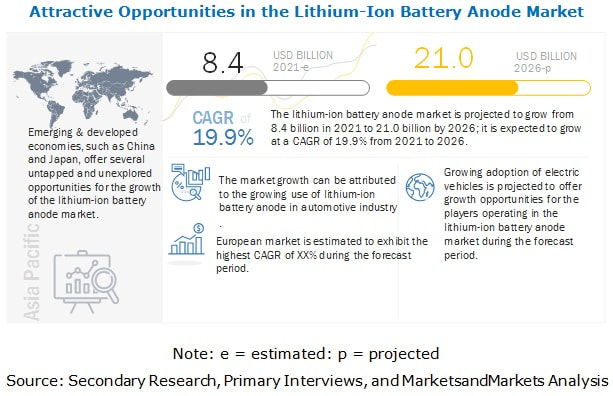

The global lithium-ion battery anode market size is projected to grow from USD 8.4 billion in 2021 to USD 21.0 billion by 2026, at a CAGR of 19.9% from 2021 to 2026. The growing demand for electric vehicles along with the high demand for lithium-ion batteries for industrial applications is driving the market growth. Moreover, strategies such as agreements and plant expansions undertaken by several prominent players in the lithium-ion battery anode industry are further fueling the lithium-ion battery anode industry growth across the globe.

The agreements, as well as plant expansions made by many prominent players in the lithium-ion battery anode industry, are one of the key factors. The lucrative market opportunities in the regions of China, Hungary, Germany, and Poland, as well as the rising concerns related to environment due to the usage of fossil fuels, are expected to boost the lithium-ion battery anode market. The key players in the lithium-ion battery anode market include Showa Denko Materials (Japan), JFE Chemical Corporation (Japan), Kureha Corporation (Japan), SGL Carbon (Germany), Shanshan Technology (China), and POSCO CHEMICAL (South Korea). The lithium-ion battery anode market report analyzes the key growth strategies adopted by the leading market players between 2017 and 2021, which include expansions, investments, and mergers & acquisitions. To know about the assumptions considered for the study download the pdf brochure Recent Developments

JFE Chemical Corporation manufactures organic and chemical materials. JFE Chemical Corporation works as a subsidiary of JFE Steel which is one of the business division of JFE Group Holdings. The company was formed with the merger of the Chemicals Division of Kawasaki Steel Corporation and Adchemco which was the chemicals business subsidiary of NKK Corporation. JFE Chemical Corporation has a strong presence in Japan along with a significant presence in China, Thailand, and Hong Kong. It has manufacturing centers located in Chiba, Kurashiki, Kasaoka city of Japan. The company also has a research and development center located in Chiba, Japan. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=147095907

0 Comments

The global silane coupling agents market size is estimated to grow from USD 1.2 billion in 2021 to USD 1.6 billion by 2026, at a CAGR of 5.5% during the forecast period. The driving factors for the silane coupling agents market is increasing penetration of silane coupling agents in the automotive & transportation, building & construction industry, energy & chemical segment, and electrical & electronics industry in the emerging economies, such as India, China, and the Middle-East, Thailand, Indonesia, Brazil, and Argentina.

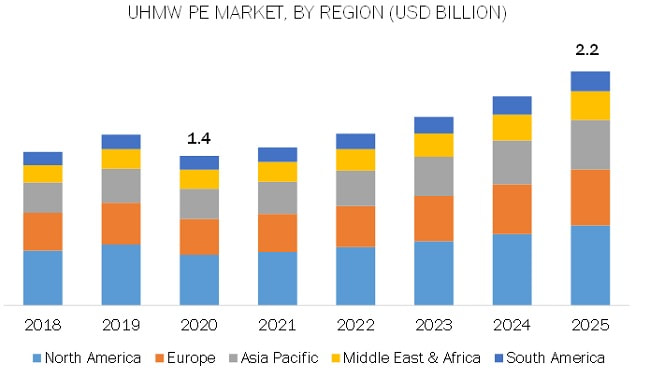

APAC accounted for the largest share of the Silane coupling agents market in 2020. The market in the region is growing because of increased foreign investments because of cheap labor and availability of raw materials. The demand for silane coupling agents in APAC is expected to increase in the next five years, due to many ongoing and upcoming building & construction projects, and industrial projects in Southeast Asian countries. High economic growth and heavy investments in these applications play a key role in driving the silane coupling agents market. Dow (US), Wacker Chemie AG (Germany), Evonik Industries AG (Germany), Shin-Etsu Chemical Co. Ltd. (Japan), Momentive (US), Gelest Inc. (US), Nanjing Union Silicon Chemical Co., Ltd (China), 3M (US), and WD Silicones (China), among others, are the leading silane coupling agents manufacturers, globally. These companies adopted new product launch, expansion, agreements & contracts and merger & acquisition, as their key growth strategies between 2016 and 2021 to earn a competitive advantage in the silane coupling agents market. To know about the assumptions considered for the study download the pdf brochure Dow is one of the largest player in the silane coupling agents market. It operates through Performance Materials & Coatings, Industrial Intermediates & Infrastructure, and Packaging & Specialty Plastics business segments. The product list involves acrylics, ethylene vinyl acetate (EVA), methacrylic acid copolymer resins, polyethylene (PE), high-density polyethylene (HDPE), ethylene dichloride (EDC), methylene diphenyl diisocyanate (MDI), among others. The company has strong financial backgrounds and geographical presence with 106 manufacturing sites in 31 countries. Shin-Etsu chemical Co. Ltd. is the second-largest player of the silane coupling agents market, globally. The company strives to maintain and further strengthen its leadership position in the silane coupling agents market by continuously expanding its business and launching new products that meet the increasing global demand. In September 2018, Shin-Etsu Chemical decided to make a USD 900 million facility investment in its silicones business. It will expand production capacity both in Japan and globally for silicone products. Read More: https://www.marketsandmarkets.com/PressReleases/silane-coupling-agent.asp  The ultra-high molecular weight polyethylene (UHMW PE) market is estimated at USD 1.4 billion in 2020 and is projected to reach USD 2.2 billion by 2025, at a CAGR of 9.4% from 2020 to 2025. Ultra-High Molecular Weight Polyethylene (UHMW PE) is a simple linear background polyethylene possessing unique properties. Due to its ultra-high molecular density, it provides high abrasion resistance and impact strength in comparison to other engineering polymers. Apart from this, the material can also be optimized for more application specific requirements such as noise resistance, low coefficient of friction, excellent chemical resistance, self-lubrication, bio-compatibility, wear resistance, and electric insulation resistance.

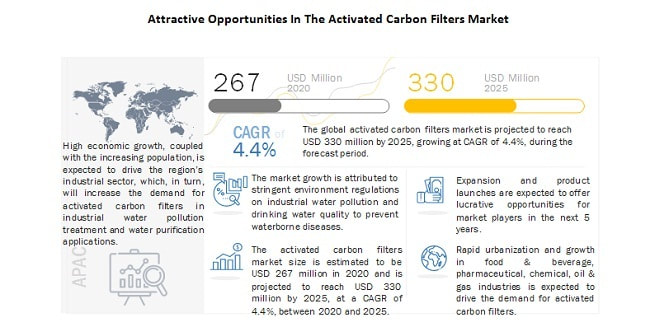

To know about the assumptions considered for the study download the pdf brochure The UHMW PE market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific UHMW PE market in 2019. The Asia Pacific region is an emerging and lucrative market for UHMW PE, owing to industrial development and improving economic conditions. In addition, the growth of the medical industry in Asia Pacific is one of the reason leading to an increase in the demand for UHMW PE. UHMW PE is also being used in mechanical equipment. The presence of a number of mechanical component manufacturing plants in China and rapid industrialization in Asia Pacific are expected to drive the UHMW PE market in the coming years. Based on end-use industry, the healthcare & medical segment is expected to grow Increasing demand for UHMW PE by the healthcare & medical industry is expected to drive the market across regions. In the healthcare & medical industry, there is a high demand for UHMW PE for the manufacture of orthopedic implants and parts for medical devices due to properties such as high strength to weight ratio, self-lubrication, and impact resistance. The growing demand for orthopedic implants from developed countries is expected to fuel the growth of the UHMW PE market globally. The decline in the age group of people undergoing knee and hip surgeries, the demand for UHMW PE has increased in the healthcare & medical industry. UHMW PE possesses the basic requirements for any medical implant material, which includes biological stability, biocompatibility, toughness, high creep resistance, low friction, and low wear. Major companies such as Celanese Corporation (US), Koninklijke DSM N.V. (Netherlands), LyondellBasell Industries N.V. (Netherlands), Braskem S.A (Brazil), Asahi Kasei Corporation, (Japan) Du Pont De Nemours Inc. (US), Saudi Arabia Basic Industries Corporation (Saudi Arabia), Mitsui Chemicals, Inc. (Japan), Honeywell International, Inc. (US), and Teijin Limited (Japan) and others are key players in the UHMW PE market. These players have been focusing on developmental strategies, such as expansions, acquisitions, partnerships, joint veture, and new product developments, which have helped them expand their businesses in untapped and potential markets. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=257883188  The global activated carbon filters market size is estimated at USD 267 Million in 2020 and is projected to reach USD 330 Million by 2025, at a CAGR of 4.4%, between 2020 and 2025. Activated carbon filters are used to remove organic compounds, and free chlorine from water to make it suitable for drinking and reuse in manufacturing processes or to discharge in water bodies. They are used to remove organic elements, such as humic acid and fulvic acid from potable water to prevent the formation of trihalomethanes, a class of carcinogens. They are also used for air/gas filtration in various industries. The filter media, which is used in the filtration process is activated carbon, also known as activated charcoal. Activated carbon is a form of carbon that removes organic compounds from liquids and gases by a process known as “adsorption”. It is extremely porous and thus has a very large surface area available for adsorption.

To know about the assumptions considered for the study download the pdf brochure The key players in the activated carbon filters market are TIGG LLC (US), Puragen Activated Carbons (US), Cabot corporation (US), Westech Engineering (US), Kuraray Co. Ltd. (Japan), Lenntech B.V. (The Netherlands), Donau Carbon Gmbh (Germany), General Carbon Corporation (US), Sereco SR.L. (Italy), Carbtrol Corp (US). The activated carbon filters market report analyzes the key growth strategies adopted by the leading market players, between 2016 and 2019, which include expansions, new product developments, and collaborations. Recent Developments

APAC is estimated to be the largest market for activated carbon filters in 2019. The market for this region is segmented into China, India, Japan, Malaysia, Indonesia, and the Rest of APAC. According to the World Bank, APAC is the fastest-growing region in terms of both population and economy. The region has witnessed significant growth in the past decade, accounting for over one-third of the world’s GDP. High economic growth, coupled with the increasing population, is expected to drive the region’s industrial sector. This is expected to increase the demand for activated carbon filters in water pollution treatment and water purification applications. Don’t miss out on business opportunities in Activated Carbon Filters Market. Speak to our analyst and gain crucial industry insights that will help your business grow. The Dow Chemical Company (US), and BASF SE (Germany) are Key Players in Polymer Emulsion Market8/9/2021  The global polymer emulsion market size is estimated at USD 25.2 billion in 2020 and is projected to reach USD 38.1 billion by 2025, at a CAGR of 8.6%, between 2020 and 2025. Monomers dissolved in water are known as polymer emulsions. They are formed by a chain reaction known as emulsion polymerization. They are also known as waterborne polymers due to their water content. Polymer emulsions are used increasingly as substitutes for solvent-based polymers. Polymer emulsions have high molecular weight and are considered eco-friendly as they have low VOCs. The key applications of polymer emulsion are paints & coatings, paper & paperboard, adhesives & sealants, and others.

APAC is the largest and fastest-growing market for polymer emulsion. The region is witnessing growth in the polymer emulsion market because of the rapid expansion of building & construction, consumer durables, and transportation sectors. The manufacturers are attracted to the region as skilled labor required for the operation of manufacturing units is available at lower wages. The presence of major polymer emulsion manufacturers and stringent government regulation related to VOC emission are major factors supporting the growth of polymer emulsion in the region. To know about the assumptions considered for the study download the pdf brochure The key players in the blowing agents market are DIC Corporation (Japan), Dow Chemical Company (US), BASF SE (Germany), Arkema Group (France), Celanese Corporation (US), Trinseo (US), The Lubrizol Corporation (US), Wacker Chemie AG (Germany), Synthomer Plc (UK), Asahi Kasei Corporation (Japan), and others. These players adopt various developmental strategies such as expansions, new product development, agreement, and acquisitions to expand their market share. The Dow Chemical Company is the largest player in the polymer emulsion market. The company serves various high-growth end-markets, offering an extensive product portfolio that includes all types of polymer emulsions. The company is backward integrated, offering waterborne resins, surfactants, binders, and other products. The company adopted both organic and inorganic strategies, including expansion and agreement between 2016 and 2019. For instance, in 2018, the company opened a regional sales center located in Toronto, Canada, to address the demand for Canadian customers. These strategies have helped the company to strengthen its position in the North American market. BASF SE is the second-largest player in the polymer emulsions market. The company offers a wide range of polymer emulsions as well as raw materials such as surfactants and binders which are used to manufacture polymer emulsion. In 2018, the company expanded its production facilities of Joncryl water-based emulsion at its Ludwigshafen site. This has strengthened the company’s position as one of the leading manufacturers of water-based resin as well as emulsion polymers products. Don’t miss out on business opportunities in Polymer Emulsion Market. Speak to our analyst and gain crucial industry insights that will help your business grow. BASF SE (Germany) and Dow Inc., (US) are Leading Players in the Polyurethane Additives Market8/6/2021  The polyurethane additives market size is projected to reach USD 4.5 billion by 2025 at a CAGR of 4.2% from 2020. The demand for polyurethane additives market is increasing, owing to the growing demand for innovative and cost-effective additives.

APAC is projected to be the fastest-growing market for polyurethane additives. The rising population, increased demand for automobiles, growing disposable income, rapid industrialization, and increased urbanization are driving the APAC polyurethane additives market. China is the largest market for polyurethane additives in the region. China is also a major producer and consumer of polyurethane additives in the region as it has a huge manufacturing base. Apart from China, India and South Korea are projected to grow at a decent rate during the forecast period. The increase in demand for polyurethane additives and the growing construction industry in the emerging economies, such as APAC and South America, are driving the market. The key players in the polyurethane additives market include Evonik Industries (Germany), BASF (Germany), Huntsman Corporation (US), Covestro (Germany), Dow Inc. (US), Lanxess AG (Germany), Albemarle Corporation (US), Tosoh Corporation (Japan), Momentive (US), BYK (US). The polyurethane additives market report analyzes the key growth strategies, such as expansion and new product launch, adopted by the leading market players between 2015 and 2020. To know about the assumptions considered for the study download the pdf brochure BASF SE (Germany) is among the key players in the polyurethane additive market. The company adopted the strategies of expansion to strengthen its competitiveness in the global polyurethane additives market. For instance, in April 2019, the Company has increased the production capacity of alkylethanolamines (AEOA) by 20% at its Verbund site in Ludwigshafen, Germany. This would increase the company’s global annual production capacity to more than 110,000 metric tons. The versatile AEOA is used for various applications, including for manufacturing of polyurethane additives. This strategy will help the company to serve its customers better. Dow Inc., (US) is one of the leading manufacturers of polyurethane additives. The company adopted new product launch as one of its key business strategies. For instance, in June 2020, the Company launched new silicone additives under the VORASURF brand namely, VORASURF RF 5374 Additive, VORASURF 5382 Additive, and VORASURF RF 5388 Additive. These additives are developed in order to support more sustainable polyurethane foams in the cold chain applications. This strategy has helped the company to expand its existing product portfolio. Don’t miss out on business opportunities in Polyurethane Additives Market. Speak to our analyst and gain crucial industry insights that will help your business grow. Compagnie de Saint-Gobain SA and AGC Inc. are Leading Players in the Insulating Glass Window Market8/6/2021  The insulating glass window market is projected to grow from USD 12.8 billion in 2020 to USD 16.2 billion by 2025, at a CAGR of 4.8% from 2020 to 2025. The major reasons for the growth of the insulating glass window market include the optimal energy saving performance of insulating glass windows, the growing construction industry in regions like the Middle East and Asia Pacific, and the rising demand for value added glass products. These factors are responsible for driving the demand for insulating glass window market.

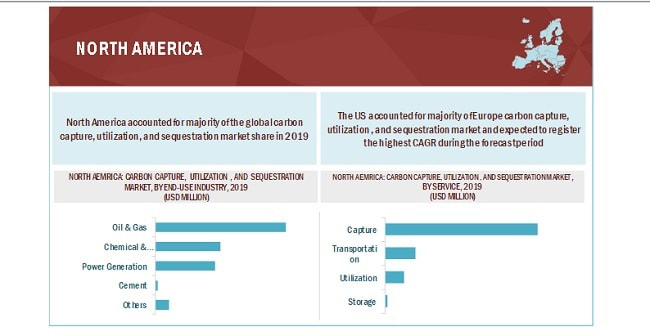

Asia Pacific is projected to be the fastest-growing market during the forecast period. Growing demand for insulating glass window due to the increasing investments in the commercial construction sector, as well as government initiatives that support the use of insulating glass windows in commercial buildings. Furthermore, the presence of leading insulating glass window manufacturers is expected to drive the insulating glass window market in the region. Compagnie de Saint-Gobain SA (France), AGC Inc. (Japan), Central Glass Co., Ltd. (Japan), Glaston Corporation (Finland), Guardian Glass (US), Internorm International GmbH (Austria), JE Berkowitz (JEB) (US), Nippon Sheet Glass Co. Ltd. (Japan), Viracon (US), H.B. Fuller (US), Henkel AG & Co. KGaA (Germany), Dymax Corporation (US), Sika AG (Switzerland), and The 3M Company (US). These are leading players in the insulating glass window market, globally. These players have adopted the strategies of new product launches, acquisitions, expansions, agreements, contracts, partnerships, investments, joint ventures, and divestments, to increase their presence in the global market. To know about the assumptions considered for the study download the pdf brochure Compagnie de Saint-Gobain SA is the leading player in the global insulating glass window market and is estimated to have the highest share in the market. In October 2019, Saint-Gobain Glass France, a subsidiary of Saint-Gobain, entered into several contracts with its waste collecting partners located in France. The purpose of this contract is to recycle glass from end-of-life windows to save energy and raw materials. Saint-Gobain Glass France’s waste collecting partners have committed to guaranteeing cullet quality compatible with that needed to manufacture new flat glass. The purpose of the contract is to reduce the procurement cost of raw glass materials, thereby minimizing the manufacturing costs of glass, either flat, insulated, or float glass. Another important player in the global insulating glass window market is AGC Inc. In October 2018, AGC Inc. entered into a partnership with Panasonic Corporation (Japan) to develop a vacuum insulated glass with the highest class of insulation performance for the European market. Total value of USD 11 million was invested in this development. The new vacuum insulated glass was launched in the European market by March 2019 for application in the residential sector of the region. The partnership would help AGC Inc. in catering to the growing need for soundly insulated residential replacement windows in Europe due to the common practice of homeowners renovating older houses to live in for several years or even decades. Don’t miss out on business opportunities in Insulating Glass Window Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  Carbon capture, utilization, and sequestration (also referred to as CCUS) is a process that involves capturing carbon dioxide (CO2), transporting it through pipelines, ships, and other modes of transport and storing it under the Earth’s surface to prevent CO2 emissions. This process is highly useful for curbing CO2 emissions, which lead to a better atmosphere. The growing need to reduce CO2 emissions from industrial and power plants drives the demand for CCUS system. The global carbon capture, utilization, and storage market size is expected to grow from USD 1.6 billion in 2020 to USD 3.5 billion by 2025, at a CAGR of 17.0% during the forecast period.

COVID-19 has merely put any effect on the market, which is expected to grow at a significant rate in 2020 as well, owing to continuous investment in the field of carbon capture and sequestration. Currently, CCUS is being largely used across natural gas processing plants and power generation plants. The operations of these plants were not affected by the COVID-19 pandemic; as a result, lockdown imposed due to the pandemic posed very minimal impact on the CCUS market. To know about the assumptions considered for the study download the pdf brochure North America is the largest carbon capture, utilization, and sequestration market owing to the presence of multiple large-scale CCS facilities in the US and Canada. Century plant, Shute Creek Plant, BPundaryy Dam, Petra Nova Plant, ENID Fertiliser plant are some few projects that are operational in eth US and Canada, The carbon capture, utilization, and storage market in North America is expected to be driven by rising environmental concerns in the region. Current operational projects in eth region include Boundary Dam (Canada), Petra Nova (US), Alberta Carbon Trunk Line (ACTL (Canada), and ENID Fertiliser plant (US), among others . Over the past years, companies have strengthened their position in the global carbon capture, utilization, and storage market by adopting expansions as a major strategy. From 2016 to 2019, the partnership was the key strategies adopted by the market players to maintain growth in the global carbon capture, utilization, and storage market. For instance, in May 2020, Royal Dutch Shell, together with Equinor ASA (Norway), and Total SE (France) have invested in the Northern Lights carbon capture and storage (CCS) project in Norway. With this investment of USD 682.3 million, the trio intends to set up a joint-venture company. This unique project opens for the decarbonization of industries with restricted opportunities for CO2 reductions. In November 2015, Flour Corporation signed a contract with Shell (US), wherein Flour corporation constructed Shell’s Quest Carbon Capture and Storage (CCS) project in Alberta, Canada. This project demonstrated Flour’s third-generation modular execution capabilities. The key players in the market include Fluor Corpoation (US), Royal Dutch Shell (Netherlands), Aker Solutions (Norway), Mitsubishi Heavy Industries, Ltd. (Japan), Linde PLC (UK), Hitachi, Ltd.(Japan), Exxon Mobil Corporation (US), JGC Holdings Corporation (Japan), Honeywell International, Inc. (US), Halliburton (US), and Schlumberger Limited (US) among others. COVID-19 has majorly affected the commercial sectors CCUS projects, such as cement plants, chemical plants, and others. Moreover, Upcoming carbon capture, utilization, and storage projects are expected to delay due to the outbreak of COVID – 19 pandemic. Don’t miss out on business opportunities in Carbon Capture, Utilization, and Storage Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The outbreak of COVID-19 has now spread across major APAC, European, and North American countries, affecting the market for impact modifiers since most global companies have headquarters in these regions. COVID-19 had disrupted the supply chain, which had slowed down market growth due to a lack of raw materials and unavailability of manpower. The lockdown in major countries due to this pandemic has also led to shutting down of the production facilities of plastic products.

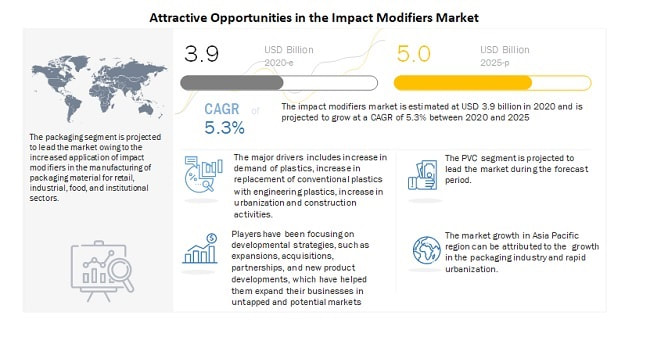

To know about the assumptions considered for the study download the pdf brochure In 2020, the global impact modifiers market size is estimated at USD 3.9 billion and projected to reach USD 5.0 billion by 2025, at a CAGR of 5.3% from 2020 to 2025. The major drivers for the market include an increase in demand for plastics, replacement of conventional plastics with engineering plastics, and urbanization & construction activities. However, the prohibition of PVC products across various end-use industries restrains the market growth. Moreover, the demand for plastics in packaging applications and the development of impact modifiers for bio-based polymers are expected to propel the market for impact modifiers. The impact modifiers market in the Asia Pacific region is projected to grow at the highest CAGR between 2020 and 2025. China, India, and Japan together accounted for the major share of the Asia Pacific impact modifiers market in 2019. Moreover, the Asia Pacific region is an emerging and lucrative market for impact modifiers, owing to industrial development and improving economic conditions. The presence of a number of plastic products manufacturing plants in China and rapid industrialization in Asia Pacific are expected to drive the impact modifiers market during the forecast period. Major companies such as Dow Inc. (US), Lanxess A.G. (Germany), Kaneka Corporation (Japan), Arkema S.A. (France), Mitsubishi Chemical Corporation (Japan), LG Chem Ltd. (South Korea), Shandong Ruifeng Chemical Co., Ltd. (China), Mitsui Chemicals, Inc. (Japan), Wacker Chemie AG (Germany), Formosa Plastics Corp. (Taiwan), Sundow Polymers Co., Ltd. (China), SI Group, Inc. (US), Akdeniz Kimya San. ve Tic. Inc. (Turkey), ), En-Door (China), Novista Group (China), and Indofil Industries Limited (India) and among others. Contact – Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: [email protected] Visit Our Website: https://www.marketsandmarkets.com/ |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed