Solenis LLC (US) and Baker Hughes (US) are Leading Players in the Corrosion Inhibitors Market6/25/2021  The global corrosion inhibitors market size is projected to reach USD 10.1 billion by 2026 at a CAGR of 4.9% from 2021. The increasing demand for corrosion protection chemicals in various end-use segments coupled with stringent regulatory and sustainability mandates concerning the environment is driving the market for corrosion inhibitors.

The increase in demand for corrosion inhibitors and the growing industrial development in the emerging economies, such as APAC and South America, are driving the market. The key players in the corrosion inhibitors market include Nouryon (Amsterdam), Henkel (Germany), The Lubrizol (US), BASF SE (Germany), Ecolab Inc. (US), Solenis LLC (US), Baker Hughes (US), The Dow Chemical Company (US), and Suez S.A. (France). These market leaders have adopted various organic as well as inorganic growth strategies between January 2016 and March 2021 to strengthen their position in the corrosion inhibitors market. The strategy of acquisition and merger was among the major growth strategies adopted by the leading market players to enhance their regional presence and meet the growing demand for corrosion inhibitors in emerging economies To know about the assumptions considered for the study download the pdf brochure Solenis, formerly known as Ashland Water Technologies, is one of the leading global producers of specialty chemicals for water-intensive industries, including pulp & paper, oil & gas, petroleum refining, chemical processing, mining, biorefining, power, and municipal. The company’s product portfolio includes a broad array of process, functional, and water treatment chemistries, corrosion inhibitors as well as state-of-the-art monitoring and control systems. The company serves its products to various end-use industries, such as biorefining, chemical processing, industrial water, mining & mineral processing, municipal, oil & gas, packaging paper & board, and power generation. The company has focused on the adoption of organic and inorganic strategies to cement its position as the market leader in the corrosion inhibitor market. This includes a merger with BASF SE for paper and wet end water chemicals merged its paper wet-end and water chemicals business The combined business is expected to operate under the Solenis name and offer increased sales, service, and production capabilities across the globe also company has inaugurated a new technology center in Brazil, which will develop new products for various end users. Baker Hughes is an energy technology company with a diversified portfolio of technologies and services that span the energy and industrial value chain. It is one of the leading providers of oilfield services, products, technologies, and systems used in the oil & gas industry. It also provides products and services for other businesses such as downstream chemicals and process and pipeline services. Recently, GE (US) and Baker Hughes Inc. merged their oil and gas equipment and services operations. The company offers corrosion inhibitors in the oilfield services and equipment segment. The company has a strong global presence with a wide product portfolio. The company merged its oil & gas equipment and services operations with GE. The development helped the company to expand its corrosion inhibitors product offerings in the oil & gas industry. Solenis LLC (US), Nouryon (Amsterdam), Baker Hughes (US), BASF SE (Germany), and Ecolab Inc. (US) are the key players in the corrosion inhibitors market. Read More: https://www.marketsandmarkets.com/PressReleases/global-corrosion-inhibitor-market.asp

0 Comments

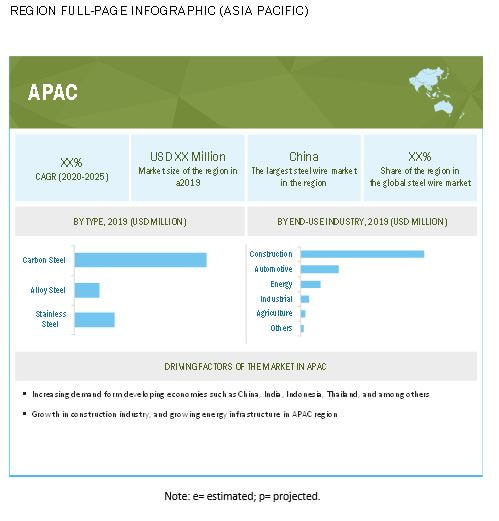

Steel wire are used in a various of end-use industries, including construction, automotive, energy, agriculture, industrial, and others. It possesses high strength, scrub resistance, and good conductivity, which makes it useful in applications such as wire for tires, hoses, galvanized wires and strands, ACSR strands, and armoring of conductor cables, springs, fasteners, clips, staples, mesh, fencing, screws, nails, barbed wires, chains, etc. However, amidst the global COVID-19 pandemic, the demand for steel wires from the industries mentioned above is expected to show a sharp decline. The global steel wire market size is expected to grow from USD 93.2 billion in 2020 to USD 124.7 billion by 2025, projecting a CAGR of 6.0 % during the forecast period between 2020 and 2025.

APAC accounts for the biggest share of the global steel wire market. The construction and automotive end-use industry are major consumers of steel wire in the region. The region is home to some of the major steel wire manufacturers such as Kobe Steel, Tata Steel, and Nippon Steel. Moreover, the China is a manufacturing hub of various commercial, military, and passenger automotive vehicles. Europe is the second major consumer of steel wire construction; automotive and energy are the major industries fueling the growth of the steel wire market in this region. To know about the assumptions considered for the study download the pdf brochure Over the past years, steel wire manufacturers have strengthened their position in the global steel wires market by adopting expansions, partnerships, agreements, new product/technology launches, joint ventures, contracts, and mergers & acquisitions. However, owing to lockdown announced by several countries in 2020, the demand for steel wire from automotive, industrial and energy end-use industries has declined sharply, which resulted in declined demand for steel wire. For instance, as per European Automobile Manufacturers Association the demand for the demand for new cars in Europe is declined by 25% in first quarter of 2020, thereby reducing steel wire demand. The major manufacturers profiled in this report include ArcelorMittal (Luxembourg), Nippon Steel (Japan), JFE Steel Corporation (Japan), TATA Steel Limited (India) and Kobe Steel, Ltd. (Japan), are some of the key players in the steel wire market. JSW Steel Ltd. (India), Bekaert SA (Belgium), The Heico Companies (United States), Ferrier Nord (Italy) and Byelorussian Steel Works (Belarus), and among others. The steel wire business of these companies is severely affected due to the outbreak of COVID – 19 pandemic. Reduced demand for steel wire from several OEMs and disruption in the supply chain have compelled the steel wire manufacturing companies to operate at partial capacities. However, several steel wire manufacturers have focused their concentration on new product development. These developments, coupled with end-use industries resuming their operations at full capacities, would create demand for steel wires during the forecast period. For instance, Bekaert SA reached to and acquisition agreement with Bridon-Bekaert Ropes Group and took full ownership. The company adopted this strategy to grow their business globally and to create significant value over the period of time. Read more: https://www.marketsandmarkets.com/PressReleases/steel-wire.asp Increasing awareness, changing regulations, and rising emphasis on safety measures across the globe6/17/2021  The increasing number of fire accidents, which result in injuries, loss of life, and damage to property, has led to the implementation of various codes, regulations, and standards for fire safety and fire protection. In this regard, Europe and North America have the highest number of safety codes and regulations as compared to other regions.

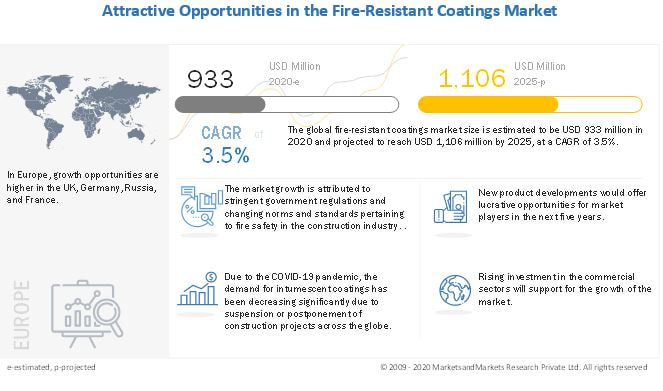

The implementation of stringent regulations and norms is driving the demand for fire-resistant coatings, as newly constructed buildings and processing plants need to meet the required safety and fire resistance standards. Considering the growth opportunities, market players are focusing on developing new and innovative products that comply with the stringent safety and fire protection standards. Thus, as a preventive measure, governments, builders, and construction industries are using fire-resistant coatings to ensure the utmost safety at housing, commercial, institutional, and industrial places. These factors are thereby supporting market growth. The fire-resistant coatings market was USD 933 million in 2020 and is projected to reach USD 1,106 million by 2025, at a CAGR of 3.5% from 2020. Increasing awareness and emphasis on safety measures and preference for lightweight materials, which require additional protection, are expected to drive the market. Increasing urbanization and the growing building & construction industry are expected to provide growth opportunities in the market during the forecast period. The use of low-cost cementitious coatings in developing countries and in dry environments is expected to support market growth. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=95861153 Europe accounted for the largest share of the global fire-resistant coatings market in 2019. The growth of the fire-resistant coatings market in this region is mainly attributed to stringent government regulations, an industrial initiative for sustainable development, and a strong emphasis on protection against fire. Moreover, the practice of constructing green buildings and adopting green coatings offers many opportunities for the growth of the market in the region. The European market is mainly dominated by the EU-5 countries, especially Germany and the UK. The leading players in the fire-resistant coatings market include AkzoNobel (Netherlands), PPG (US), Jotun (Norway), Sherwin-Williams (US), and Hempel (Denmark). The key industry players are adopting strategies to expand their presence and enhance their product portfolio through investments in R&D. For example, in 2017, Hempel invested in an R&D center solely for fire-resistant coatings in Spain. This expansion will help the company comply with the ever-changing demand from the construction industry and develop high efficacy products. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=95861153  Increased infrastructure spending in China, India, Malaysia, and Indonesia is one of the major factors contributing to the growth of the Asia Pacific asphalt additives market. The increase in government expenditure on infrastructure in the Asia Pacific region can be attributed to the increasing construction of roads and other public infrastructure development projects for improved transportation and enhanced connectivity between important economic centers in these countries.

The Indian government increased its expenditure for the construction of roads and bridges. According to India Brand Equity Foundation, the infrastructure sector has become one of the major focus areas for the Indian government. In the Union Budget 2020-21, the Indian government announced USD 13.14 billion for road and highways construction. Public-private partnerships and foreign investments in road pavement applications are major trends being observed in the economies of the Asia Pacific region, which are expected to drive the road construction market for the next 10 years. To know about the assumptions considered for the study download the pdf brochure Since asphalt additives are used in road pavements, an increase in infrastructure development and road construction projects in the Asia Pacific region are expected to contribute to the growth of the asphalt additives market during the forecast period. The asphalt additive market is projected to grow from USD 3.4 billion in 2021 to USD 4.7 billion by 2026, at a CAGR of 6.8% from 2021 to 2026. Increase in road construction projects along with the growing usage of asphalt additives in roofing application are some of the major key factors driving the growth of the asphalt additive market across the globe. Nouryon (Netherlands), DowDuPont (US), Arkema SA (France), Honeywell International Inc. (US), Evonik Industries (Germany), Huntsman Corporation (US), Kraton Corporation (US), Ingevity Corporation (US), and BASF SE (Germany) are some of the leading players operating in the asphalt additive market. These players have adopted the strategies of expansions, new product developments, acquisitions, and collaborations to enhance their position in the market. Read More: https://www.marketsandmarkets.com/PressReleases/asphalt-additive.asp  Plastics are used in mulch films, greenhouse film covers, shades, netting, and silage strap wrap in the agricultural sector. The plastics used in the agriculture sector provide high light transmission to promote the growth of plants. Agricultural plastics need to be able to withstand high solar radiation and mechanical stress. Therefore, antioxidants are used to provide processing and thermal stability and discoloration resistance to agricultural plastics. Countries such as India have not explored the benefits of plastics in the agricultural industry. According to the Federation of Indian Chambers of Commerce & Industry, in 2013, the global average demand for plastics in the agricultural industry was 8%, and in India, it was 2%. Thus, there is a strong growth opportunity for stakeholders in the plastic antioxidants market in India.

The plastic antioxidants market is projected to reach USD 2.6 billion by 2025, at a CAGR of 5.3% from USD 2.0 billion in 2020. Factors such as plastics replacing conventional materials, increasing demand in medical industry, and rapid urbanization in developing countries will drive the plastic antioxidants market. The major restraint for the market will be adverse effect on health from synthetic plastics antioxidants. However, the untapped demand in the agricultural sector of developing countries will act as an opportunity for the market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=106598592 Antioxidants are stabilizing agents that inhibit the process of oxidation by reacting and decomposing the reactive species. They protect plastics and other materials against thermally induced oxidation. Antioxidants that are used in plastics include primary antioxidants and secondary antioxidants. Different types of antioxidants provide different levels of reactivity as a function of temperature and also react and decompose the different radical intermediates in the oxidation process, thereby providing thermal stability to plastics. PP is the largest polymer resin segment of the plastic antioxidants market. Asia Pacific was the largest market for plastic antioxidants in 2019, in terms of both volume and value. Factors such as plastics replacing conventional materials, increasing demand in medical industry, and rapid urbanization in developing countries will drive the plastic antioxidants market. APAC projected to be fastest growing region for the plastic antioxidants market. The region is characterized by a growing population and economic developments. The increasing population in the region, accompanied by increasing construction spending in the developing markets of China, India, and Indonesia, is projected to make this region an ideal destination for the plastic industry. This, in turn, is expected to drive the plastic antioxidants industry in the near future. The increase in employment rate, the rise in disposable income of the people, and an increase in foreign investments in various industries of the economy are some of the other factors that make APAC an attractive market for plastic antioxidants manufacturers. Don’t miss out on business opportunities in Plastic Antioxidants Market. Speak to our analyst and gain crucial industry insights that will help your business grow. Several harmful chemicals are still being used as ingredients in makeup products. These chemicals may have an adverse effect on human health and can increase the risks of health hazards when several makeup products are used together. A combination of increased public interest and market trends in the cosmetics industry has led cosmetics manufacturers to seek more natural and sustainable cosmetic emulsifiers. The demand for organic pigments, which are environment-friendly and are manufactured using sustainable technologies, is increasing rapidly. Manufacturing companies are investing to venture into the green market and are following sustainable technologies. The growing demand for cosmetic pigments that are manufactured using natural ingredients and organically produced from renewable raw materials is proving an opportunity for the cosmetic pigments market players.

The market size of cosmetic pigments is estimated at USD 645 million in 2021 and is projected to reach USD 960 million by 2026, growing at a CAGR of 8.3%. The global cosmetic pigments market is driven by the growing demand from color cosmetics and personal care applications. Increased need for product differentiation and growing awareness about the improved appearance of products are boosting the market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=179525453 Recent Developments:

Asia Pacific is the fastest-growing market, in terms of both production and demand. Higher domestic demand, easy availability of raw materials, and low-cost labor make Asia Pacific the most preferred destination for the manufacturers of cosmetic pigments. The use of cosmetic pigments as an important additive in various applications such as nail products, lip products, eye makeup, facial makeup, hair color products, special effect & special purpose as is driving the market in China. Asia Pacific is emerging as a leading consumer of cosmetic pigments due to the increasing demand from domestic as well as international markets. The key players in the cosmetic pigments market include Sun Chemical (US), Sensient Cosmetic Technologies (France), Merck (Germany), ECKART (UK), Sudarshan (India), Kobo Products (US), Clariant (Switzerland), and Geotech (Netherlands). These players have established a strong foothold in the market by adopting strategies such as expansion, new product launch, and merger & acquisition. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=179525453  The demand for reinforced 3D printing high performance plastics is increasing for functional part manufacturing. These grades offer optimum performance in extreme conditions such as corrosive and high temperature/pressure environments. Carbon fibers and glass fibers are added to PEEK, PEKK, and polyamide to enhance their performance. Novamid ID1030 CF10, offered by Royal DSM, is a 3D printing grade high-quality polyamide that is 10% carbon-reinforced. Novamid finds a variety of applications ranging from automotive to packaging. Another manufacturer from the US, Stratasys, Ltd., provides FDM Nylon 12 CF, which is polyamide (PA)12 thermoplastic filament reinforced with chopped carbon fiber 35% by weight. The material has the highest flexural strength of any thermoplastic, leading to the highest stiffness-to-weight ratio. The combination of lightweight and high strength and stiffness makes it an ideal replacement for heavier metal components in applications such as functional prototypes and selective end-use parts.

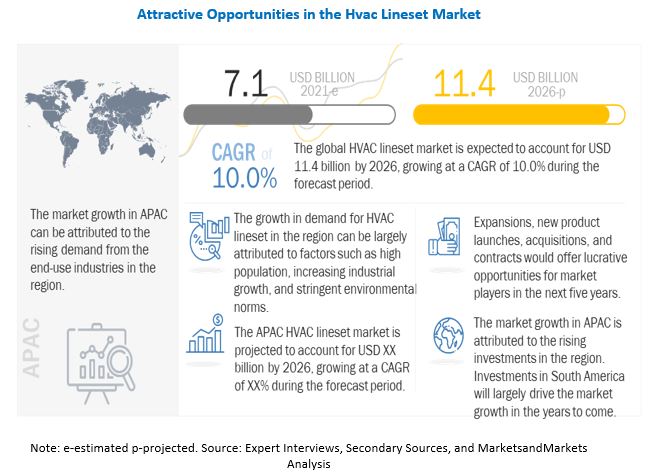

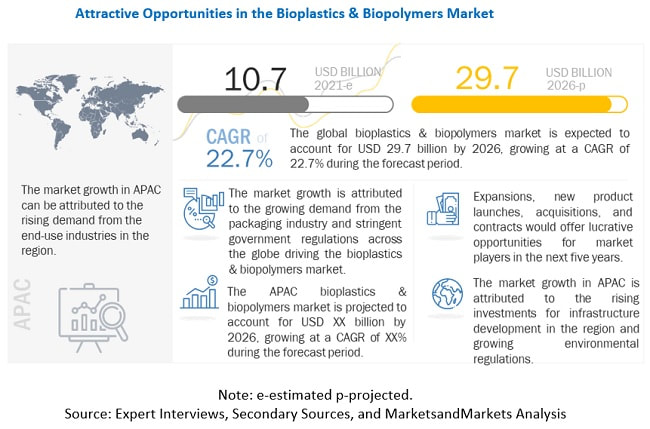

Download pdf brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=216044197 The global 3D printing high performance plastic market is expected to grow from USD 72 million in 2020 to USD 202 million by 2025, at a CAGR of 22.9% during the forecast period. Increasing demand from high end-use industries, growing novel application in tooling and proptotying, and government supportive activities to promote the usage of 3D printing materials is driving the growth of the market. North America to continue the similar growing trend in the market North America held the largest share in 3D printing high performance plastic market and is projected to continue the similar trend over the projected period. Manufacturers of 3D printing materials in North America are putting efforts by undertaking new product launch, collaboration, and other strategies. For instance, in September 2018, Stratasys Ltd. signed a multi-year technical partnership with Team Penske (US). Team Penske will be using advanced materials, such as Carbon Fiber-filled Nylon 12, in additive manufacturing for advanced car testing, production parts, and prototypes. The partnership is aimed at innovating new materials in 3D printing to increase output and improve vehicle performance. Arkema S.A. (France), Royal DSM N.V. (the Netherlands), Stratasys, Ltd. (US), Evonik Industries AG (Germany), 3D Systems Corporation (US), EOS GmbH Electro Optical Systems (Germany), Victrex plc. (UK), Solvay (Belgium), Oxford Performance Materials (US) , and SABIC (Saudi Arabia) are some of the key players in the 3D printing high performance plastic market.. These players have taken different organic and inorganic developmental strategies over the past five years. Don’t miss out on business opportunities in 3D Printing High Performance Plastic Market . Speak to our analyst and gain crucial industry insights that will help your business grow.  The Paris Agreement aims to limit global warming to well below 2°C above pre-industrial levels and ideally to no more than 1.5°C. However, a lack of ambitious policies to curb emissions among large emitters indicates a likely temperature increase of more than 3°C by 2100 and up to 4.8°C under the worst-case scenarios. Due to this, the number of hot days is projected to increase globally, resulting in a rise in demand for cooling solutions. The Intergovernmental Panel on Climate Change (IPCC) predicts that global energy demand from residential AC will grow 33-fold between 2000 to 2100, mostly from developing countries. Furthermore, populous cities in already hot regions could see temperature shifts of multiple degrees. For instance, Ahmedabad in India, which is trying to save lives by implementing a Heat Action Plan, will see an increase of 1.6°C. Additionally, demand for cooling solutions is likely to grow in more temperate climates. The colder regions could be more detrimentally affected by rising temperatures than hotter regions because they have not traditionally prepared for hot days and heatwaves. In order to cope with high summer temperatures, buildings have traditionally relied on ventilation. which is less effective during heatwaves. With heatwaves becoming more prevalent in the UK and the rest of Europe, the demand for cooling is likely to grow. Moreover, cities raise temperatures by trapping heat and preventing its dissipation into the lower atmosphere. They also produce their own heat, such as warm pollutants ejected from vehicle fumes and industrial activities, which become concentrated, confined by buildings and urban structures. This results in microclimates called the urban heat islands (UHI). The UHI in a city with more than one million population can result in temperatures between 1-3°C warmer than its surrounding areas. Developed cities with UHI dynamics include London, Paris, New York, and Las Vegas. Low-and middle-income countries suffer acutely due to UHIs. These factors create growth opportunities for HVAC line sets manufacturers. The global HVAC linesets market size is projected to reach USD 11.4 billion by 2026 at a CAGR of 10.0% from USD 7.1 billion in 2021. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=209588791 Browse 186 market data Tables and 67 Figures spread through 231 Pages and in-depth TOC on “HVAC Linesets Market” Major players operating in the global HVAC linesets market include Daikin (Japan), Halcor (Greece), Hydro (Norway), KME SE (Italy), Mueller Streamline Co. (US), Cerro Flow Products LLC (US), JMF Company (US), Zhejiang Ice Loong Environmental Sci-Tech Co., Ltd (China), Feinrohren S.p.A. (Italy), DiversiTech Corporation (US), Foshan Shunde Lecong Hengxin Copper Tube Factory (China), Zhejiang Hailiang Co., Ltd. (China), Linesets Inc. (US), Cambridge-Lee Industries LLC (US), HMAX (US), ICool USA, Inc. (US), PDM US (US), MM Kembla (Australia), Mandev Tubes (India), Uniflow Copper Tubes (India), Kobelco & Materials Copper Tube Co., Ltd. (Japan), Mehta Tubes Limited (India), and Klima Industries (South Korea).  The global bioplastics & biopolymers market size is expected to grow from USD 10.7 billion in 2021 to USD 29.7 billion by 2026, at a CAGR of 22.7% between 2021 and 2026. Bioplastics are plastics derived from renewable sources such as corn, potatoes, rice, soy, sugarcane, wheat, and vegetable oil, while biopolymers are naturally occurring polymers. A bioplastic may or may not be biodegradable. Bioplastics are mainly segmented into biodegradable and non-biodegradable plastics for various applications in the packaging, consumer goods, automotive & transportation, agriculture & horticulture, medical, and other end-use industries.

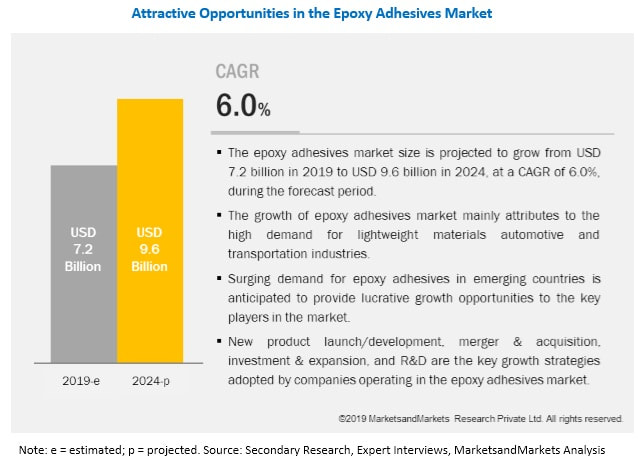

The Report is backed adequately with the reasoning, approaches, and sources Downlow PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=88795240 Consumer awareness regarding sustainable plastic solutions and pervasive efforts to eliminate the use of non-biodegradable conventional plastics are contributing to the market growth of bioplastics. Traditional plastics, which are generally petroleum-based, take decades to break down or degrade and lay in the landfills for a long period. Biodegradable plastics break down faster when they are discarded and are absorbed back into the natural system. In addition, the rate of decomposition of biodegradable plastics by the activities of microorganisms is much faster than that of traditional plastics. Biodegradable plastics break down 60% and more within 180 days or less as compared with traditional plastics, which take around 1,000 years to break down. Increasing landfills and waste piles have emerged as serious environmental hazards and resulted in numerous adverse effects on flora and fauna of the ecosystem. The growing consumer awareness regarding these adverse effects (arising from the use of traditional plastics) is encouraging the use of biodegradable plastics. Moreover, the use of conventional polymers may pose a threat to human health and safety due to their toxic content. For example, PVC may cause genetic disorders, ulcers, deafness, and vision failure. The table below lists the risks associated with the use of conventional polymers/plastics. Such high risks increase the demand for products that are safe for human health. Therefore, increasing consumer awareness, along with governmental legislation, is driving the use of bio-based products such as biodegradable plastics and bio-based plastics. APAC is estimated to be the fastest-growing market for bioplastics & biopolymers between 2021 and 2026. Growth in APAC is primarily attributed to the fast-paced expansion of the economies such as China, India, and Indonesia. Growing population increased consumer spending, and rapid industrial expansion are the major factors responsible for the high growth rate of the region. Growing environmental concern and awareness along with increasing regulations are the key factors driving the demand for bioplastics & biopolymers. The manufacturers focus on the high-growth market to gain market share and increase their profitability. The key players in this market are NatureWorks (US), Braskem (Brazil), BASF (Germany), Total Corbion (Netherlands), Novamont (Italy), Biome Bioplastics (UK), Mitsubishi Chemical Holding Corporation (Japan), Biotec (Germany), Toray Industries (Japan), and Plantic Technologies (Australia). Don’t miss out on business opportunities in Bioplastics & Biopolymers Market. Speak to our analyst and gain crucial industry insights that will help your business grow. Henkel AG (Germany) and Sika AG (Switzerland) are the Kay Players in the Epoxy Adhesives Market6/2/2021  The global epoxy adhesives market size is projected to grow from USD 7.2 billion in 2019 to USD 9.6 billion by 2024, at a CAGR of 6.0% between 2019 and 2024. Increasing urbanization growing usage of composites, plastics, and other higher strength metals in the construction industry are driving the global epoxy adhesives market. Epoxy adhesives are used in various applications due totheir exceptional bonding and mechanical & electrical insulating properties and resistance to chemicals andheat.

The key epoxy adhesive market players are Henkel AG (Germany), Sika AG (Switzerland), 3M Company (US), H.B. Fuller (US), DuPont (US), Illinois Tool Works Incorporation (US), Ashland (US), RPM International (US), Lord Corporation (US), Huntsman Corporation (US), Mapie S.p.A. (Italy), Panacol-Elosol GmBH (Germany), Permabond LLC. (UK), Delo Industrie Klebstoffe GmBH & Co. KGAA (Germany), Masterbond Inc. (US), Weicon GmBH & Co. KG (Germany), Hernon Manufacturing Inc. (US), Hubei Huitian New Materials Co. Ltd. (China), Parson Adhesives Inc. (US), and Uniseal Inc. (US). These players have adopted growth strategies, such as new product development, merger & acquisition, and investment & expansion, to expand their geographical presence and broaden their product portfolio. To know about the assumptions considered for the study download the pdf brochure Henkel AG (Germany) is one of the leading solution providers for adhesives, sealants, and functional coatings. The company has three business segments, namely, adhesive technologies, laundry & home care, and beauty care. The company manufactures epoxy adhesives under its adhesive technologies segment. Henkel offers a multitude of products to cater to the needs of different target groups: consumers, craftsmen, and industrial businesses. Henkel Adhesive Technologies is a global leader in adhesives, sealants, and functional coatings, worldwide. The complete solution of the company is organized into five technology cluster brands-LOCTITE, BONDERITE, TECHNOMELT, TEROSON, and AQUENCE. It has a strong network for distributing and manufacturing adhesives with 185 production sites in 56 countries to meet the changing demands of the market. The company continuously focuses on its organic & inorganic growth.

|

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed