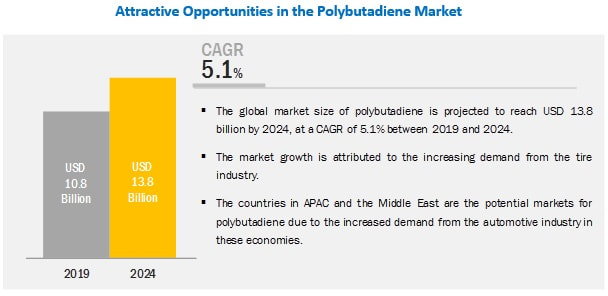

The polybutadiene market size is expected to grow from USD 10.8 billion in 2019 to USD 13.8 billion by 2024, at a CAGR of 5.1% during the forecast period. The polybutadiene market is driven by tire, polymer modification, and industrial rubber manufacturing industries. However, fluctuating raw material prices can hinder the growth of the market.

Emerging economies such as China, India, Indonesia, and Thailand are experiencing high demand for polybutadiene. Increasing disposable income, huge consumer base, rising urban population, low labour costs, and easy availability of raw materials are attracting global automobile manufacturers to shift their production facilities to the region, thus, creating a high demand for polybutadiene in this region. To know about the assumptions considered for the study download the pdf brochure Recent Developments

0 Comments

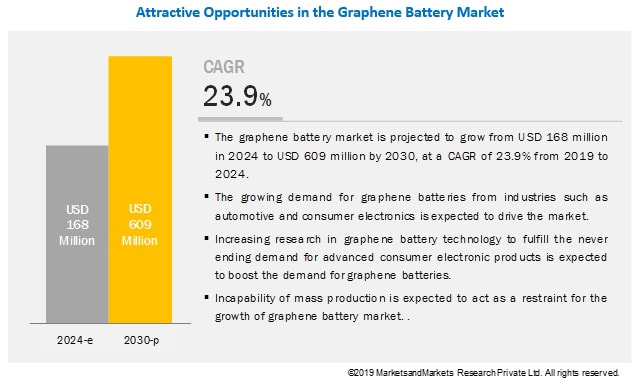

The global graphene battery market size is projected to grow from USD 168 million in 2024 to USD 609 million by 2030, at a CAGR of 23.9% from 2024 to 2030. The increasing demand for graphene batteries in consumer electronics and automotive industries is expected to drive the graphene battery market.

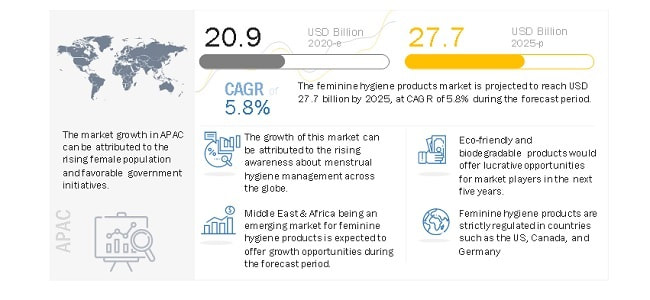

Samsung SDI (South Korea), Huawei Technologies Co., Ltd. (China), Log 9 Materials Scientific Private Limited (India), Cabot Corporation (US), Grabat Graphenano Energy (Spain), Nanotech Energy (US), Nanotek Instruments, Inc. (US), XG Sciences, Inc. (US), ZEN Graphene Solutions Ltd. (Canada), Graphene NanoChem (Malaysia), Global Graphene Group (US), Vorbeck Materials Corp. (US), Graphenea Group (Spain), Hybrid Kinetic Group Ltd. (Hong Kong) and Targray Group (Canada) are some of the leading players operating in the graphene battery market. These players have adopted the strategies of expansion and joint-venture to enhance their position in the graphene battery industry. To know about the assumptions considered for the study download the pdf brochure In line with the rising demand for graphene batteries, in December 2018, Log 9 Materials Scientific Private Limited (India) announced that they are working on graphene-based metal-air batteries. The metal-air battery uses metal as the anode, oxygen as the cathode, and water as an electrolyte. A graphene rod is used in the air cathode of the battery. Since oxygen has to be used as the cathode, the cathode material has to be porous to let the air pass, a property in which graphene excels. According to Log 9 Materials, the graphene used in the electrode can increase the battery efficiency by five times at one-third the cost. In November 2017, Samsung SDI (South Korea), in collaboration with Samsung Advanced Institute of Technology (SAIT), developed a unique “graphene ball” that could make lithium-ion batteries last longer and charge faster. Samsung Advanced Institute of Technology (SAIT) said that using the new graphene ball material to make batteries will increase their capacity by 45% and make their charging speed five times faster. It was also said that this battery would be able to maintain a temperature of 60 degrees Celsius that is required for use in electric cars. In December 2016, Huawei unveiled new graphene- Li-Ion battery with abilities to withstand high temperature (60° degrees as opposed to the existing 50° limit). The lifespan of the graphene-Li-Ion battery will also be twice that of the ordinary Li-ion battery. To achieve this breakthrough, Huawei incorporated three new technologies including a special additive in the electrolyte, cathodes with modified large-crystal NMC materials, and graphene for more efficient cooling. In June 2014, Vorbeck Materials Corp. (US) launched Vor-Power, a lightweight, flexible battery strap that can be attached to any existing bag strap to enable a mobile charging station that provides about 50 hours of additional talk or surf time. The product weighs 450 grams, provides 7,200 mAh, and is probably the world’s first graphene battery. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=96975481  The global feminine hygiene products market size is projected to grow from USD 20.9 billion in 2020 to USD 27.7 billion by 2025, at a CAGR of 5.8% during the forecast period 2020 to 2025. The growth can be attributed to the increasing female population and rapid urbanization.

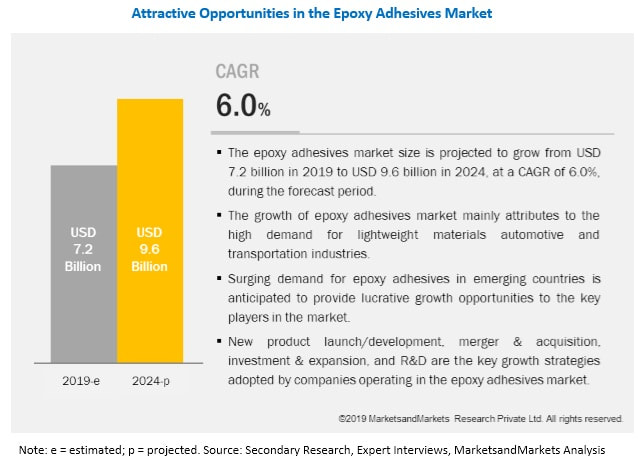

Asia Pacific accounted for the largest share of the feminine hygiene products market in 2019. The countries considered for study in the Asia Pacific feminine hygiene products market include China, India, Japan, Indonesia, Malaysia, and Thailand. Growing disposable income, rapid urbanization, and awareness about menstrual hygiene management are driving the feminine hygiene products market in this region. Recently, the Indian government announced plans to invest USD 160 million in the Suvidha initiative, a scheme to ensure proper access to sanitary napkins in rural areas of the country. The government plans to provide biodegradable sanitary napkins to the masses at the cost of USD0.00014 through this scheme. The government plans to involve high net worth individuals (HNIs) and corporates to assist in distributing sanitary napkins to underprivileged women across the country. These developments will further boost the demand for feminine hygiene products. To know about the assumptions considered for the study download the pdf brochure Johnson & Johnson (US), Procter & Gamble (US), Kimberly-Clark (US), Essity Aktiebolag (publ) (Sweden), Kao Corporation (Japan), Daio Paper Corporation (Japan), Unicharm Corporation (Japan), Ontex (Belgium), Hengan International Group Company Ltd. (China), and Drylock Technologies (Belgium) are some of the leading players operating in the feminine hygiene products market. These players have adopted the strategies of acquisitions, expansion, and product launches to enhance their position in the market. In May 2020, Ontex announced plans for new personal hygiene manufacturing plant in Rockingham County, North Carolina, US. The new facility is scheduled to start production from mid-2021. The company has a presence in 21 countries, and it has 19 manufacturing sites in 15 countries in Europe, Russia, the Middle East, Africa, Pakistan, Australia, and the Americas. It also has around 30 sales and marketing offices and nine dedicated R&D centers. Kao Corporation entered into a partnership with the United Nations Population Fund in February 2019 to support the Menstrual Hygiene Improvement Project in Uganda. Kao is providing funds to EcoSmart Uganda Ltd., a start-up company founded by five young social entrepreneurs in Uganda, to domestically produce sanitary napkins. Kao Corporation operates its feminine hygiene business through the human health care segment. The company has sales and distribution facilities across Japan and other countries. It has a portfolio of over 20 leading brands. Read More: https://www.marketsandmarkets.com/PressReleases/feminine-hygiene-product.asp  The global epoxy adhesives market size is projected to grow from USD 7.2 billion in 2019 to USD 9.6 billion by 2024, at a CAGR of 6.0%.

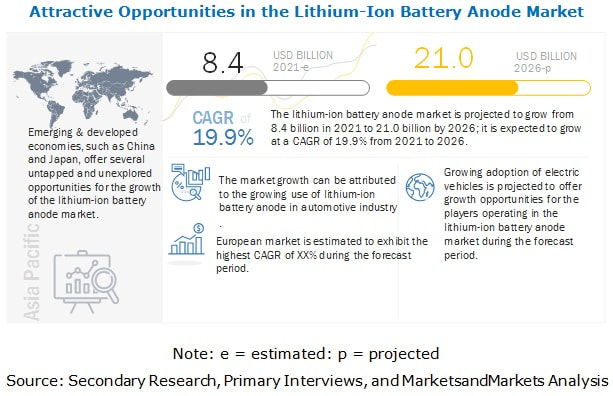

Increasing urbanization and growing usage of composites, plastics, and other higher strength metals in the construction industry is driving the global epoxy adhesives market. Epoxy adhesives offer the ability to adhere strongly, with exceptional mechanical & electrical insulating properties and chemical and heat resistance. Early buyers will receive 10% customization on reports: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=142980020 One-component type is expected to withess the highest growth during the forecast period. The one-component based epoxy adhesives market is estimated to grow at the highest CAGR from 2019 to 2024, in terms of volume. The excellent properties of the one-component type adhesives such as, quick curing time, a solvent-less system, and consumer friendly usage, is driving the demand in this segment. Building & construction is projected to be the largest end user of epoxy adhesives. The building & construction industry accounted for the largest share of the overall epoxy ahdesives market, in terms of volume, followed by the automotive industry. The building & construction industry started using epoxy adhesives with the increasing usage of composites, plastics, and other higher strength metals. Growing urbanization is fueling the growth of the construction sector, which is driving the epoxy adhesives market. Epoxy adhesives market in APAC is projected to witness the highest CAGR during the forecast period. APAC is projected to be the fastest-growing epoxy adhesives market during the forecast period. China is the largest market for epoxy adhesives in the region. However, India and Thailand are the fastest-growing markets for epoxy adhesives in the region. Owing to increased government investments in developing countries for infrastructure, such as public utilities, commercial, and entertainment structures, and housing demands to cater to the steadily-growing population, the demand for epoxy adhesives in this region is expected to growth significantly. The major players in the epoxy adhesives market include Henkel AG (Germany), Sika AG (Switzerland), 3M Company (US), H.B. Fuller (US), DuPont (US), Illinois Tool Works Incorporation (US), Ashland (US), RPM International (US), Lord Corporation (US), and Huntsman Corporation (US). Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=142980020  The global lithium-ion battery anode market size is projected to grow from USD 8.4 billion in 2021 to USD 21.0 billion by 2026, at a CAGR of 19.9% from 2021 to 2026. Factors such as strict government mandates on fuel economy, rising concerns related to environmental issues, which include greenhouse gas and an increase in R&D initiatives are expected to drive the growth of the market.

Europe is the second-largest consumer of lithium-ion battery anode and accounted for a share of 6.1% of the global market, in terms of value, in 2020. The region is home to some of the largest battery manufacturers, such as Saft (France) and FIAMM (Italy). Batteries have major applications as clean, sustainable, and compact sources of power in automotive. The region is witnessing significant growth in the demand for EVs which is largely dependent on government incentives and funds. Growth in demand for electric vehicle has increased the demand for lithium-ion battery anode which in return has fueled the demand for lithium-ion battery anode in the region. To know about the assumptions considered for the study download the pdf brochure Some of the key players in the lithium-ion battery anode market include Showa Denko Materials (Japan), JFE Chemical Corporation (Japan), Kureha Corporation (Japan), SGL Carbon (Germany), Shanshan Technology (China), and POSCO CHEMICAL (South Korea). The lithium-ion battery anode market report analyzes the key growth strategies adopted by the leading market players between 2017 and 2021, which include expansions, investments, and mergers & acquisitions. Showa Denko Materials is one of the leading companies engaged in the manufacturing of lithium-ion battery materials. The company manufactures a wide range of chemicals and electronics related products. In April 2021, Showa Denko Materials established a local production for graphite electrodes in Southeast Asia and Europe. This will help the company to strengthen its supply chain and geographical presence. Another player in the lithium-ion battery anode market is SGL Carbon. The company is among the leading manufacturers of specialty graphite and composite materials. In April 2021, SGL Carbon signed a collaboration agreement with Altech Chemicals for the development of high purity alumina-coated (HPA) graphite materials for use by the lithium-ion battery industry in anode application. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=147095907  The global polymer emulsion market size is projected to grow from an estimated value of USD 25.2 billion in 2020 to USD 38.1 billion by 2025, at a CAGR of 8.6% during the forecast period. Monomers dissolved in water are known as polymer emulsions. They are formed by a chain reaction known as emulsion polymerization. They are also known as waterborne polymers due to their water content. Polymer emulsions are used increasingly as substitutes for solvent-based polymers. Polymer emulsions have high molecular weight and are considered eco-friendly as they have low VOCs. The key applications of polymer emulsion are paints & coatings, paper & paperboard, adhesives & sealants, and others.

The key players in the blowing agents market are DIC Corporation (Japan), Dow Chemical Company (US), BASF SE (Germany), Arkema Group (France), Celanese Corporation (US), Trinseo (US), The Lubrizol Corporation (US), Wacker Chemie AG (Germany), Synthomer Plc (UK), Asahi Kasei Corporation (Japan), and others. These players adopt various developmental strategies such as expansions, new product development, agreement, and acquisitions to expand their market share. To know about the assumptions considered for the study download the pdf brochure Recent Developments

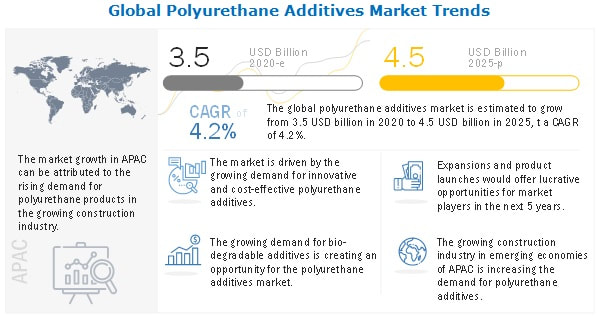

The polyurethane additives market size is projected to reach USD 4.5 billion by 2025 at a CAGR of 4.2% from 2020. The demand for polyurethane additives in emerging economies, such as APAC and South America, is increasing owing to the growing construction industry. The volatility in raw material prices and the recyclability of polyurethanes is hindering the polyurethane additives market. The demand for polyurethane additives is increasing, owing to the growing demand for innovative and cost-effective additives. This increase in demand for bio-based polyurethane additives provides growth opportunities to the market. On the other hand, the increasing regulatory pressure towards the usage of bio-based products is the major challenges for the market.

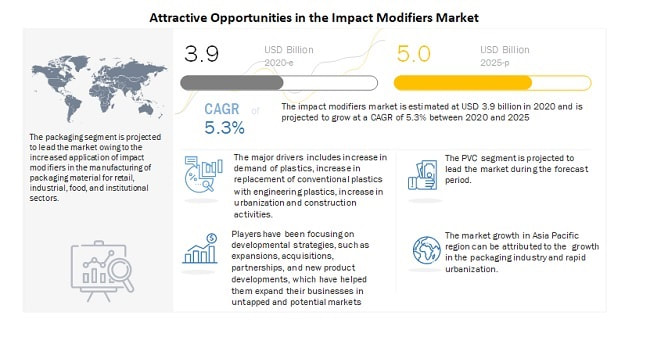

Driver: Increasing demand for innovative and cost-effective additives Flexible polyurethane foam is an important material finding usages in mattresses, furniture cushioning, bedding, carpet underlay, automotive interiors, etc. These being highly cellular polymers are easily ignitable. This characteristic limits their greater use in areas that require them to pass certain fire regulations as fire hazards are associated with the use of these polymeric materials, which can cause loss of life and property, are of particular concern among government regulatory bodies, consumers, and manufacturers alike. This further drives the demand for innovating new additives such as flame retardants to reduce the flammability of polyurethanes. A large range of flame retardants such as inorganic phosphorus, organophosphorus, nitrogen, halogen, and phosphorus-halogen based compounds are used to meet the demand for the required additives. To know about the assumptions considered for the study download the pdf brochure Restrain: Volatility in the raw material prices Raw materials used for manufacturing polyurethane are primarily extracted from crude oil. According to the US EIA (Energy Information Administration), in 2020, Brent crude oil spot prices averaged USD 40 per barrel in June, up to USD 11 per barrel from May and up to USD 22 per barrel from the multiyear lows from April. Prices rose as OPEC+ producers agreed to extend the deepest production cuts through July, and many locations, previously on lockdown, demanded more liquid fuels. Given supply reductions and rising demand, the EIA estimated that global oil inventories declined in June 2020 for the first time since December 2019. The global oil inventory averaged 8.4 million barrels per day, which caused crude oil prices to drop sharply. Owing to such fluctuating crude oil prices, raw material prices of polyurethane additives are volatile. Opportunity: Emerging market for environment-friendly polyurethane additives A few polyurethane additives are hazardous, and their application is limited owing to negative effects on polymer mechanical properties. Accordingly, identifying materials that are environmentally friendly and harmless to humans has become urgent. There are a few alternative polyurethane additives that are gaining research interest. Those are natural and recyclable resources that can enhance the flame retardant properties of other polymers. Room for improvement is always present as the related technology is continually developed. Hence, the growing demand for environment friendly polyurethane additives is creating a growth opportunity for the market. Challenge: Increasing regulatory pressure on the usage of eco-friendly products Various measures have been adopted across different countries to create a sustainable environment. There are various regulations that put pressure on chemical manufacturers to produce environmentally friendly products. The EPA (Environmental Protection Agency) has banned a few chemicals that are hazardous to the environment. Extensive research is conducted to develop environment-friendly products. Moreover, the regulations are stricter in various countries of Europe and in California (US). Hence, it is building pressure on chemical manufacturers to produce environment-friendly alternatives that provide the same quality and performance as of the chemicals that are not environment friendly. APAC is projected to be the fastest-growing market for polyurethane additives. The rising population, increased demand for automobiles, growing disposable income, rapid industrialization, and increased urbanization are driving the APAC polyurethane additives market. China is the largest market for polyurethane additives in the region. China is also a major producer and consumer of polyurethane additives in the region as it has a huge manufacturing base. Apart from China, India and South Korea are projected to grow at a decent rate during the forecast period. The key players in the non-phthalate plasticizers market include Evonik Industries (Germany), BASF (Germany), Huntsman Corporation (US), Covestro (Germany), Dow Inc. (US), Lanxess AG (Germany), lbemarle Corporation (US), Tosoh Corporation (Japan), Momentive (US), and BYK (US). These players have established a strong foothold in the market by adopting strategies, such as expansion and new product launch. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=121317889  The global impact modifiers market size is estimated at USD 3.9 billion in 2020 and is projected to reach USD 5.0 billion by 2025, at a CAGR of 5.3% from 2020 to 2025. Impact modifiers are additives that enable plastic products to absorb shocks and protect these products from cracking or breaking. The use of impact modifiers improves the properties of polymers, such as impact strength, toughness, and hardness. The amount of impact modifier added depends upon the level of impact resistance needed for end-use applications.

Plastics have many applications in several industries, such as packaging, construction, automotive, consumer goods, textile, agriculture, and medical, among others. Plastics, especially engineering plastics, possess superior mechanical and electrical properties, excellent abrasion resistance, superior chemical resistance, and other properties in comparison to those of conventional materials such as metals, glass, paper, and ceramics. To know about the assumptions considered for the study download the pdf brochure Continuous innovation and the need for lighter material in several applications are encouraging the replacement of conventional materials with plastic. The increase in consumption of polymers has also increased the usage of impact modifiers in the manufacturing of products for various applications, which improve the mechanical and impact properties of the final product and reduce its cycle time. PVC is the largest application segment of the impact modifiers market by application. The growth of impact modifiers in PVC application is mainly attributed to its easy availability and low cost as well as the increasing applicability of PVC among varied end-use industries, such as packaging, construction, automotive, and consumer goods. PVC is mainly used in pipes, windows, flooring, roofing, inflatable structures, and lighter structures. It contributes to the quality, cost-effectiveness, and safety of construction material. The impact modifiers market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific impact modifiers market in 2019. Moreover, the Asia Pacific region is an emerging and lucrative market for impact modifiers, owing to industrial development and improving economic conditions. The presence of a number of plastic products manufacturing plants in China and rapid industrialization in Asia Pacific are expected to drive the impact modifiers market during the forecast period. Major companies such as Dow Inc. (US), Lanxess A.G. (Germany), Kaneka Corporation (Japan), Arkema S.A. (France), Mitsubishi Chemical Corporation (Japan), LG Chem Ltd. (South Korea), Shandong Ruifeng Chemical Co., Ltd. (China), Mitsui Chemicals, Inc. (Japan), Wacker Chemie AG (Germany), Formosa Plastics Corp. (Taiwan), Sundow Polymers Co., Ltd. (China), SI Group, Inc. (US), Akdeniz Kimya San. ve Tic. Inc. (Turkey), ), En-Door (China), Novista Group (China), and Indofil Industries Limited (India) and among others. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=58674504 The global feminine hygiene products market size is projected to grow from USD 20.9 billion in 2020 to USD 27.7 billion by 2025, at a CAGR of 5.8% during the forecast period 2020 to 2025. The market growth is driven by the rise in awareness about feminine hygiene management and the increasing disposable income of females.

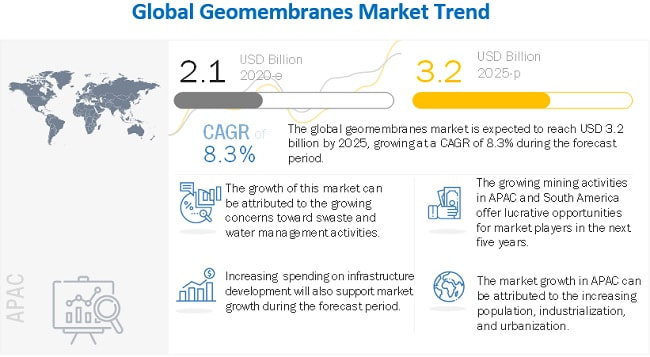

Driver: Rising female literacy and awareness of menstrual health & hygiene Over the last decade, global agencies and organizations such as UNICEF and UNESCO have been active in raising literacy levels of young females in under-developed and developing countries as rising female literacy will have a positive impact on feminine health management. UNICEF also views menstrual health and hygiene as a fundamental right of women and girls and hence has termed it as a key objective in its Sustainable Development Goals (SDGs) for 2030. The rising literacy level among females is expected to have a positive impact on the overall feminine health management and thus is directly linked to the adoption of feminine hygiene products. As a result, rising female literacy is expected to drive the feminine hygiene products market. To know about the assumptions considered for the study download the pdf brochure Restraint: Social stigma associated with menstruation and feminine hygiene products The common perception and stigma associated with menstruation acts as a major disadvantage for many women. According to the Essity Health & Hygiene Report 2019, one of four women come under the menstruating age in the world. Women who menstruate not only need a private space for washing and managing their menstruation but also need feminine hygiene products and an appropriate place for disposal. These needs are often overlooked in rural areas, making menstruation an impediment in community participation, education, and working life. According to UNICEF, menstrual and hygiene needs remain unchecked due to gender inequality, discriminatory social norms, cultural taboos, and poverty. Girls face stigma, harassment, and social exclusion during menstruation. This compels girls and women to adopt traditional feminine hygiene products or completely avoid using them. For example, girls in Bolivia were reported carrying around used sanitary napkins because they believe the blood could cause disease if it comes in contact with other garbage. In many societies, tampons are reserved for married women in fear that they can rupture the hymen. Opportunity: Developing eco-friendly feminine hygiene products Currently, the issue of the non-biodegradability of feminine hygiene products is a serious environmental concern. However, the development of eco-friendly products such as sanitary napkins from the natural fiber is a sustainable option to advance in this market. The naturally available absorbent fibers such as organic cotton, banana fiber, jute, and bamboo etic are widely available, are biodegradable in nature, and have a low carbon footprint. The use of these fibers also reduces the manufacturing cost of sanitary napkins. Companies such as Saathi, Carmesi, Heyday, Everteen, Purganic, and Aakar are producing sanitary napkins using 100% eco-friendly biodegradable products. Moreover, these companies enable women in rural locations to produce and distribute affordable and biodegradable sanitary napkins to the masses. This sustainable solution for developing sanitary napkins provides a unique opportunity for companies to enter the market. Challenge: Impact of feminine hygiene products on the environment Currently, the environmental impact caused by sanitary napkins is one of the widely debated issues. A plastic disposable sanitary napkin requires approximately 500-800 years to decompose completely. Thousands of tons of disposable sanitary napkin waste are generated every month all over the world. According to Menstrupedia, a digital guide for information on menstruation and issues, approximately 432 million sanitary napkins are generated in India annually, which can potentially cover landfills spread over 24 hectares. According to The Good Trade, over 20 billion feminine hygiene products end up in a landfill every year in the US, and tons of waste can be found scattered or clogged in waterways in low-income countries that lack the infrastructure to dispose of this waste. Most of the chemicals from these products cause groundwater pollution and loss of soil fertility, and hence disposing of them is a major issue. Incineration has often been considered as another alternative to a landfill; however, the operational costs and further environmental damage in terms of toxic fumes create additional issues. Asia Pacific accounted for the largest share of the feminine hygiene products market in 2019. The countries considered for study in the Asia Pacific feminine hygiene products market include China, India, Japan, Indonesia, Malaysia, and Thailand. Growing disposable income, rapid urbanization, and awareness about menstrual hygiene management are driving the feminine hygiene products market in this region. Recently, the Indian government announced plans to invest USD 160 million in the Suvidha initiative, a scheme to ensure proper access to sanitary napkins in rural areas of the country. The government plans to provide biodegradable sanitary napkins to the masses at the cost of USD0.00014 through this scheme. The government plans to involve high net worth individuals (HNIs) and corporates to assist in distributing sanitary napkins to underprivileged women across the country. These developments will further boost the demand for feminine hygiene products. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=69114569  The global geomembranes market size is expected to grow from USD 2.1 billion in 2020 to USD 3.2 billion by 2025, at a Compound Annual Growth Rate (CAGR) of 8.3%. The major driving factors are increasing mining activities in APAC and South America and the growing concerns towards waste and water management activities.

To know about the assumptions considered for the study download the pdf brochure Driver: Increased mining activities in APAC and South America Rapid industrialization and urbanization in key countries such as China and India have spurred the demand for metals and minerals in the past few years. Other countries in APAC that have attracted significant mining investments include Australia, New Zealand, Japan, South Korea, Singapore, Mongolia, and Indonesia. South America is also a high-growth region for the mining industry. It has become a preferred destination for mining investments by major global mining companies. Key countries such as Brazil, Peru, and Chile have large mining capacities and have witnessed increased investments from foreign companies over the past five years. The mining industry is one of the major consumers of geomembranes. Geomembranes are used to help recapture and recycle the harmful chemicals being used in solution to treat ponds and secondary containment applications. This is expected to drive the geomembranes market during the forecast period. Restrain: Fluctuating raw material prices on account of volatility in crude oil prices Volatility in crude oil prices is one of the major restraining factor for geomembranes manufacturers. Most raw materials for geomembranes are petroleum-based and are vulnerable to fluctuations in crude oil prices. The rise or fall in crude oil prices directly impacts the price of the raw materials required for geomembranes. Manufacturers have to cope with high and volatile raw material costs, which reduce their profit margins. This scenario has compelled market players to enhance the efficiency and productivity of their operations to sustain growth and retain market share. Opportunity: Increasing spending on infrastructure development Infrastructure development includes creating water supply and treatment plants, roads, tunnels, dams, railways, airports, bridges, telecommunication networks, schools, and hospitals. According to the Confederation of International Contractors’ Associations (CICA), the output for residential and non-residential (including commercial, industrial, and others) infrastructures will grow by 85%, in terms of volume, to reach USD 15.5 trillion by 2030. There are a multitude of applications for geomembranes within construction sector.. The long shelf-life along with good physical & mechanical properties of geomembranes will work in favor of the market. Thus, growing infrastructural developments, are expected to create growth opportunities for the geomembranes market during the forecast period. Based on region, the geomembranes market has been segmented into APAC, Europe, North America, the Middle East & Africa, and South America. North America geomembranes market was the largest market in 2019. Market growth is primarily due to enormous potential in mining, wastewater management, and infrastructural activities in the US, Canada, and Mexico. Europe North America was the second-largest market for geomembranes owing to well-established manufacturing and construction sector of the region. Major vendors in the geomembranes market include Solmax (Canada), Raven Industries (US), AGRU (Austria), Carlisle Construction Materials LLC (US), Atarfil (Spain), PLASTIKA KRITIS (Greece), JUTA (Czech Republic), Maccaferri (Italy), Firestone Building Products (US), The NAUE group (Germany), Anhui Huifeng New Synthetic Materials (China), Carthage Mills (US), Environmental Protection (US), Geofabrics (Australia), Geosynthetics Limited (UK), Ginegar Plastic Products (Israel), Global Synthetics (Australia), Layfield Group (Canada), CETCO (US), Nilex (Canada), SOTRAFA (Spain), SOPREMA (France), Texel Industries Limited (India), Titan Environmental Containment (Canada), and US Fabrics (US). Read More: https://www.marketsandmarkets.com/PressReleases/geomembranes.asp |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed