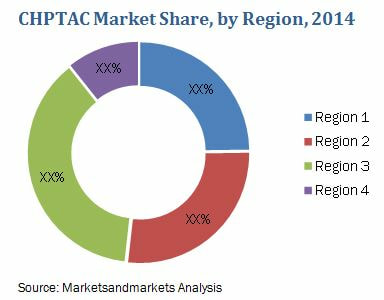

Increased use of paper and paper products with the increasing modernization and industrialization drives the paper industry in Asia-Pacific, making it an attractive market for CHPTAC. China’s paper industry drives the market for CHPTAC in the country with China being the largest market. Asia-Pacific is the fastest-growing market for CHPTAC, followed by Europe and North America which are growing at almost the same pace. The U.S., Thailand, and China are the world’s largest markets for CHPTAC in various end-use industries which include paper, water treatment, oil & gas, etc. Moreover, China and India are projected to be the fastest-growing economies between 2015 and 2020. The U.S. accounted for largest share of the CHPTAC market for starch modification. The U.S. is one of the largest producers of corn and maize for which it is one of the key producers of modified starch, which makes it the largest market for CHPTAC.

Ask for free sample pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=268263224 The paper industry in the developed and developing counties offers growth opportunities. Supported by favorable growth in a number of end-use industries with small shares in the personal care, textile, dye, chemicals, nutraceuticals, and cosmetics of CHPTAC, the overall CHPTAC market remains attractive during the forecast period. The top countries in terms of demand of CHPTAC are U.S., Thailand, China, and the Netherlands, among others. The market for CHPTAC (3-chloro-2-hydroxypropyl)trimethylammonium chloride is growing at an average pace, with Asia-Pacific leading in terms of demand, followed by Europe and North America. The CHPTAC industry is segmented by its end-use industries which include paper, textile, water treatment, oil & gas, and others (personal care, dye, nutraceuticals, cosmetics, and chemicals). The paper industry accounts for the maximum share of CHPTAC produced globally. In terms of volume, the CHPTAC market is projected to register a CAGR of 3.3% between 2015 and 2020. The fastest-growing application of CHPTAC is projected to register a growth rate of 3.7% during the forecast period. This report follows both top-down and bottom-up approaches to estimate and forecast the CHPTAC market by volume and value. This report focuses on the CHPTAC market by its end-use industry and region. Download PDF to Know More @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=268263224

0 Comments

The report “Anionic Surfactants Market by Type (LAS, Lignosulfonates, AES/FAS, Alkyl Sulfates/Ether Sulfates, Sarcosinates, Alpha Olefin Sulfonates, Phosphate Esters), Application (Home Care, Personal Care, Oil & Gas, Construction), and Region – Global Forecast to 2022″, The global anionic surfactants market is estimated at USD 16.36 Billion in 2017 and is projected to reach USD 20.10 Billion by 2022, at a CAGR of 4.2%. Anionic surfactants are widely used in cleaning and related products such as detergents, soaps, cleaners, shampoos, and hand washes. These are among the largest application areas of surfactants due to which anionic surfactants account for the majority of share of the overall surfactants market. The rising number of applications in home care, personal care, oil & gas, construction, textiles, agriculture, and food processing industries is driving the anionic surfactants market. The growing demand for detergents and cosmetics is also driving the market.

Ask for free sample reports @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=239519688 Browse 90 market data Tables and 28 Figures spread through 124 Pages and in-depth TOC on “Anionic Surfactants Market “ Home care application accounted for the largest share in 2017. The home care segment is projected to be the largest market for anionic surfactants from 2017 to 2022, owing to the rapid growth of the chemical industry in Asia Pacific. Factors such as rising disposable incomes, rising living standards, flexible government taxation policies, rapid technological advancements in products, and product offerings by major international and domestic players at competitive prices are few of the major factors driving the market for chemicals. This, in turn, is driving the anionic surfactants market in the home care application. Lignosulfonates is expected to be the fastest-growing segment in the anionic surfactants market. Lignosulfonates are widely used in the construction industry as a concrete additive. The construction industry is witnessing high growth in almost all the regions such as the Middle East and Asia Pacific, especially in countries such as China, India, the UAE, and Saudi Arabia, among others. The growth in the housing and infrastructure sectors (hotels, stadium, and restaurants) in Asia Pacific is contributing to the demand for lignosulfonates in the region. Download PDF brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=239519688 Asia Pacific was the largest anionic surfactants market in 2017. In Asia Pacific, China was the largest market for anionic surfactants in 2017, wherein the market is driven by demand from industries such as home care, personal care, oil & gas, construction, and textiles, among others. The market players are undertaking various technological developments and expansions to meet the increasing demand and enhance profit margins. The market in this region has promising growth potential owing to the availability of low-cost raw materials. The presence of vast manufacturing industry, which includes textiles, paints, oil & gas, chemicals, cosmetics, and detergents, is also expected to drive the market in the region. The global anionic surfactants market has a large number of market players; however, the market is led by some major players, such as AkzoNobel (Netherlands), BASF (Germany), Clariant (Switzerland), DowDuPont (US), Evonik (Germany), Croda International (US), Stepan Company (US), Huntsman (US), Kao Corporation (Japan), and Galaxy Surfactants (India), among others. Don’t miss out on business opportunities in Anionic Surfactants Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The report “Aroma Ingredients Market for Personal Care Industry by Type (Synthetic Ingredients, Natural Ingredients), Application (Fine Fragrances, Toiletries, and Cosmetics), and Region (APAC, Europe, North America) – Global Forecast to 2023″, The aroma ingredients market is projected to grow from USD 2.27 billion in 2018 to USD 2.83 billion by 2023, at a CAGR of 4.5% between 2018 and 2023. The increasing demand for personal care products, coupled with the change in lifestyles and consumer preferences is expected to drive the growth of the aroma ingredients market during the forecast period.

Ask free sample reports @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=113835443 Browse 64 market data Tables and 41 Figures spread through 110 Pages and in-depth TOC on “Aroma Ingredients Market” Based on type, the synthetic ingredients segment of the aroma ingredients market is projected to grow at the highest CAGR, in terms of value from 2018 to 2023 Based on type, the aroma ingredients market has been segmented into synthetic ingredients and natural ingredients. The synthetic ingredients segment of the market is projected to grow at the highest CAGR in terms of value during the forecast period. Synthetic ingredients are compounds artificially made through chemical reactions. They have characteristic odors as per their molecular structures. These are synthesized using various artificial chemicals primarily derived from coal tar and petroleum. Synthetic ingredients are less costly as well as consistent in quality and price, unlike natural ingredients. Hence the synthetic ingredients are the fastest-growing type of aroma ingredients. Based on application, the fine fragrances segment is projected to lead the aroma ingredients market during the forecast period in terms of value The fine fragrances segment is projected to lead the aroma ingredients market in terms of, value between 2018 and 2023. Fine fragrance is a term used for products diluted with alcohol and contain a high concentration of aroma ingredients. Fine fragrances include major applications, such as perfumes, colognes, body mists, and deodorants. Aroma ingredients are the key compounds in fine fragrance formulations. The increasing demand for perfumes, colognes, deodorants, and body mists across the globe is expected to drive the demand for aroma ingredients in the fine fragrances application. Download PDF to know more @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=113835443 The European region is expected to be the largest market for aroma ingredients during the forecast period The aroma ingredients market has been studied for 5 regions, namely, APAC, North America, Europe, the Middle East & Africa, and South America. The European region is projected to be the largest market for aroma ingredients during the forecast period due to the strong foothold of manufacturers of personal care products in the region. Aroma ingredients are the key compounds used in the formulation of various personal care products. The European region is also home for the leading manufacturers of aroma ingredients. The major countries driving the growth of the aroma ingredients market in the European region are France, Germany, Italy, and UK. Some of the key players in the aroma ingredients market include Symrise (Germany), Takasago International Corporation (Japan), Sensient Technologies Corporation (US), MANE (France), Robertet SA (France), T. Hasegawa Co., Ltd. (Japan), Frutarom (Israel), Givaudan (Switzerland), Firmenich SA (Switzerland), and International Flavors & Fragrances Inc. (US). Don’t miss out on business opportunities in Aroma Ingredients Market. Speak to our analyst and gain crucial industry insights that will help your business grow. Leading players deploying multiple strategies to strengthen their position in engineered foam market5/9/2019  The global engineered foam market is projected to reach USD 122.30 billion by 2026, at a CAGR of 7.9% from 2016 to 2026. The growing demand for engineered foam from end-use industries has led to significant developments in the engineered foam market. Engineered foam has been increasingly used over general foams with enhanced features such as high strength & stiffness, uniform distribution of load, improved performance in extreme conditions, stability in corrosive environments, and others. Engineered foam is largely used in aerospace & defense, transportation, manufacturing & constructions, medical & healthcare, and other industries for insulations and cushioning applications.

Ask for Free Sample Reports @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=27777113 Polyurethane is the major material type used for making engineered foams, followed by polystyrene, polyvinyl chloride, and others. Engineered foams are available in three forms, namely, flexible form, rigid form, and spray forms. With increasing demand for customized materials for cushioning and insulation applications by various end-use industries, the engineered foam market is expected to grow at a significant pace during the forecast period. Key players operating in the engineered foam market include BASF SE (Germany), The Dow Chemical Company (U.S.), Huntsman Corporation (U.S.), Bayer AG/Covestro (Germany), Seikisui Chemical Co., ltd (Japan), Trelleborg AB (Sweden), Inoac Corporation (Japan), Recticel NV/SA (Belgium), Vita (Lux III) S.A.R.L (U.K.), Armacell GmbH ( Luxembourg), Foamcraft, Inc. (U.S.), Foampartner group (Switzerland), Future Foam, Inc. (U.S.), FXI-Foam Innovations (U.S.), Rogers Corporation (U.S.), UFP Technologies, Inc. (U.S.), The Woodbridge Group (Canada), among others. Some of them are specialized foam manufacturers while others are raw material manufacturers with forward integration in some grades of foam manufacturing. Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=27777113 Substantial investments for expansions, agreements, and new product launches have been made in the past few years by key companies such as Bayer AG, The Dow Chemical Company, Armacell GmbH, BASF SE, and Huntsman Corporation. Among these, Bayer AG is one of the most active players in the market with regards to adoption of growth strategies. It has expanded its business in different regions to increase its global reach and also to cater to its customers with prominent product launches. Bayer AG has been focusing on new product launches and also is expanding its business in new geographies. This has helped the company expand its global footprint and tap the critically advantageous geographic regions that are witnessing rapid growth in the engineered foam market. BASF SE and The Dow Chemical Company have also outperformed other companies in the number of developments. The companies have actively been involved in new product launches through high R&D investments. In September 2013, BASF built the Polyurethane Systems House, in which polyurethane raw materials are blended to deliver customized products, including products for medical applications. Customized raw material would further help the company manufacture quality foam products. Armacell GmbH is another company specialized in production of engineered foams and is focused on organic as well as inorganic growth strategies. The company has made several acquisitions in Europe and Americas region in the past few years to increase its market share in the subsequent areas. In October 2016, the company acquired 100% of the shares of PoliPex Ltda. (PoliPex), a leading Brazilian manufacturer of extruded polyethylene (PE) insulation foams. This will increase the product portfolio of Armacell GmbH into polyethylene foams. The company also made some new product launches that includes Armaflex Ultima, a blue elastomeric foam based flexible insulation material. The launch aims to gain fire class BL-s1, d0 (tubes) stages respectively for B-s2, d0 (sheets). This launch helped the company diversify product portfolio. The global engineered foam market is a competitive market, with key players adopting various growth strategies to expand their shares in the global engineered foam market. Don’t miss out on business opportunities in Epoxidized Soybean Oil Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The report “Compressor Rental Market by Compressor Type (Reciprocating, Rotary Screw), End-Use Industry (Construction, Mining, Oil & Gas, Power, Manufacturing), Region (North America, Europe, Asia-Pacific, Middle East & Africa, South America) – Global Forecast to 2026″, The compressor rental market is projected to reach USD 5.53 Billion by 2026, at a CAGR of 6.4% from 2016 to 2026.

Browse 81 market data tables and 48 figures spread through 139 pages and in-depth TOC on “Compressor Rental Market” Ask for Free Sample Pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=23430927 Increasing demand for pneumatic tools in the construction and manufacturing end-use industries is fueling the growth of the compressor rental market. Even though, the mining equipment market was experiencing a lull over the past few years, it began to witness a positive trend, in terms of demand for mining equipment since 2015. Air compressors are best suited for heavy duty applications in mining operations. The revival of the mining equipment market is expected to have a positive impact on the growth of the compressor rental market during the forecast period. Among end-use industries, the chemical segment of the compressor rental market is projected to grow at the highest CAGR from 2016 to 2026. In the chemical industry, air compressors are used for transporting liquids under pressure. They are also used in pressurizing tanks, aeration tanks, and culture vessels for spot cooling and molding plastics. Air compressors find application in the automatic control systems used in the chemical industry. Besides air compressors, screw compressors are also commonly used in the chemical industry. Rapid growth of the chemical industry in the Middle East & Africa and Asia-Pacific regions is fueling the growth of compressor rental market. Download PDF brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=23430927 Based on compressor type, the rotary screw segment of the compressor rental market is projected to grow at the highest CAGR from 2016 to 2026. On basis of compressor type, the rotary screw segment accounted for the largest share of the compressor rental market in 2015. This segment is projected to grow at the highest CAGR during the forecast period, 2016 to 2026. Rotary screw compressors are being increasingly used as power tools in the construction industry. In the oil & gas industry, rotary screw compressors are used in oil rigs to extract crude oil. Growth of the construction and oil & gas industries has resulted in growth of the rotary screw compressor type segment of compressor rental market. The compressor rental market in the Asia-Pacific region is expected to grow at the highest CAGR between 2016 and 2026. The Asia-Pacific compressor rental market is projected to grow at the highest CAGR between 2016 and 2026. Growing industrialization and infrastructure development in the Asia-Pacific region offers numerous opportunities for use of air compressors. The key driver for the growth the Asia-Pacific compressor rental market is the rising demand for compressors from the construction industry. Key players, such as Atlas Copco, Ingersoll Rand, and United Rentals, Inc., among others have been focusing on the strategy of mergers & acquisitions to expand their presence in the compressor rental market. Don’t miss out on business opportunities in Compressor Rental Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The market size of waste heat recovery (WHR) system was USD 44.14 billion in 2015 and is projected to reach USD 65.87 billion by 2021, at a CAGR of 6.90% between 2016 and 2021. The major players adopted key strategies such as supply contract and agreements to increase their market share and revenue. Other major growth strategies adopted by WHRS manufacturers are acquisitions and partnership & collaboration that help the company strengthen their position in the WHR system market.

Ask for free sample reports @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=202657867 Major players operating in the WHR system market are ABB Ltd. (Switzerland), Amec Foster Wheeler (U.K.), Ormat Technologies Inc. (U.S.), General Electric Co. (U.S.), Mitsubishi Heavy Industries Ltd. (Japan), Echogen Power Systems Inc. (U.S.), Econotherm Ltd. (U.K.), Thermax Limited (India), Siemens AG (Germany), and Cool Energy Inc. (Colorado). Ormat Technologies Inc. (U.S.) is one of the leading WHR system manufacturers, globally. The company has been focusing on supply contracts to maintain its leading position in the market. For instance, in November 2014, Ormat Technologies secured a contract of USD22.3 million from Utah Associated Municipal Power Systems (U.S.) for engineering, procurement, and construction at the Kern River Gas Transmission Company’s Veyo natural gas compressor station in southern Utah. This contract included installation of air-cooled Ormat Energy Converter, which will generate power using the recovered heat. Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=202657867 Amec Foster Wheeler (U.K.) is another major player in the WHR system market. The company has been focusing on supply contracts as part of its strategic development activities. In April 2016, Amec Foster Wheeler secured a contract from Cleco Corporation (U.S.) to design and supply a complete 50 MWe power island in Louisiana, US. This waste heat generated from the production of carbon black, used in items such as tires and industrial rubber products will be used to produce steam, which will in turn create electricity that can be sold and sent to the grid. This contract included supplying the power plant’s major equipment, including steam turbine generator, WHR steam generator, feedwater heater, condenser, deaerator, pumps, and cooling tower. This report provides a detailed analysis of the WHR system market and segments the same on the basis application, end-use industry, and region. Based on application, the market has been segmented into preheating, steam & electricity generation, and others. Based on end-use industry, the market has been segmented as petroleum refining, metal production, cement, chemical, paper & pulp, and others. Based on region, the market has been segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. Don’t miss out on business opportunities in Waste Heat Recovery System Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The 3D PA (polyamide) market consisting of PA11 and PA12 is forecasted based on two scenarios as its growth is primarily based on the adoption of 3D printing technology by end-use industries. Scenario one represents comparatively normal growth whereas scenario two projects exponential growth.

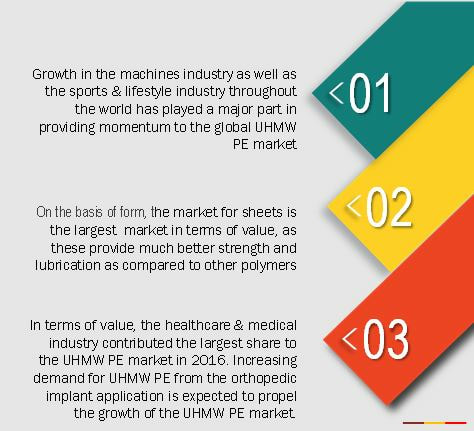

Ask for Free Sample Pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=150620564 The PA11 and PA12 market in 3D printing is an emerging market with a significant number of global and regional players. This market is dominated by a few players in North America and Europe region. PA12 has a large number of developed grades for 3D printing in comparison to PA11, which is an evolving market. EOS GmbH (Germany), Arkema SA (France), 3D Systems (U.S.), Stratasys (U.S.), and Evonik AG (Germany) are the major manufacturers of PA11 and PA12 grades. Arkema SA and Evonik AG has its own supply base whereas the other companies mentioned above modify the basic grades of PA 11 and PA 12. These players have been focusing on organic as well as inorganic growth with special focus on the Asia-Pacific market. Agreements, collaborations, expansions, investments, and new product launches are some of the key strategies adopted by market players to achieve growth in the 3D printing market. The expiry of major laser sintering patents in 2014 has helped many players to enter into 3D printing market Substantial investments have been made in the past few years by key companies such as EOS GmbH (Germany), 3D systems (U.S.), Stratasys (U.S.), Arkema SA (France) and others in the form of new facilities, joint ventures, collaborations, and others. Arkema SA (France) has been instrumental in promoting PA11 for which it is a major supplier as an unfilled powder for 3D printing as well as to the intermediaries which modify the grades according to the end user requirements. EOS GmbH (Germany) has developed a large number of grades of PA11 and PA 12 to support its laser sintering systems business. Recently, the company launched PA1102, PA2241FR, PA1101, Prime part plus, and others to increase its product portfolio. 3D Systems (U.S.) recently launched ProX GF/AF/ EX and others. The company acquired CRDM Ltd., a U.K.-based firm in August 2013, which has materials, such as polyamide, polyurethane resins, stainless steel, cobalt chrome, and ABS. The acquisition helped 3D Systems to add the stated materials to its portfolio along with the market share of the company in Europe. Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=150620564 Arkema SA (France) and Evonik AG (Germany) have been the key suppliers of PA11 and PA12 bio-based and specialty polyamides. Arkema SA has made some key strategic partnerships with castor oil suppliers, such as Jayant Agro and others in the Asia-Pacific region. Evonik AG has been instrumental in the supply of PA12 directly as 3D printing unfilled powder or to the intermediaries, which is primarily used in 3D printing technology by laser sintering. Apart from these, many players from China has emerged in the scene to supply primarily unfilled grades of PA12. Apart from new product launches and expansions, companies operating in this market have also been focusing on mergers & acquisitions which together accounted for around 30% of the total new developments in the polyamide market between 2012 and 2015.  The report “Ultra-High Molecular Weight Polyethylene Market by Form (Sheets, Rods & Tubes), End-Use Industry (Aerospace, Defense, & Shipping, Healthcare & Medical, Mechanical Equipment), Region – Global Forecast to 2021″, The Ultra-High Molecular Weight Polyethylene (UHMW PE) market is projected to reach USD 2.16 Billion by 2021, at a CAGR of 9.9% from 2016 to 2021. This growth is mainly attributed to the increasing demand for UHMW PE from the healthcare & medical industry worldwide due to its properties such as self-lubrication, biocompatibility, and impact resistance.

Browse 102 market data tables and 83 figures spread through 177 pages and in-depth TOC on “Ultra-High Molecular Weight Polyethylene Market” Ask for Free Sample Pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=257883188 Sheets segment estimated to lead the UHMW PE market in 2016 By form, the sheets segment is estimated to account for a major share of the UHMW PE market in 2016. This large share is mainly attributed to the extensive use of sheets in the aerospace, defense, & shipping industries for the manufacture of aircraft interiors & mechanical equipment industries for the manufacture of conveyer belts. Rods & tubes are the second most used form of UHMW PE used majorly in the mechanical equipment industry. Healthcare & medical end-use industry segment expected to lead the UHMW PE market by 2021 By end-use industry, the healthcare & medical segment is estimated to account for a major share of the UHMW PE market in 2016. In the healthcare & medical industry, there is a high demand for UHMW PE for the manufacture of orthopedic implants and parts for medical devices due to properties such as high strength to weight ratio, self-lubrication, and impact resistance. The growing demand for orthopedic implants from developed countries is expected to fuel the growth of the UHMW PE market globally. Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=257883188 The North American region is expected to lead the global UHMW PE market during the forecast period By region, North America is estimated to account for the largest share of the global UHMW PE market in 2016, and the U.S. is estimated to account for the largest market share in 2016. The growing aerospace, defense & shipping, and healthcare & medical industry in the North American region is driving the demand for UHMW PE. Braskem S.A. (Brazil), Celanese Corporation (U.S.), LyondellBasell Industries N.V. (Netherlands), Koninklijke DSM N.V. (Netherlands), Asahi Kasei Corporation (Japan), Mitsui Chemicals, Inc. (Japan), Quadrant Engineering Plastic Products AG (Switzerland), E. I. Du Pont De Nemours and Company (U.S.), Honeywell International, Inc. (U.S.), Toyobo Co., Limited (Japan), and Rochling Engineering Plastics SE & Co. KG (Germany) are some of the key players in the global UHMW PE market. Don’t miss out on business opportunities in Ultra-High Molecular Weight Polyethylene Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The report “Glass Filled Nylon Market by Type (Polyamide 6, Polyamide 66),End Use Industry(Automotive, Electrical & Electronics, Industrial), Manufacturing Process(Injection Molding, Extrusion Molding), Glass Filling and Region Global Forecast to 2024″ The glass filled nylon market size is estimated to grow from USD 8.2 billion in 2019 to USD 10.8 billion by 2024, at a CAGR of 5.8% during the forecast period. The glass filled nylon market is witnessing significant growth because of the growing demand from industries such as industrial, automotive, and electrical & electronics. Glass filled nylon provides various superior properties such as high strength, dimensional stability, high creep resistance, and chemical resistance.

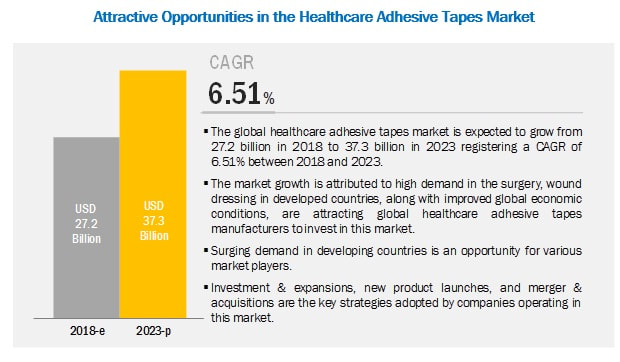

Browse 90 market data Tables and 50 Figures spread through 121 Pages and in-depth TOC on “Glass Filled Nylon Market” Ask for Sample pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=25070558 The automotive end-use segment accounted for the largest share of the glass filled nylon market in 2019. Automotive is an important end-use industry segment of the glass filled nylon market. Glass filled nylon is an ideal solution for vehicle weight reduction. It is fast replacing metal parts in the automotive industry due to the ease of mass production as well as ease in molding it. Polyamides are also cheaper in unit cost in comparison to metals, which make them an economic alternative. Glass filled nylon is used in applications such as automotive engine covers, parts inside the engine compartment, and under the bonnet of cars. Polyamide 6 is the most widely used glass filled nylon. Polyamide 6 is the most widely used polymer in the making of glass filled nylon. In terms of value and volume, polyamide 6 is the most widely used glass filled nylon due to its easy availability and low price. It also offers superior properties such as good tensile strength, high mechanical strength, and chemical resistance. These properties make polyamide 6 based glass filled nylon suitable for various applications in the automotive and electrical & electronics industries. APAC is expected to be the largest market for glass filled nylon during the forecast period. APAC is the largest glass filled nylon market, in terms of value and volume. China, India, and Japan are the fast-growing economies that contribute to the growth of the market in the region. The booming electrical & electronics and industrial sectors are also bolstering the glass filled nylon market in APAC. China is one of the prominent consumers of glass filled nylon in APAC. The country has become the single-largest consumer of glass filled nylon in the electrical & electronics industry, which is expected to strengthen its position further. Major players in the glass filled nylon market include BASF SE (Germany), Asahi Kasei Corporation (Japan), Lanxess (Germany), DowDuPont Inc. (US), Royal DSM N.V. (Netherlands), Ensinger GmbH (Germany), Arkema (France), SABIC (Saudi Arabia), Evonik (Germany), and Ascend Performance Materials (US). Don’t miss out on business opportunities in Glass Filled Nylon Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The report “Healthcare Adhesive Tapes Market by Resin (Acrylic, Rubber, Silicone), Backing Material (Paper, Fabric, Plastic), Application (Surgery, Hygiene, Wound Dressing, Secure Iv Lines, Ostomy Seal, Splint, Bandages, Diagnostic), and Region – Forecast to 2023″ The healthcare adhesive tapes market is projected to grow from USD 27.2 billion in 2018 to USD 37.3 billion by 2023, at a CAGR of 6.51% during the forecast period. The major factor driving the healthcare adhesive tapes market includes the increase in demand for surgeries, wound dressings, hygiene, transdermal drug delivery, and many others, owing to their advantages in many medical applications. These adhesive tapes have wide acceptability due to factors such as low cost and easy availability, as compared to traditional medical procedures.

Browse 93 market data Tables and 43 Figures spread through 155 Pages and in-depth TOC on “Healthcare Adhesive Tapes Market” Ask for free Sample pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=175119477 Acrylic is estimated to be the largest resin segment in the healthcare adhesive tapes market during the forecast period. The acrylic segment is expected to account for the largest market share during the forecast period because of its better adhesion properties to a variety of substrates. Acrylic adhesive tapes are designed with high or low tack and high or low peel strength. These tapes are permeable to moisture that is measured by the moisture vapor transmission rate (MVTR). Acrylic healthcare adhesive tapes release off from body or skin without leaving adhesive residue. These tapes are preferred for stick-to-skin application because of the breathable nature compared to rubber adhesive tapes. Fabric to account the largest share as a backing material in the healthcare adhesive tapes market during the forecast period. The fabric is the most popular backing material used in the manufacturing of healthcare adhesive tapes. Fabric healthcare adhesive tapes are high in demand as they have high strength, toughness, good abrasion, and heat resistance, low creep at elevated temperatures, good chemical resistance, and excellent dimensional stability. Owing to its strength, these tapes are used for securing dressings, catheters, tubing, and wound dressing and for other medical purposes. Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=175119477 North America to account for the largest share of the healthcare adhesive tapes market during the forecast period. Various factors have contributed to the growth of the North American healthcare adhesive tapes market. These factors include the rising incidence of chronic wounds, increase in the number of elderly citizens, increasing patient awareness on wound care, aging population, and technological advancements in the healthcare industry. The surgical adhesive tapes application has witnessed steady growth along with an increase in orthopedic and trauma, neurosurgery, cardiovascular, and gastroenterology. The increasing number of orthopedic procedures in the US is driving the demand for bandages and healthcare adhesive tapes. Major vendors in the healthcare adhesive tapes market include 3M (US), Cardinal Health, Inc. (US), Nitto Denko Corporation (Japan), Johnson & Johnson Services, Inc. (US), PAUL HARTMANN AG (Germany), Avery Dennison Corporation (US), NICHIBAN Co., Ltd. (Japan), Smith & Nephew (UK), Lohmann GmbH & Co.KG (Germany), Scapa Group Plc (US), Medline Industries Inc. (US), and Essity Aktiebolag (PUBL) (Sweden). Don’t miss out on business opportunities in Healthcare Adhesive Tapes Market. Speak to our analyst and gain crucial industry insights that will help your business grow. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed