The foam insulation market size was USD 17.58 Billion in 2016 and is projected to reach USD 22.39 Billion by 2021, at a CAGR of 4.95% from 2016 to 2021. The increasing demand for foam insulation from end-use industries, such as building & construction, transportation, and consumer appliances, is driving the foam insulation market.

Focus on the reduction of greenhouse gas emissions and strict government regulations on the construction of energy efficient buildings are expected to drive the demand for foam insulation. The major restraining factor for the market is the lack of awareness about the benefits of foam insulation. Download the PDF Brochure for more insight @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=166726706 Building & construction is the largest end-use industry for foam insulation By end-use industry, the building & construction segment is estimated to account for the largest share of the global foam insulation market in 2016, in terms of both value and volume. This end-use industry is projected to drive the foam insulation market from 2016 to 2021 due to the rising concern related to greenhouse gas emissions and the growing demand for net-zero energy buildings in countries like Germany, U.K., France, and U.S. The various building codes for new residential and commercial construction in countries such as U.S., U.K., Germany, China, Japan, and South Korea are also expected to drive the demand for foam insulation. Population growth and rapid urbanization in key countries, such as China and India, accompanied by the rising demand for consumer appliances have contributed to the growth of the foam insulation market in this region. Increasing investments in the region’s building & construction industry also help drive the demand for foam insulation. Besides, major market players, such as Covestro AG (Germany), BASF SE (Germany), Saint-Gobain (France), and Huntsman Corporation (U.S.), are setting up manufacturing plants in the Asia-Pacific region due to the availability of cheap labor and low production cost. To speak to our analyst for a discussion on the above findings, click Speak to Analyst

0 Comments

The high speed steels market is projected to grow from USD 2.13 Billion in 2016 to USD 2.77 Billion by 2021, at a CAGR of 5.3% from 2016 to 2021. The growing demand for high speed steels to manufacture various cutting tools, such as tool bits, drills, taps, gear cutters, saw blades, planers, jointer blades, milling cutters, router bits, punches, and dies, among others is driving the growth of the high speed steels market, globally.

The report “High Speed Steels Market by Product Type (Metal Cutting Tools, Cold Working Tools, Others), End-Use Industry (Automotive Industry, Plastic Industry, Aerospace Industry, Energy Sector, Others), Region – Global Forecasts to 2021″. Download the PDF Brochure for more insight @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=230635068 High speed steels are widely used in the automotive industry. Among end-use industries, the automotive industry segment is projected to lead the high speed steels market. In the automotive industry, high speed steels are used for manufacturing pumps, valves, injectors, turbochargers, inserts, pistons, valve needles, valve balls, and valve seats, among others. High speed steels based molds are used in the molding of plastics to form headlamps, tail lamps, and inner panels of automobiles. Growing automation in the automotive industry and rising demand for vehicles across the globe have boosted the demand for high speed steels in the automotive industry. Among product types, the metal cutting tools segment of the high speed steels market is projected to grow at the highest CAGR. The growth of this segment can be attributed to the fact that metal cutting tools made from high speed steels ensure effective manufacturing of critical and complex components with ease and utmost accuracy. The Asia-Pacific high speed steels market is projected to grow at the highest CAGR during the forecast period, 2016 to 2021. The region is a major consumer of high speed steels, which are used in varied end-use industries, such as automotive, plastic, and aerospace, among others. The demand for high speed steels is increasing in various countries, such as Japan, China, India, and South Korea, among others of the Asia-Pacific region. In order to meet this growing demand for high speed steels, top manufacturers of high speed steels from the U.S. and Europe are focusing on the Asia-Pacific region to expand their businesses. Hudson Tool Steel Corporation (U.S.), Sandvik Materials Technology AB (Sweden), Erasteel (France), Nachi-Fujikoshi Corporation (Japan), Daido Steel Co., Ltd. (Japan), Friedr. Lohmann GmbH (Germany), Kennametal Inc. (U.S.), Voestalpine AG (Austria), ArcelorMittal S.A. (Luxembourg), and ThyssenKrupp AG (Germany), among others, are the key companies operating in the high speed steels market. These players, with a wide market reach and established distribution networks, are investing increasingly in research & development activities for development of new grades of high speed steels. They also have strong technical and market development capabilities, which enable them to upgrade their existing products for new applications. To speak to our analyst for a discussion on the above findings, click Speak to Analyst  The Polyurethane Additives Market is projected to reach USD 2.75 billion by 2021, at a CAGR of 6.3%, in terms of value from 2016 to 2021. The polyurethane additives market is driven by increasing usage of polyurethane in the construction and automotive industries.The report includes analysis of the polyurethane additive market by region, namely, North America, Europe, Asia-Pacific, the Middle East & Africa, and South America.

Download the PDF Brochure for more insights @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=121317889 Building & construction expected to dominate the market for PU additive The building & construction industry is projected to drive the polyurethane additive market, aided by increased demand for insulation applications for maintaining optimum temperature and reducing the energy cost. Automotive is another end-use industry where polyurethane is being used for vehicle interiors as well as exteriors. The use of the polyurethane helps reduce the weight of vehicles and enhance fuel efficiency. Polyurethane additives are used mainly in flexible foam, rigid foam, coatings, adhesives & sealants, elastomers, and binders. Flexible foams are primarily used in bedding & furniture, and automotive & transportation industries. North America, Europe, Asia-Pacific, Middle East & Africa, and South America are considered the main regions in the polyurethane additives market report. Asia-Pacific region is dominant in the polyurethane additive market. The rising demand for polyurethane additives in this region is mainly driven by its increased use in building & construction industries. Europe is the second-largest consumer of polyurethane additives, globally. The market in this region is mainly driven by the growing opportunities from transportation and construction industries. The Middle East & Africa is the second fastest-growing market, due to the increased demand for rigid foam for insulation purposes in the region. Covestro AG (Germany), BASF SE (Germany), The Dow Chemical Company (U.S.), and Huntsman International LLC (U.S.) are the leading companies operating in this market. These companies are expected to account for a significant market share in the near future. Entering into related industries and targeting new markets will enable polyurethane additive manufacturers to overcome the effects of the volatile economy, leading to the diversified business portfolio and increase revenue. The other main manufacturers of polyurethane additives are Tosoh Corporation (Japan), Albemarle Corporation (U.S.), Eastman Chemical Company (U.S.), Kao Corporation(Japan) ), Evonik Industries AG (Germany), Air Products and Chemicals, Inc. (U.S.), and Momentive Performance Materials Inc. (U.S.).  The methyl ester ethoxylate market has grown at a moderate pace over the past five years owing to the increase in demand of methyl ester ethoxylate for industrial cleaning and domestic cleaning applications. Currently, the methyl ester ethoxylate market is dominated by various key players, such as Huntsman Corporation (U.S.), KLK OLEO (Malaysia), Lion Corporation (Japan), Ineos Group Limited (Switzerland), and Jet Technologies (Australia).

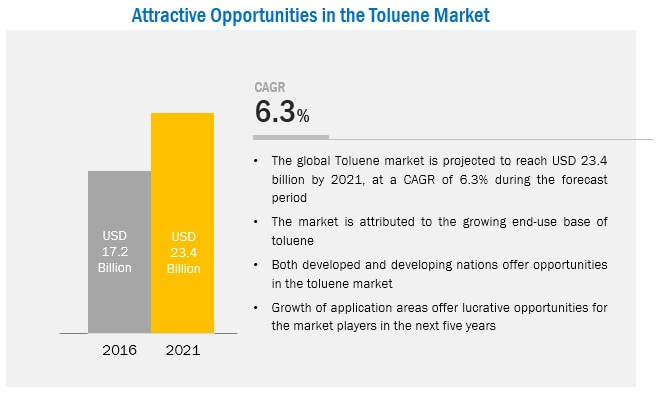

Download the PDF Brochure for more insight @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38024882 New product developments/launches were undertaken in the past few years by Lion Corporation. Other companies have not taken part in major developments in the methyl ester ethoxylate market; however, there is scope for developments as the demand for methyl ester ethoxylate is rising. New companies are also expected to enter this market. In February 2016, Lion Corporation introduced TOP SUPER NANOX, a super-concentrated liquid laundry detergent. Methyl ester ethoxylate and a lift out (LO) ingredient are its primary raw materials. This improved the position of the company in the concentrated liquid detergents segment. In February 2013, Lion Corporation introduced an improved version of TOP NANOX, a super-concentrated liquid laundry detergent used for removing grimes and sources of odor. This product has methyl ester ethoxylates as a raw material. It is the successor to TOP NANOX, a product introduced in 2010. Huntsman Corporation is one of the leading producers of methyl ester ethoxylates. It operates through five business segments, namely, polyurethanes, performance products, advanced materials, textile effects, and pigments & additives. It has more than 100 manufacturing and R&D facilities in over 30 countries. It is involved in producing eco-friendly surfactants made from oleochemicals derived from coconut, soybean, and palm oils. These products help the company reduce its carbon footprint. KLK OLEO is involved in developing renewable resources such as palm oil and its derivatives. It has vertical integration wherein it produces its own raw materials such as palm oil and has exclusive ownership and management of the entire supply chain. It has its own palm tree plantations and mills through which it produces and processes its raw materials. This makes it possible for the company to maintain the quality of its finished products and also have control over its feedstock supply. Related Reports: Methyl Ester Ethoxylates Market by Type (C16-C18 & C12-C14), Application (Domestic Cleaning, Industrial Cleaning, Personal Care & Others), and Region – Global Forecast to 2021  The global market size of toluene was USD 20.02 Billion in 2015 and is projected to reach USD 23.41 Billion by 2021, at a CAGR of 6.3%.

Rising end-use of toluene and its derivatives in industries such as, oil & gas, petrochemical, building & construction, paints, printing, rubber, and resins, among others are driving the market for toluene. Along with these, the growing petrochemical industry in the Asia-Pacific region countries such as, India, Taiwan, and Thailand is also driving the toluene market. Download the PDF Brochure for more insight @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1095 “Toluene Di-Isocyanate segment to be the fastest growing market for toluene” The TDI segment is estimated to be fastest growing segment in the toluene market. Growth in the automotive and building & construction industries is expected to drive the market of TDI for polyurethane, which is used as an insulating foam in these industries. North America is expected to witness high potential growth in the TDI segment due to the recent discoveries of shale gas and shale oil in the region and a strong manufacturing base in the U.S. Rising energy costs and greenhouse gas emissions have prompted various companies to improve the energy efficiency in households and industrial buildings, which is driving the demand for PU foams for use as insulators. PU foam is used in automobiles due to the light weight, which helps in the reduction of fuel emissions. With the increasing concerns regarding the conservation of energy, the market for PU is expected to grow, which, in turn, is expected drive the demand for toluene. The global toluene market has a large number of market players; however the market is led by some of the major players, such as, China Petroleum & Chemical Corporation (China), China National Petroleum Corporation (China), Exxon Mobil Corporation (U.S.), Covestro AG (Germany), BP P.L.C. (U.K.), SK Innovations (South Korea), BASF SE (Germany), GS Caltex (South Korea), Formosa Chemical & Fiber Corporation (Taiwan), Royal Dutch Shell (Netherlands), and CPC Corporation (Taiwan), among others. The Asia-Pacific region, with its growing economies and rapidly expanding commercial and industrial bases, is projected to lead the toluene market from 2016 to 2021, both, in terms of value and volume. The toluene market in Europe and North America is consolidated, whereas the market in the Asia-Pacific region has a fragmented structure, where China, Japan, India, and South Korea are the leading players. To speak to our analyst for a discussion on the above findings, click Speak to Analyst  The Compressor Rental Market is projected to reach USD 5.53 Billion by 2026, at a CAGR of 6.4% between 2016 and 2026.

Increasing demand for pneumatic tools in the construction and manufacturing end-use industries is fueling the growth of the compressor rental market. Even though, the mining equipment market was experiencing a lull over the past few years, it began to witness a positive trend, in terms of demand for mining equipment since 2015. Air compressors are best suited for heavy duty applications in mining operations. The revival of the mining equipment market is expected to have a positive impact on the growth of the compressor rental market during the forecast period. Download the PDF Brochure @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=23430927 Based on end-use industry, the construction segment led the compressor rental market The growth of the construction segment of the compressor rental market can be attributed to growth of various sectors, such as residential & commercial construction, infrastructure development, demolition & road building equipment, and civil engineering in the Asia-Pacific region. Compressors are considered to be the most efficient tools for bulk handling & lifting as well as drilling applications in the construction industry. Increased use of compressors in the construction industry is one of the driving factors for the compressor rental market. Technologically advanced air compressors are preferred as pneumatic power tools in commercial applications. They are used as jackhammers, pneumatic drills, pneumatic nail guns, and air saws, among others. Increasing demand for these pneumatic tools in the construction and manufacturing end-use industries is driving the demand for compressors, thereby fueling the growth of the compressor rental market. China is the largest market for compressor rental in the Asia-Pacific region, owing to the continuous growth of the chemical and mining industries in the country. Growth of the construction and general manufacturing industries in China is also projected to fuel the demand for compressor rental in the country, thereby contributing to the growth of the Asia-Pacific compressor rental market during the forecast period. Atlas Copco, Ingersoll Rand, Hertz Equipment Rental Corporation, and United Rentals, Inc., among others are the leading players operating in the compressor rental market. These leading players primarily concentrate on acquisitions to expand their geographical reach, globally. The competitiveness in the compressor rental market is increasing due to growing capacities of companies and increasing number of agreements taking place between them. Various strategic growth activities have been adopted by key players, such as Atlas Copco, Ingersoll Rand, and United Rentals, Inc., among others to strengthen their position in the compressor rental market. These market players are concentrating more on inorganic growth strategies than organic growth strategies. Expansions and new product launches are some of the key strategies adopted by these leading players to grow in the compressor rental market. To speak to our analyst for a discussion on the above findings, click Speak to Analyst  The market for modacrylic fiber is projected to grow from USD 621.9 Million in 2016 to USD 723.7 Million by 2021, at a CAGR of 3.08%.

This growth is due to the increasing applications of modacrylic fiber such as hair fiber, pile (synthetic/fake fur), and protective clothing. Industrial regulations and standardization regarding the safety of employees, also provide an opportunity for this market to grow. Request for sample report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=44304885 Market Dynamics Drivers

Increase in safety concerns in the household, industrial and transportation sectors have led to the standardization of materials that are being used. Countries in North America and Europe have stringent rules & regulations regarding the use of fire-resistant materials such as modacrylic fiber in household upholstery, airline interiors and for protective apparel for industrial workers and firefighters. These regulations and standards force the manufacturers to improve on the quality of the products being offered and also have a positive impact on their application in sectors such as industrial, defense & public safety as well as in household. Major Market Developments

On the basis of key regions, the modacrylic fiber market is segmented into, North America, Europe, Asia-Pacific, Middle East, and Africa, and South America. The Asia-Pacific region is a key market for modacrylic fiber. The development of the economies and rapid growth in the industrialization in this region are impacting the growth of this market. Increasing industrial regulations related to employee safety ensures that industries switch to protective clothing made from modacrylic fiber, thereby impacting the growth of the market. The following are the key players in the modacrylic fiber market:

Expansions, new product launches, and partnerships were the key strategies adopted by industry players to achieve growth in the epoxy adhesives market between 2012 and 2016. The increasing demand for light weight vehicles, wind energy, and the shift in the construction business towards the construction of multi-storied buildings which use epoxy adhesives in glazing and panels, is leading to the rise in demand. Companies have adopted strategies such as, new product launches, expansions, and mergers & acquisitions to fulfill the growing demand. Some of the key players, such as Henkel AG & Co., KGaA (Germany), Huntsman Corporation (U.S.), 3M Company (U.S.), Ashland Inc. (U.S.), Sika A.G. (Switzerland), The Dow Chemical Company (U.S.), Lord Corporation (U.S.), Illinois Tool Works Inc. (U.S.), and Permabond LLC (U.S.), have adopted these strategies to strengthen their businesses, globally.

Download the PDF Brochure for more insights @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=142980020 Henkel AG & Co. KGaA is a major player in the global epoxy adhesives market. The company’s wide range of business segments provides an added advantage to the company’s profit margin, which enables the company to compensate the loss from low performing business segments and invest in strategic expansions and R&D activities. The adhesive technology business segment of the company accounted for 50% of its total revenue in 2015. The company follows the capacity expansions strategy to support the growing demand, improve product cost competitiveness, and the product portfolio by investing in R&D activities in new applications to cater to the market. Recently in October 2016, the company launched Loctite EA 9452, a new high-performance 2-part epoxy adhesive. This product launch helped the company in entering into the filtration industry. 3M Company is another major player in the global epoxy adhesives market. North America accounted for 64% of the overall company revenue. The industrial and consumer business segment of the company manufactures adhesives & sealant products for various applications. These business segments together earned about 47% of its total revenue in 2015. The company’s business strategy mainly revolves around its targets for increasing its global footprint, increasing revenues, and launching innovative solutions through its products. As a part of its growth strategy, the company plans to establish new production facilities and expand its existing plant capacities which would enable the company to strengthen its position in the high growth epoxy adhesives market. In September 2012, 3M expanded its epoxy adhesives product line by adding the Scotch Weld EPX DP810, and DP110 products. These products provide long-term reliability for heavy-duty applications including aerospace, appliances, sporting goods, and electronics. Apart from the above mentioned market players, H.B. Fuller (U.S.), MasterBond (U.S.), Royal Adhesives & Sealants (U.S.), and Threebond Co. Ltd. (Japan), are the other important players in this market.  The global engineered foam market is projected to reach USD 122.30 billion by 2026, at a CAGR of 7.9% from 2016 to 2026. The growing demand for engineered foam from end-use industries has led to significant developments in the engineered foam market. Engineered foam has been increasingly used over general foams with enhanced features such as high strength & stiffness, uniform distribution of load, improved performance in extreme conditions, stability in corrosive environments, and others. Engineered foam is largely used in aerospace & defense, transportation, manufacturing & constructions, medical & healthcare, and other industries for insulations and cushioning applications. Polyurethane is the major material type used for making engineered foams, followed by polystyrene, polyvinyl chloride, and others. Engineered foams are available in three forms, namely, flexible form, rigid form, and spray forms. With increasing demand for customized materials for cushioning and insulation applications by various end-use industries, the engineered foam market is expected to grow at a significant pace during the forecast period.

Download PDF Brochure for more insight @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=171499038 Key players operating in the engineered foam market include BASF SE (Germany), The Dow Chemical Company (U.S.), Huntsman Corporation (U.S.), Bayer AG/Covestro (Germany), Seikisui Chemical Co., ltd (Japan), Trelleborg AB (Sweden), Inoac Corporation (Japan), Recticel NV/SA (Belgium), Vita (Lux III) S.A.R.L (U.K.), Armacell GmbH ( Luxembourg), Foamcraft, Inc. (U.S.), Foampartner group (Switzerland), Future Foam, Inc. (U.S.), FXI-Foam Innovations (U.S.), Rogers Corporation (U.S.), UFP Technologies, Inc. (U.S.), The Woodbridge Group (Canada), among others. Some of them are specialized foam manufacturers while others are raw material manufacturers with forward integration in some grades of foam manufacturing. Substantial investments for expansions, agreements, and new product launches have been made in the past few years by key companies such as Bayer AG, The Dow Chemical Company, Armacell GmbH, BASF SE, and Huntsman Corporation. Among these, Bayer AG is one of the most active players in the market with regards to adoption of growth strategies. It has expanded its business in different regions to increase its global reach and also to cater to its customers with prominent product launches. Bayer AG has been focusing on new product launches and also is expanding its business in new geographies. This has helped the company expand its global footprint and tap the critically advantageous geographic regions that are witnessing rapid growth in the engineered foam market. BASF SE and The Dow Chemical Company have also outperformed other companies in the number of developments. The companies have actively been involved in new product launches through high R&D investments. In September 2013, BASF built the Polyurethane Systems House, in which polyurethane raw materials are blended to deliver customized products, including products for medical applications. Customized raw material would further help the company manufacture quality foam products. Armacell GmbH is another company specialized in production of engineered foams and is focused on organic as well as inorganic growth strategies. The company has made several acquisitions in Europe and Americas region in the past few years to increase its market share in the subsequent areas. In October 2016, the company acquired 100% of the shares of PoliPex Ltda. (PoliPex), a leading Brazilian manufacturer of extruded polyethylene (PE) insulation foams. This will increase the product portfolio of Armacell GmbH into polyethylene foams. The company also made some new product launches that includes Armaflex Ultima, a blue elastomeric foam based flexible insulation material. The launch aims to gain fire class BL-s1, d0 (tubes) stages respectively for B-s2, d0 (sheets). This launch helped the company diversify product portfolio. The global engineered foam market is a competitive market, with key players adopting various growth strategies to expand their shares in the global engineered foam market.  The global microcellular polyurethane foam market is dominated by few key players such as BASF SE (Germany), The Dow Chemical Company (U.S.), Huntsman Corporation (U.S.), Rogers Corporation (U.S.), and Evonik Industries (Germany, among others. These companies are considered as leaders in the rapidly evolving market.

Download the PDF Brochure for more insight @https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=232217217 Substantial investments have been made in the past few years by key companies such as BASF SE (Germany), The Dow Chemical Company (U.S.), and Rogers Corporation (U.S.) to address the future demand of microcellular polyurethane foam arising from the growing end use industries. Key players operating in the market are majorly focused on acquisitions and expansions for capacity expansion of existing facilities and installation of new facilities to achieve better performance qualities, economies of scale, product innovation, and to simultaneously address the increasing demand of microcellular polyurethane foam. BASF SE made investments in its existing facility at Pudong site, which was established in 2011. The new investment project included the expansion of the Cellasto Asia Pacific Technical Center, the establishment of three new production lines, and the technical improvement of existing facilities. The production capacity was estimated to double after the project’s completion in 2015. Expansions and acquisitions are the key growth strategies adopted by the major players in the recent past. For instance, Rogers Corporation acquired a custom molding machine from PolyWorks Corporation (North Smithfield, Rhode Island) and a license to utilize PolyWorks’ technology for the molding of Poron formulations. This manufacturing facility was installed in Rogers-’ Suzhou, China manufacturing campus by mid-2011 in order to serve its global customers. Apart from expansions and acquisitions, companies also made investments in the global market. This strategy accounted for 17% of the share out of the total developments in the microcellular polyurethane foam market between 2010 and 2015. BASF built the world’s biggest single-train production plant for TDI in Europe. The plant has an annual capacity of 300,000 metric tons. The total investment including the precursor is over USD 1.23 billion. The TDI plant is located at Ludwigshafen site, Germany. TDI (toluene diisocyanate) is a key component for the polyurethane industry. A large proportion of it is used in the automotive industry for items, such as seat upholstery and interior linings, and in the furniture industry for flexible foams in mattresses & upholstery and wood coatings. Related Reports: Microcellular Polyurethane Foam Market by Type (Low Density Foam, High Density Foam), Application (Automotive, Building & Construction, Electronics, Medical, Aerospace, Others), Region (North America, Europe, APAC, MEA, RoW) – Global Forecast to 2021 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed