Economizers are mechanical devices that are used to make machines energy efficient by lowering their energy consumption. Economizers, owing to their exceptional characteristic of energy conservation and fuel saving, are been widely used in industrial boilers. Schneider Electric SE (France), Johnson Controls International plc (US), Alfa Laval AB (Sweden), Babcock & Wilcox Enterprises, Inc., (US), Honeywell International Inc. (US), Thermax Limited (India), Cleaver-Brooks, Inc. (US), SAACKE GmbH (Germany), SECESPOL Sp. z o.o. (Poland), STULZ Air Technology Systems, Inc. (US), Kelvion Holding GmbH (Germany), BELIMO Holding AG (Switzerland), Cain Industries (US), Sofame Technologies Inc. (Canada), Cannon Boiler Works (US), Shandong Hengtao Group (China), and MicroMetl Corporation (US) are key players operating in the economizer market.

Economizer Market was valued at USD 7.70 Billion in 2016 and projected to reach USD 11.54 Billion by 2022, at a CAGR of 6.7% from 2017 to 2022. Among end-use industries, the industrial segment is projected to lead the economizer market from 2017 to 2022. The power plants application segment is expected to lead the economizer market. The Asia Pacific economizer market is projected to grow at the highest CAGR during the forecast period. The demand for economizers is expected to increase during the forecast period due to their increased used in various applications such as power plants, boilers, heating, ventilation, and air conditioning (HVAC), etc. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=168759156 Economizers in power plants are used as heat exchanger devices, which conserve the residual heat generated by boilers. The growing demand for electricity has led to the installation of new fossil fuel-based thermal power plants in various regions worldwide, which, in turn, is anticipated to drive the demand for economizers, globally. China, Japan, India, South Korea, Indonesia, and Australia are key countries considered for market analysis in this region. Increasing investments in the development of new power plants and upgrade of existing power plants as well as rising government initiatives for harnessing renewable and clean energy in various countries, such as China and India, are major factors driving the growth of the Asia Pacific economizer market. Acquisitions, contracts, expansions, and collaborations are major growth strategies adopted by leading companies in the economizer market. These companies are also investing in R&D activities to strengthen their product portfolio and enhance their presence in the economizer market. Schneider Electric SE is a global specialist in energy management and automation solutions. The company was founded in 1836 and is headquartered in Rueil-Malmaison (France). It operates through 4 business segments, namely, building, industry, infrastructure, and information technology. Schneider Electric SE offers energy saving products under its critical power, cooling, and racks segment. The company focuses on sustainable development and has a broad product portfolio, along with a wide industry coverage. The company focuses on the adoption of both, organic and inorganic growth strategies to expand its geographic reach in the economizer market. For instance, in October 2016, Schneider Electric SE and Panasonic Corporation (Japan) jointly developed HVAC equipment and building management solutions to reduce energy consumption in various applications. Read More: https://www.marketsandmarkets.com/PressReleases/economizer.asp

0 Comments

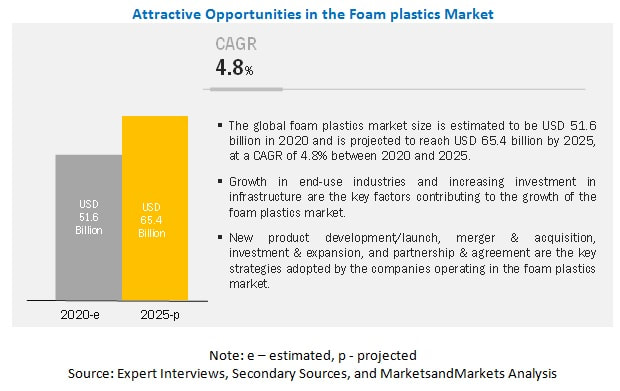

Foam plastics are resins used in manufacturing polymer foams, which are used in various end-use industries such as building & construction, furniture & bedding, packaging, and automotive among others. The market size for Foam plastics is projected to grow from USD 51.6 billion in 2020 to USD 65.4 billion by 2025, at a CAGR of 4.8%. Foam plastics are largely used in building & construction, packaging, and furniture & bedding. The polyurethane segment is estimated to account for the largest share of the overall market due to its properties such as low heat conduction coefficient, low density, low water absorption, relatively good mechanical strength, and good insulating properties.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=260352983 Building & construction segment accounted for the largest share of the foam plastics market in 2019 Foam plastics are used to make foams used in the building & construction industry for forging, doors, roof board, and slabs. PU is the dominant resin used in the building & construction industry for insulation. It has low heat conduction coefficient, low density, low water absorption, and relatively good mechanical strength and insulating properties, which are helpful in the building & construction sector. The COVID-19 pandemic has affected various end-use industries, and almost all divisions of the supply chain continue to be affected, which also includes the construction industry. According to the National Association of Home Builders (NAHB), US, the GDP growth rate during the first two quarters is expected to be negative. This decline can be compared to the aftermath of the global performance of the 2008 Great Recession. However, the fourth quarter of 2020 is expected to be a rebound period. Recent Developments In March 2019, BASF enhanced its regional innovation capabilities with new facilities at the Innovation Campus Shanghai to further strengthen collaboration with the automotive industry and to offer new process catalysts to the chemical industry. With an investment of approximately USD 38.0 million, the new 5,000-square-meter facility includes the Automotive Application Center and the Process Catalysis Research & Development (R&D) Center. One of the innovations includes polyurethane (PU) integral foam solutions with an open cell structure offering unique performance, which are light-weight and have excellent sound insulation and flame resistance. APAC is the leading market for foam plastics. The growth in the region is fueled by the booming economies of China, India, Indonesia, and Vietnam. PU resin based foams are preferred choice in the building & construction industry in APAC. It is in high demand, as it is a low-cost material that provides low heat conduction coefficient, low density, low water absorption, relatively good mechanical strength, and good insulating properties. APAC is a rapidly developing region with growth opportunities for companies willing to invest in high-growth markets. The key players profiled in the foam plastics market report are BASF SE (Germany), Covestro (Germany), Huntsman International LLC (US), The Dow Chemical Company (US), and Wanhua Chemical Group Co., Ltd. (China). Read More: https://www.marketsandmarkets.com/PressReleases/foam-plastics.asp The Asia Pacific region is the largest market for thermally conductive grease across the globe6/21/2020  The Asia Pacific region led the thermally conductive grease market, in terms of both value as well as volume. The growth of the Asia Pacific thermally conductive grease market is due to the increased use of thermally conductive grease by different end-use industries in China, India, Japan, South Korea, and Rest of Asia Pacific. Improving economic condition in the region have led to an increased demand for automobiles, thereby fueling the growth of the thermally conductive grease market in the region. Moreover, the continuously increasing population of the region is also contributing towards increased demand for consumer products, which, in turn, is leading to the growth of the Asia Pacific thermally conductive grease market.

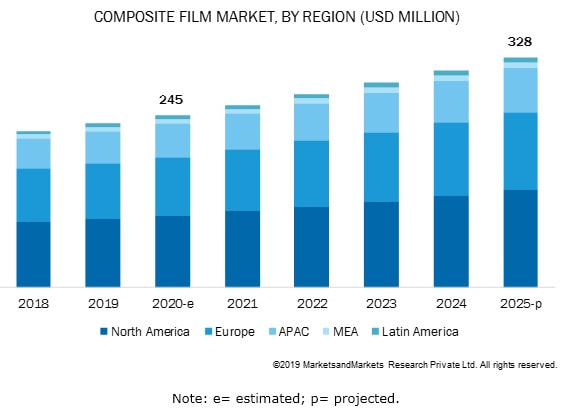

The thermally conductive grease market was valued at USD 273.0 Million in 2016 and is projected to reach USD 416.6 Million by 2022, at a CAGR of 7.3%. The growth of the thermally conductive grease market across the globe is fueled by the increased demand from the LED lighting industry in indoor and outdoor applications. There is an increasing demand for thermally conductive grease in Asia Pacific, Europe, North America, and South America. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=216193458 The LED lighting end-use industry is projected to lead the thermally conductive grease market during the forecast period, owing to the increased demand for thermally conductive grease from the indoor and outdoor LED lighting applications across the globe. The increased government initiatives to ban CFL and improve energy efficient lighting systems in various regions are expected to drive the market of LED lighting. This, in turn, is expected to drive the demand for thermally conductive grease during the forecast period. New product launches, expansions, and mergers & acquisitions are the key growth strategies undertaken by the market players to maintain and enhance their position in the thermally conductive grease market. The growth of the thermally conductive grease market can be attributed to the increased demand from the electronics & electrical industry. Leading players in this market are also focusing on partnerships to increase their market shares. Major manufacturers of thermally conductive grease, including Dow Corning Corporation (US), Electrolube (UK), Laird PLC. (UK), Momentive Performance Materials Inc. (US), 3M Company (US), Parker-Hannifin Corporation (US), LORD Corporation (US), Wacker Chemie AG (Germany), and Henkel AG & Co. KGaA (Germany) have been profiled in this report on the thermally conductive grease market. These companies adopted both organic and inorganic growth strategies to strengthen their position in the thermally conductive grease market. Electrolube is the most active player in the thermally conductive grease market. It develops various types of thermally conductive greases to cater to the varied requirements of different end-use industries. The company has adopted the strategies of agreements, expansions, and new product launches to enhance its position in the market. As a part of its strategy, in July 2016, Electrolube expanded its reach to India by establishing a new manufacturing plant to produce encapsulation resins, conformal coatings, and thermal management materials. Read More: https://www.marketsandmarkets.com/PressReleases/thermally-conductive-grease.asp  Composite films are used in a variety of end-use industries, including aerospace & defense, and automotive, among others. Led by strong end-user demand, the composite film industry is growing at a rapid pace. The global composite film market size is expected to grow from USD 245 million in 2020 to USD 328 million by 2025, at a Compound Annual Growth Rate (CAGR) of 6.0% during the forecast period.

Over the past few years, companies have strengthened their position in the global composite film market by adopting strategies such as expansions, contracts, agreements, new product launches, and acquisitions. From 2015 to 2020, expansions and contracts have been the key strategies adopted by market players to maintain growth in the global composite film market. For instance, in July 2018, Solvay signed a contract with Airbus to supply advanced materials such as prepregs, resin systems, adhesives, and surfacing films, carbon fiber, textiles, tooling, etc. till 2025. To know about the assumptions considered for the study download the pdf brochure Major manufacturers profiled in this report include 3M(US), Henkel AG Co. KGaA(Germany), Hexcel Corporation(US), Gurit (Switzerland), Solvay(Belgium), Toray Industries, Inc. (Japan), Socomore(France), Park Aerospace Corp.(US), Axiom Materials Inc.(US), among others. These companies adopted various organic and inorganic growth strategies. For instance, in March 2018, Toray acquired TenCate Advanced Composites to accelerate the growth of advanced composites for both companies. This acquisition increased the demand for composite films and thus helped Toray sustain in the composite film market. 3M (US), Henkel AG Co. KGaA(Germany), Hexcel Corporation(US), Gurit (Switzerland), Solvay(Belgium) are major players in the composite film market. These companies are the largest growth contributors of the global composite film industry. These companies specialize in manufacturing composite films that have sustainable properties. For instance, Hexcel Corporation (US) specializes in manufacturing composite films, namely HexBond, for the composite film industry, globally. Similarly, Solvay (Belgium) specializes in the manufacture of composite films for the composite film industry, globally. These companies are the key players present in the global composite film market and have a vast global presence. Read More: https://www.marketsandmarkets.com/PressReleases/composite-film.asp Polymer modified cementitious coatings are widely used in residential buildings application6/18/2020  The polymer modified cementitious coatings market is estimated to be USD 1.23 Billion in 2017 and is projected to reach USD 1.66 Billion by 2022, at a CAGR of 6.2%. The growth of this market can be attributed to the increasing demand for polymer modified cementitious coatings from the residential buildings sector. In addition, government initiatives to support infrastructural developments in the Asia Pacific region are anticipated to drive the growth of the polymer modified cementitious coatings market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=251464560 The growth of the residential buildings segment can be attributed to the increasing use of polymer modified cementitious coatings in various residential applications, such as exterior walls, driveways & sidewalks, and floorings. Furthermore, the growth of the real estate market in emerging countries of Asia Pacific and the Middle East & Africa has contributed to the growth of the polymer modified cementitious coatings market in the residential buildings segment. The high demand for polymer modified cementitious coatings from the construction industry and infrastructural development in countries, such as China and India, are key factors driving the growth of polymer modified cementitious coatings market in the Asia Pacific region. Key players operating in the polymer modified cementitious coatings market are BASF SE (Germany), Sika AG (Switzerland), Arkema S.A. (France), Fosroc International Limited (UK), Mapei S.p.A. (Italy), Akzo Nobel N.V. (Netherlands), The Dow Chemical Company (US), Saint-Gobain Weber S.A. (France), The Lubrizol Corporation (US), Evercrete Corporation (US), Celanese Corporation (US), Lafarge Malaysia Berhad (Malaysia), Flexcrete Technologies Limited (UK), Pidilite Industries Limited (India), H.B. Fuller (US), Organik Kimya San. ve Tic. A.S. (Turkey), and Berger Paints India Limited (India). Read More: https://www.marketsandmarkets.com/PressReleases/polymer-modified-cementitious-coating.asp  The elastomeric membrane market is projected to reach USD 41.10 Billion by 2022, at a CAGR of 6.7%. The elastomeric membrane market is expected to be driven by increasing residential and non-residential construction projects that are resulting in the growth of the construction industry. Moreover, regulations for energy optimization are increasing in order to address environmental concerns. Since elastomeric membranes such as TPO and EPDM contribute to energy savings, these regulations are expected to drive the elastomeric membrane market.

Download PDF Brochure to know more: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=40007366 On the basis of end-use industry, the elastomeric membrane market has been classified into residential construction and non-residential construction. The non-residential construction segment is both, the largest and the fastest-growing. Growing foreign investments in the construction industry, high-end commercial projects, and industrial development are expected to drive this segment. Growing construction of commercial buildings such as shopping malls, multiplexes, show rooms, institutional buildings, offices, and industrial buildings are resulting in the growth of the market. Industrial construction projects are also increasing due to growing manufacturing activity and growth in retail construction to meet consumer needs. These factors are cumulatively expected to result in high growth of the elastomeric membrane market in this sector. Roofs & walls is the largest and fastest-growing application of the elastomeric membrane market owing to the high demand for sheet membranes in non-residential flat roofs. Elastomeric membrane is widely used in exterior applications and hence is a preferred choice in roofing. It can sustain adverse climatic conditions and improves the durability of roofing systems. Increasing construction of commercial and industrial buildings have further fueled the use of elastomeric membranes in this application. Based on region, the elastomeric membrane market has been segmented into Asia-Pacific, North America, Europe, the Middle East & Africa, and South America. The Asia-Pacific elastomeric membrane market is the largest and fastest-growing market due to substantial investments in residential and non-residential construction projects to meet the housing and infrastructural needs of the growing population. Cheap labor, cheap & accessible raw materials, and public infrastructure projects have boosted construction activities, thereby, increasing the demand for elastomeric membrane in this region. The key players operating in the elastomeric membrane market are BASF, Sika, Carlisle Companies Inc., SOPREMA, Kemper System, Saint-Gobain, Firestone Building Products Company, Johns Manville, GCP Applied Technologies Inc., and Standard Industries Inc. These companies undertake dynamic business strategies that lead to propelling the growth of the elastomeric membrane market. However the market is restrained due to fluctuating raw material prices. To speak to our analyst for a discussion on the above findings, click Speak to Analyst  The report "Refinish Paint Market for Automotive by Layer (Clearcoat, Basecoat, Primer, & Sealer), Resin (PU, Epoxy, & Acrylic), Technology (Waterborne, Solventborne & Powder), Vehicle (Passenger Cars, Commercial Vehicles), and Region - Global Forecast to 2022", The refinish paint market for automotive is projected to grow from USD 7.00 Billion in 2017 to USD 8.50 Billion by 2022, at a CAGR of 4.0% from 2017 to 2022. The growth of this market is driven by the increasing demand for cars, high collision rate, rising income of the middle-class population, and the propensity of car owners to repair their vehicles post any collision. In 2016, the passenger car segment accounted for the largest share of the overall automotive refinish coating market.

Download the PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=9257396 Key Target Audience:

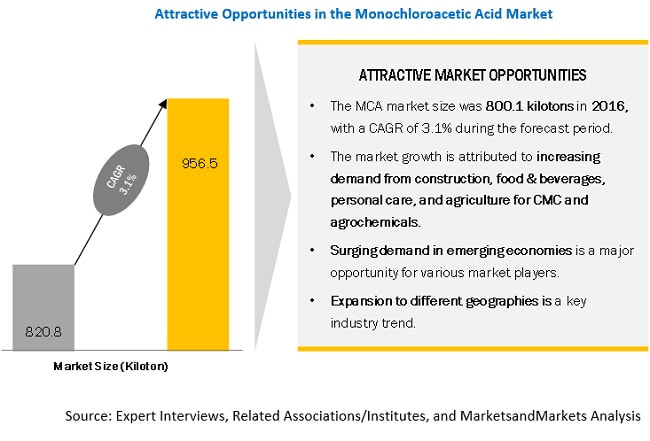

Solvent borne coating dominates the overall automotive refinish coating market. Solvent borne coating technology offers higher gloss level and excellent adhesion when compared to other technologies. It is also less affected by environmental conditions such as temperature and humidity during the curing phase. However, due to stringent environmental regulations in North America and Europe, there is a shift from solventborne to waterborne and powder coating. The refinish paint market for automotive in APAC expected to witness the highest growth during the forecast period. The growth can be majorly backed by the increasing demand for cars and rising income of middle-class population in emerging economies, such as China, India, and South Korea. Major key players are focused on inorganic growth strategies such as mergers & acquisitions to enhance its footprint as well as cater the growing demand in this region. Key players profiled in the refinish paint market for automotive report are Axalta (US), PPG Industries (US), BASF (Germany), Sherwin-Williams (US), Kansai Paint (Japan), Nippon Paint (Japan), KCC Corporation (Korea), and AkzoNobel (Netherlands) To speak to our analyst for a discussion on the above findings, click Speak to Analyst  Emerging economies such as China, India, Malaysia, Indonesia, Brazil, Mexico, Argentina, and others are some of the major markets for MCA. The growing infrastructural development and rapid urbanization in emerging economies are encouraging the rise in demand for CMC and surfactants, thus, boosting the demand for MCA.

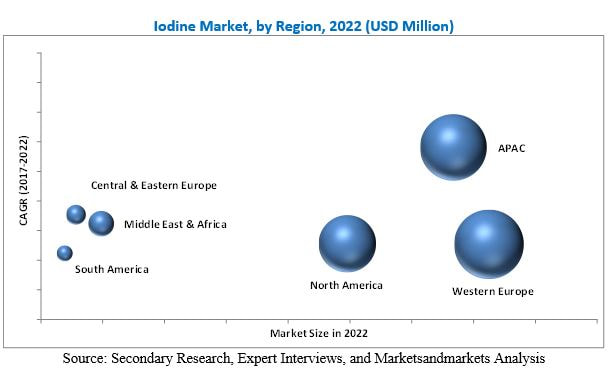

China among other emerging economies is the largest construction market. In 2016, China’s construction industry grew at 17%, a 5% increase from 2015. This growth was augmented by policy changes such as strong fiscal stimulus for infrastructure investments and easing of real estate regulations, purchase criteria, and credit availability which resulted in the growth of the domestic real estate market. Infrastructure investment will further improve, driven by mandates to meet regional development plans, initiatives such as “Belt and Road” and development of smart cities which will include optimization of urban space through public transport, high-capacity infrastructure, mixed-use development, and green city planning. In India, the constant economic growth of around 7.5% driven by government initiatives such as FDI allowance, improved policy framework, and low commodity prices have provided a strong stimulus to the construction industry. Recent deregulations for the ease of doing business are attracting foreign investments. In addition, modernization of the construction industry also drives the MCA market. The market size of Monochloroacetic Acid Market in 2016 was USD 733.4 million and is projected to reach USD 908.9 million by 2022, at a CAGR of 3.6%. CMC is the largest application of MCA that accounted for a share of 49.3%, in terms of value. Surfactants are the fastest-growing application segment of MCA, which is projected to register a CAGR of 3.5%. Download PDF Brochure to know more: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=120010112 Asia Pacific is projected to be the largest market for MCA during the forecast period. The demand for MCA is high in this region due to the large industrial base and improving lifestyles of the population. In addition to this, the increasing use of MCA for applications such as CMC, agrochemicals, and surfactants in emerging economies, such as India, China, and Indonesia also drive the Asia Pacific MCA market. Some of the key players in the MCA market include AkzoNobel (Netherlands), CABB (Germany), Daicel Corporation (Japan), PCC SE (Germany), Niacet Corporation (US), Shandong Minji Chemical (China), Denak Co. (Japan), Kaifeng Dongda Chemical Company (China), and Meridian Chem-Bond (India). Joint venture and acquisition were the major growth strategies adopted by the market players between 2014 and 2017 to cater to the demand for MCA in emerging economies. Read More: https://www.marketsandmarkets.com/PressReleases/monochloroacetic-acid.asp  Iodine is a non-metallic element with a blue-black color and lustrous appearance. It belongs to the halogen family in the periodic table and is the least reactive among the halogens. Iodine is a trace element that can be obtained mainly from three sources, which are underground brines, caliche ore, and seaweed. It is also recycled in many parts of the world, mainly in Japan. Iodine is either used in elemental or isotopic form and in the form of inorganic salts & complexes and organic compounds. It is widely used in numerous applications, such as X-ray contrast media, pharmaceuticals, iodophors, and optical polarizing films in LCDs, catalyst in polymer synthesis, biocides, human nutrition, animal feed, and fluorochemicals. Increasing use of iodine in optical polarizing films in LCD applications and growing deficiency of iodine in developing countries are the major factors driving the market for iodine globally. The growth is further driven by its application in X-ray contrast media, fluorinated derivatives, and photography. The global iodine market is estimated at USD 832.1 Million in 2017 and is projected to reach USD 1,041.0 Million by 2022, at a CAGR of 4.58% between 2017 and 2022.

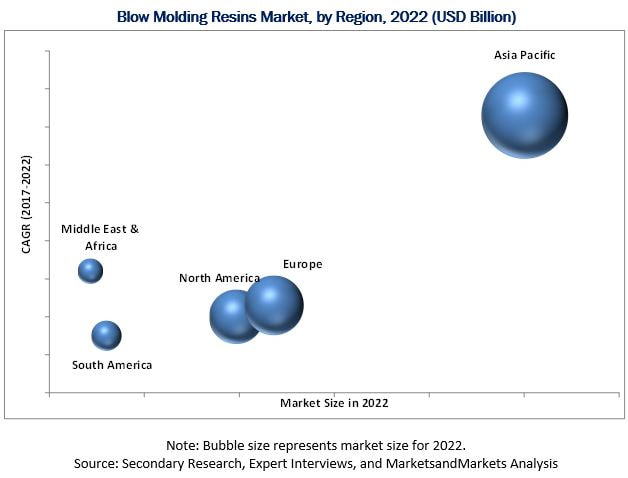

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=65097087 The Western European region was the largest market for iodine, in terms of value and volume. The high consumption of iodine in the region is attributed to the increasing demand from the healthcare and chemical industries. Growing investments in medical research, advancements in diagnostic imaging techniques, strong healthcare infrastructure with significant number of CT and MRI examinations, and growing iodine deficiency in Rest of the Western European counties are some of the factors responsible for the large market size of iodine in Western Europe. Iodine manufacturers such as Sociedad Química y Minera (SQM) (Chile), Iofina (UK), ISE Chemicals Corporation (Japan), IOCHEM Corporation (US), Compañía de Salitre y Yodo (Chile), Algorta Norte SA (Chile), Nippoh Chemicals Co., Ltd (Japan), Kanto Natural Gas Development Co., Ltd (Japan), Toho Earthtech Co., Ltd (Japan), and Godo Shigen Co., Ltd (Japan) are covered in the report. These companies have large production facilities and have adopted organic strategies to become the leading players in the global iodine market. SQM is the leading manufacturer of iodine with the largest production capacity of iodine globally. The company manufactures around 10,000 tons of iodine and its derivatives annually. The company, in 2016 launched a new product Ethyl-TriPhenyl-Phosphonium Iodide (ETPPI) through its brand Iodeal. ETPPI is a quaternary phosphonium salt used in the advancement or curing of thermosetting powder coatings and phenolic-based epoxy resins, as a phase transfer catalyst, and a Wittig reagent. This product launch helped the company enhance and broaden its product offerings. Iofina is another major company operating in iodine manufacturing after SQM. For instance, in 2017, Iofina expanded its iodine production with the construction of IO#7, a new production plant for manufacturing iodine and its derivatives. With this expansion, the company will be able to increase its iodine production with lower per kilo cost of production. Browse 109 tables and 50 figures spread through 147 pages and in-depth TOC on “Iodine Market by Source (Caliche Ore, Underground Brines), Form(organic compounds, Inorganic Salts, Elemental & Isotopes), Application(X-ray contrast media, Pharmaceuticals, Optical Polarizing Films), and Region – Global Forecast to 2022″: https://www.marketsandmarkets.com/requestsampleNew.asp?id=65097087 Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: [email protected] Visit Our Website: https://www.marketsandmarkets.com/  The Asia Pacific blow molding resins market is projected to grow at the highest CAGR during the forecast period. The growth of the Asia Pacific blow molding resins market can be attributed to the presence of the leading blow molding resins producers in the region. Moreover, the growing demand for blow molding resins in packaging applications, such as pharmaceutical and food & beverage products in countries, such as China, Japan, and India also contribute to the growth of the Asia Pacific blow molding resins market.

The increasing per capita expenditure on healthcare, personal care, and food products, large consumer base, growing urban population, low labor costs, and easy availability of raw materials are attracting international pharmaceutical, chemical, and food & beverage manufacturers to shift their production facilities to the region, thus creating high demand for the blow-molded products produced by blow molding resins in these industries. The Asia Pacific is the global manufacturing hub for the chemical industry, accounting for more than 50% of global chemical production output; this increases the demand for products, such as cans and containers, produced with the use of blow molding resins in the chemical industry. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=8448983 The target audiences for the blow molding resins market are as follows:

Exxon Mobil (US), LyondellBasell (Netherlands), DowDuPont (US), SABIC (Saudi Arabia), INEOS (Switzerland), Solvay (Belgium), Formosa Plastics (Taiwan), Chevron (US), Eastman (US), China Petroleum (China), and Reliance Industries (India), among others are the key players operating in the blow molding resins market. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=8448983 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed