation (US). Players in the chromatography resin market are mainly concentrating on new product launches, acquisition, and expansions to meet the growing demand for chromatography resin for various applications. New product launches help companies to strengthen their product portfolio and meet the specific demands of customers. The growth of the chromatography resin market has been largely influenced by new product launches that were undertaken between 2016 and 2020. Companies such as Repligen Corporation, Bio-Rad Laboratories, Inc., Tosoh Corporation, and GE Healthcare have adopted new product launches to enhance their market position. Bio-Rad Laboratories, Inc. is one of the major players in the chromatography resin market. In order to strengthen their product portfolio, the company is focusing launching the new products meeting client’s requirements. For instance, in April 2020, the company announced the commercial launch of its SARS-CoV-2 Total Ab test, a blood-based immunoassay kit to help determine if an individual has developed antibodies to SARS-CoV-2, the virus associated with COVID-19 disease. The test detects IgG, IgM, and IgA antibodies. This approach appears to be more sensitive than assays against a single immunoglobulin. Similarly, in October 2020, Repligen Corporation and Navigo Proteins GmbH announced their successful development of an affinity ligand targeting the spike protein to be utilized in the purification of COVID-19 vaccines. The companies also adopted acquisition as a strategy to increase their share and market presence. For instance,

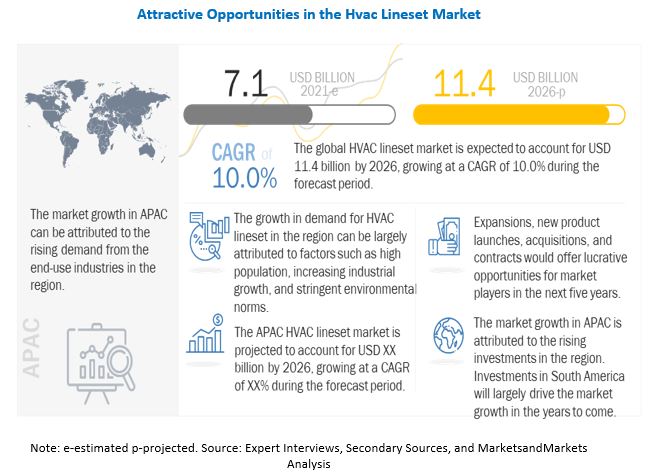

The global HVAC linesets market size is projected to reach USD 11.4 billion by 2026 at a CAGR of 10.0% from USD 7.1 billion in 2021. Urbanization and increase in residential construction, growing trends of smart homes, increasing demand for air conditioners, and significant growth in number of data centers and their power density are driving the HVAC lineset market.

The increase in demand for HVAC systems and the growing industrial development in the emerging economies, such as APAC and South America, are also boosting the market. The key players in the HVAC lineset market include Daikin (Japan), Halcor (Greece), Hydro (Norway), KME SE (Italy), Mueller Streamline Co. (US), Cerro Flow Products LLC (US), JMF Company (US), Zhejiang Ice Loong Environmental Sci-Tech Co., Ltd (China), Feinrohren S.p.A. (Italy), DiversiTech Corporation (US), Foshan Shunde Lecong Hengxin Copper Tube Factory (China), Zhejiang Hailiang Co., Ltd. (China), Linesets Inc. (US), Cambridge-Lee Industries LLC (US), HMAX (US), ICool USA, Inc. (US), PDM US (US), MM Kembla (Australia), Mandev Tubes (India), Uniflow Copper Tubes (India), Kobelco & Materials Copper Tube Co., Ltd. (Japan), Mehta Tubes Limited (India), and Klima Industries (South Korea). These market leaders have adopted various organic as well as inorganic growth strategies between January 2015 and May 2021 to strengthen their position in the HVAC lineset market. The strategy of expansions was among the major growth strategies adopted by the leading market players to enhance their regional presence and meet the growing demand for HVAC lineset in emerging economies To know about the assumptions considered for the study download the pdf brochure Daikin is one of the leading players in air-conditioning and fluorochemicals businesses. It is engaged in manufacturing general air-conditioning equipment with in-house divisions covering both air conditioning and refrigerants. The company operates globally and provides its products in more than 150 countries. The company operates many R&D centers as well that are dedicated to innovations in the Air Conditioning business segments. The R&D centers of the company are located in 6 regions namely: the US, Japan, China, Asia/Oceania, and Europe. The company offers long line sets and Mini Split Line sets under the brand name of Daikin. These line sets are offered through onsite sales or through the channel of e-commerce such as e-Bay. Halcor is amongst the leading manufacturers and suppliers of copper tubes in Europe. The company operates as a copper tubes division of ElvalHalcor, a joint venture established in December 2017, between Elval and Halcor. The copper segment of ElvalHalcor comprises four subsidiaries and two joint ventures, located in Greece, Belgium, Bulgaria, Romania and Turkey. The copper segment of ElvalHalcor develops and distributes a wide range of products, including copper and copper-alloy rolled and extruded products with Halcor being the sole producer of copper tubes in Greece. Halcor along with four more companies form the copper division of ElvalHalcor, is engaged in the production, processing and marketing of copper and copper alloys products. Halcor offers copper alloy and copper based products for application in various sectors, such as plumbing, HVAC&R, renewable energy, architecture, engineering and industrial production. Halcor has a commercial presence across European and global markets with its products being distributed in approximately 60 countries around the world. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=209588791 Increasing industrialization in developing economies drives the Corrosion Inhibitors Market2/15/2022  Infrastructural development in economies such as China, India, Brazil, and South Korea, are expected to boost industrial activities and increase the consumption of corrosion inhibitors during the forecast period. In 2018, countries such as China, the US, Australia, the UK, and France spent 5.57%, 0.52%, 1.69%, 0.92%, and 0.84% of their GDP in construction and maintenance of infrastructure, according to Statista. In 2020, China had scheduled USD 1.07 trillion as infrastructure spending, according to China Banking News.

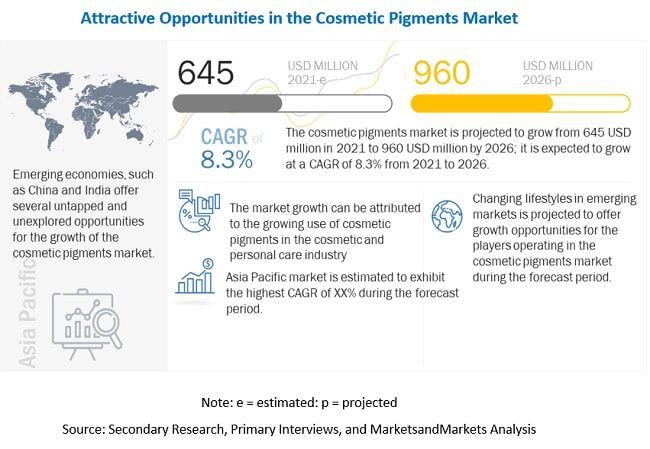

According to the World Bank, emerging economies need to spend about 4.5% of GDP to achieve sustainable development. Infrastructural growth related to electricity demand, clean water demand, fuel demand, transportation demand, and construction demand are expected to boost the market for corrosion inhibitors in the next five years. The global spending on infrastructure is expected to reach USD 94 trillion by 2040, and an additional USD 3.4 trillion would be required to attain United Nations’ Sustainable Development Goals for electricity and water, according to Oxford Economics. Countries in APAC, including China, India, Indonesia, Malaysia, the Philippines, Thailand, and Vietnam, will be the fastest-growing and account for nearly 50% of the global infrastructure spending by 2040, according to an Oxford Economics study. Due to the increasing consumption of industrial water in emerging economies, the opportunity is being created for manufacturers to offer a wide range of corrosion inhibitors to various specific applications in order to protect them from corrosion. To know about the assumptions considered for the study download the pdf brochure The global corrosion inhibitors market size is projected to reach USD 10.1 billion by 2026 at a CAGR of 4.9% from 2021. The increasing demand for corrosion protection chemicals in various end-use segments coupled with stringent regulatory and sustainability mandates concerning the environment is driving the market for corrosion inhibitors. Water Treatment application will account for the major share of the corrosion inhibitor market, based on application in terms of value. Water treatment accounted for 44.4% of the total corrosion inhibitor market in terms of application, in 2020. Corrosion can cause many concerns such as rusting of pipelines, equipment surfaces, and lowered efficiency of the equipment mainly in the industrial sector. Feed water use in various industries contains carbon dioxide which is corrosive to steel. If this carbon dioxide is left untreated, iron deposits on the boilers. These corrosion inhibitors are fed downstream of the deaerating equipment. It is volatilized and carried out with the steam after reacting with carbon dioxide. Corrosion inhibitors for boiler treatment include neutralizing and filming amines for condensate linings. Morpholine, cyclohexylamine, diethylethanolamine (DEAE), aminomethyl propanol, and aqua ammonia octadecylamine (ODA) are some of the common corrosion inhibitors used to protect boiler systems from corrosion. The Middle East & Africa region is the second fastest-growing region for the corrosion inhibitor market, in terms of value. The region has emerging markets, such as Saudi Arabia, the UAE, Iran, Kuwait, and South Africa. The region has established oil & gas and chemical & petrochemical industries due to the abundant availability of natural resources. The oil & gas industry in the region is growing at a steady pace due to rising exports and increased exploration of reserves. Huge investments, rising population, growing disposable income, and integration of production activities are likely to increase output in the form of fuel and feedstock and, in turn, drive the corrosion inhibitors market. Major players operating in the global corrosion inhibitor market include Solenis (US), Nouryon (The Netherlands), Baker Hughes Company (US), Ecolab (US), BASF SE (Germany), SUEZ Water Technologies & Solutions (France), DOW Chemical Company (US), Lubrizol Corporation (US), Lanxess (Germany), and Henkel Corporation (Germany). Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=246  The pandemic is estimated to have an impact on various factors of the value chain of the cosmetic pigments market, which is expected to reflect during the forecast period, especially in the year 2020 to 2021. The various impact of COVID-19 are as follows:

IMPACT ON COSMETIC PIGMENTS: The outbreak of the COVID-19 pandemic has resulted in the temporary shutdown of production plants and related activities in most of the major economies across the globe. Besides, it has slow down the growth of various sectors as most of the countries worldwide have resorted to nationwide lockdown as a measure to control the spread of the virus. This has resulted in disruptions in the global supply chains and consequently affected the growth of the cosmetic industry attributed to the shortage of raw materials and other inputs. Likewise, limited transportation, travel restrictions, and halt of manufacturing activities have hampered the growth of the cosmetic pigments market, and the purchase and usage patterns have changed drastically, which has reduced the sales of various beauty segments. In addition, some of the beauty companies, such as Clarins and Estée Lauder Companies Inc, have switched their manufacturing from beauty products to sanitizers. This has impacted the overall growth of the cosmetic industry, which ultimately has created challenges for the players operating in the cosmetic pigments market. To know about the assumptions considered for the study download the pdf brochure The market size of cosmetic pigments is estimated at USD 645 million in 2021 and is projected to reach USD 960 million by 2026, growing at a CAGR of 8.3%. The global cosmetic pigments market is driven by the growing demand from color cosmetics and personal care applications. Increased need for product differentiation and growing awareness about the improved appearance of products are boosting the market. Asia Pacific is the fastest-growing market, in terms of both production and demand. Higher domestic demand, easy availability of raw materials, and low-cost labor make Asia Pacific the most preferred destination for the manufacturers of cosmetic pigments. The use of cosmetic pigments as an important additive in various applications such as nail products, lip products, eye makeup, facial makeup, hair color products, special effect & special purpose as is driving the market in China. Asia Pacific is emerging as a leading consumer of cosmetic pigments due to the increasing demand from domestic as well as international markets. The key players in the cosmetic pigments market include Sun Chemical (US), Sensient Cosmetic Technologies (France), Merck (Germany), ECKART (UK), Sudarshan (India), Kobo Products (US), Clariant (Switzerland), and Geotech (Netherlands). These players have established a strong foothold in the market by adopting strategies such as expansion, new product launch, and merger & acquisition. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=179525453 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed