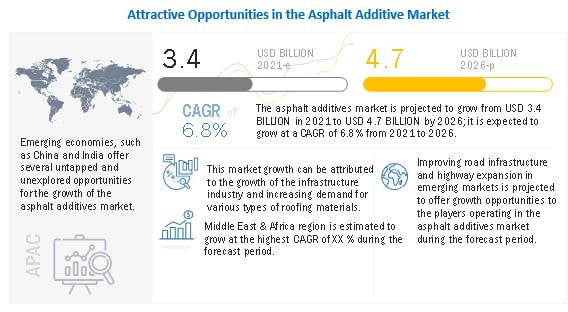

The asphalt additive market is projected to grow from USD 3.4 billion in 2021 to USD 4.7 billion by 2026, at a CAGR of 6.8% from 2021 to 2026. Increase in road construction projects along with the growing usage of asphalt additives in roofing application are some of the major key factors driving the growth of the asphalt additive market across the globe.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=156734514 Asphalt is primarily used in roofing applications for waterproofing. It is also used as a saturate in asphalt saturated felts, roll roofing, and shingles. Asphalt shingles are one of the least expensive roofing applications and are witnessing increased demand from the North American and European regions. The sub-prime crisis of 2007-2008 in the US caused a recession in the construction industry. However, the construction industry in the North American region has recovered and is growing at a moderate pace. As the market for building materials is increasing in the North American and European regions, the use of asphalt in these materials is expected to grow. Consequently, the demand for asphalt additives is also expected to increase as these improve the service life and durability of asphalt in roofing applications. The Asia Pacific region was the largest market for asphalt additives in 2020 The Asia-Pacific region was the largest market for asphalt additives in 2020, owing to the increasing demand for asphalt additives products in developing economies, such as India and China. China is the leading consumer of asphalt additives products in the Asia-Pacific region. The considerable growth and innovation, along with industry consolidations, is expected to drive the growth of the Asia-Pacific asphalt additives market. Nouryon (Netherlands), DowDuPont (US), Arkema SA (France), Honeywell International Inc. (US), Evonik Industries (Germany), Huntsman Corporation (US), Kraton Corporation (US), Ingevity Corporation(US), and BASF SE (Germany) are some of the leading players operating in the asphalt additive market. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=156734514

0 Comments

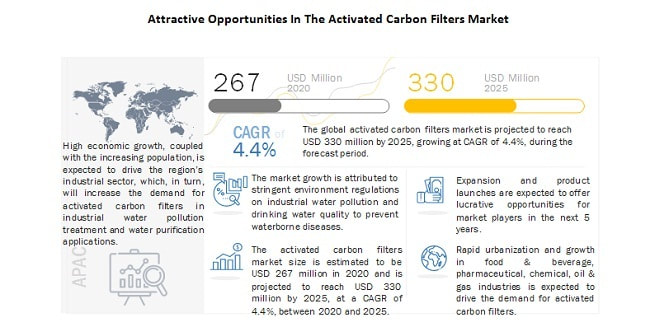

Industrial water pollution treatment is the largest application of activated carbon filters market5/5/2021  The global activated carbon filters market size is estimated at USD 267 Million in 2020 and is projected to reach USD 330 Million by 2025, at a CAGR of 4.4%, between 2020 and 2025. Activated carbon filters are used to remove organic compounds, and free chlorine from water to make it suitable for drinking and reuse in manufacturing processes or to discharge in water bodies. They are used to remove organic elements, such as humic acid and fulvic acid from potable water to prevent the formation of trihalomethanes, a class of carcinogens. They are also used for air/gas filtration in various industries. The filter media, which is used in the filtration process is activated carbon, also known as activated charcoal. Activated carbon is a form of carbon that removes organic compounds from liquids and gases by a process known as “adsorption”. It is extremely porous and thus has a very large surface area available for adsorption.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=213859954 The industrial water pollution treatment application is expected to be the largest, and drinking water purification application is expected to be the fastest-growing segment in the overall market. The global activated carbon filters market is mainly driven by the implementation of stringent regulations by regional governments and environmental agencies to control water pollution. Also, activated carbon filters are used to treat industrial discharge to re-use it in the manufacturing rocess again. Re-use of industrial discharge water and water pollution control are the two major making industrial water pollution treatment the largest application in the market. APAC is the largest as well as the fastest-growing market for activated carbon filters market. APAC is estimated to be the largest market for activated carbon filters in 2019. The market for this region is segmented into China, India, Japan, Malaysia, Indonesia, and the Rest of APAC. According to the World Bank, APAC is the fastest-growing region in terms of both population and economy. The region has witnessed significant growth in the past decade, accounting for over one-third of the world’s GDP. High economic growth, coupled with the increasing population, is expected to drive the region’s industrial sector. This is expected to increase the demand for activated carbon filters in water pollution treatment and water purification applications. Recent Developments

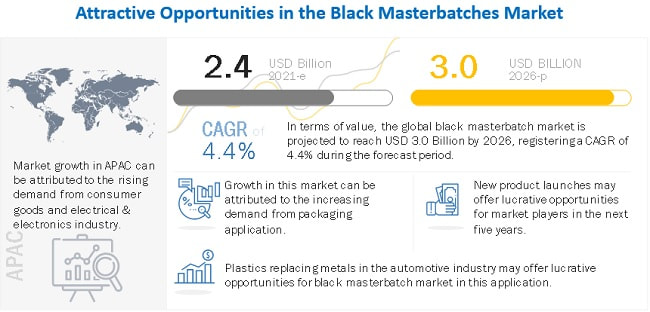

Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=213859954 Replacement of metals with plastics in automotive industry is driving the Black Masterbatches Market5/3/2021  The black masterbatches market size is estimated to be USD 2.4 billion in 2021 and is projected reach USD 3.0 billion by 2026, at a CAGR of 4.4 % between 2021 and 2026. . This growth is mainly supported by the increasing need for innovative and attractive plastic products from the packaging industry. Most of the polymer manufacturers have switched the processing method of plastics from compounding to masterbatch. This process is cost-effective and saves processing time as compared to compounded materials. American and European black masterbatch manufacturers are focusing on expanding their manufacturing facilities in emerging economies owing to cost-effective labor, low setup cost, tax benefits, and high demand for black masterbatch.

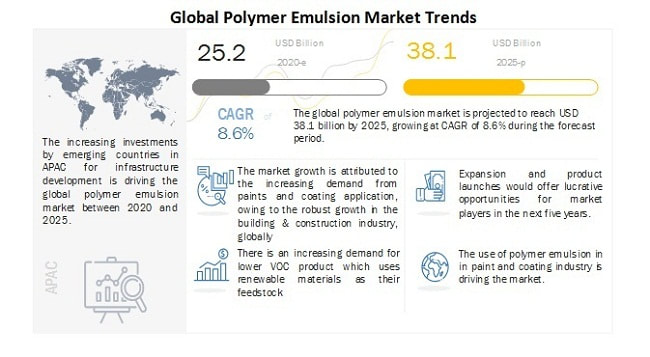

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=58392794 Plastics provide superior mechanical, physical, thermal, and electrical properties than metals. Engineering plastics are widely used in various automotive components such as steering wheels, airbags, seatbelts, bumpers, and dashboards. Continuous innovation and demand for lightweight materials in the automotive industry are encouraging the replacement of metals with plastics. It is estimated that for every 10% reduction in the weight of vehicles, fuel efficiency can be increased by 7–8%. In addition, plastics offer better design, safety, and environmental sustainability than metals. Automotive and airplane manufacturers utilize lightweight plastics such as PP and PC for windows, hoods, and interior applications. Plastics used in the manufacture of automotive components are PBT, PET, PVC, ABS, PA, PS, PC, and PE. Implementation of stringent regulations on vehicular emissions in developed nations has led to automobile manufacturers working on weight reduction of vehicles. As plastic is used for weight reduction in vehicles, the demand for plastics in the automotive industry is increasing rapidly. Black masterbatch is used in exterior applications such as vehicle bodies, bumper, headlamp lenses, body side protection strips, window sealing profiles, and tires in the automotive industry. The APAC comprises major emerging nations such as China and India. Hence, the scope for the development of most industries is high in this region. The black masterbatches market is growing significantly and offers opportunities for various manufacturers. The APAC region constitutes approximately 61.0% of the world’s population, and the manufacturing and processing sectors are growing rapidly in the region. The APAC is the largest black masterbatches market with China being the major market which is expected to grow significantly. The rising disposable incomes and rising standards of living in emerging economies in the APAC are the major drivers for this market. Key players in this market are LyondellBasell (US), Avient Corporation (US), Ampacet Corporation (US), Cabot Corporation (US), Plastika Kritis S.A. (Greece), Plastiblends India Ltd. (India), Hubron International (UK), Tosaf Group (Israel), and Penn Color, Inc. (US). The global and regional players have sizable shares in the black masterbatch market. The key players in the market are focusing on strategies, such as new product launches, partnerships & agreements, acquisitions, and expansions, to expand their businesses globally. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=58392794  The global polymer emulsion market size is projected to grow from an estimated value of USD 25.2 billion in 2020 to USD 38.1 billion by 2025, at a CAGR of 8.6% during the forecast period. The growth of the market is driven mainly by the increasing demand from growing end-use industries in emerging markets and stringent regulations regarding VOC emission.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1269 Rising environmental concerns and increasing competition amongst market players have encouraged manufacturers to continuously make technological advancement and increase the use of bio-based or green products. This is increasing the demand for lower VOC products, which uses renewable materials as their feedstock. The acrylics segment accounts for the largest share of the overall polymer emulsion market. Acrylic polymer emulsion is used widely in various applications due to its properties, such as low VOC emission and excellent durability. It is also preferred in multiple end-use applications due to its versatility. Acrylics are used to prepare polymers with rigid, flexible, ionic, nonionic, hydrophobic, or hydrophilic properties. They are transparent, have resistance to breakage, provide excellent finish gloss, improved adhesion to non-porous surfaces, and flow and stability. They are also commonly known as polyacrylates. Paints & coatings is the largest application The growth of the market is attributed to the high demand in industries, such as construction and automotive. Polymer emulsion is used widely in paints & coatings as its manufacturing process has a lower carbon footprint. The high VOC content of solvent-based products and the implementation of government regulations regarding air pollution control has stimulated the development of low VOC paints & coatings. This increased the demand for water-based paints & coatings, which in turn, drive the growth of polymer emulsions in the paints & coatings segment. APAC is the largest and fastest-growing market for polymer emulsion. The region is witnessing growth in the polymer emulsion market because of the rapid expansion of building & construction, consumer durables, and transportation sectors. The manufacturers are attracted to the region as skilled labor required for the operation of manufacturing units is available at lower wages. The presence of major polymer emulsion manufacturers and stringent government regulation related to VOC emission are major factors supporting the growth of polymer emulsion in the region. DIC Corporation (Japan), Dow Chemical Company (US), BASF SE (Germany), Arkema Group (France), Celanese Corporation (US), Trinseo (US), The Lubrizol Corporation (US), Wacker Chemie AG (Germany), Synthomer Plc (UK), and Asahi Kasei Corporation (Japan) are the major players in the polymer emulsion market. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1269 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed