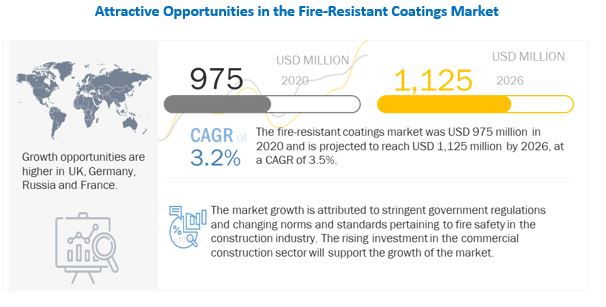

The global fire-resistant coatings market size is projected to grow from USD 975 million in 2020 and is projected to reach USD 1,125 million by 2026, at a CAGR of 3.5%. Europe accounted for the largest share of the market. It is projected to reach USD 490 million by 2026, at a CAGR of 3.0%, between 2021 and 2026. The growing building & construction sector in the region is projected to drive the market.

To know about the assumptions considered for the study download the pdf brochure The increasing number of fire accidents, which result in injuries, loss of life, and damage to property, has led to the implementation of various codes, regulations, and standards for fire safety and fire protection. In this regard, Europe and North America have the highest number of safety codes and regulations as compared to other regions.In the US, the International Code Council (ICC) and the National Fire Protection Association (NFPA) had recommended several standards and norms pertaining to fire safety and protection in buildings, infrastructure, and industrial sector. In the UK and Germany, under British standard 476 and ETA & DIN 4102 standard, several regulations were imposed related to fire safety and standard in building construction steelwork. In Russia, Federal Law No. 123-03 and GOST R 53295-2009 were imposed in July 2008, wherein technical regulation related to fire safety in building and construction activities was mandated to ensure safety and protection from fire accidents. The implementation of stringent regulations and norms is driving the demand for fire-resistant coatings, as newly constructed buildings and processing plants need to meet the required safety and fire resistance standards. Considering the growth opportunities, market players are focusing on developing new and innovative products that comply with the stringent safety and fire protection standards. Thus, as a preventive measure, governments, builders, and construction industries are using fire-resistant coatings to ensure the utmost safety at housing, commercial, institutional, and industrial places. These factors are thereby supporting market growth. Europe projected to account for the largest share of the fire-resistant coatings market during the forecast period. Europe accounted for the largest share of the global fire-resistant coatings market in 2019. The growth of the fire-resistant coatings market in this region is mainly attributed to stringent government regulations, an industrial initiative for sustainable development, and a strong emphasis on protection against fire. Moreover, the practice of constructing green buildings and adopting green coatings offers many opportunities for the growth of the market in the region. The European market is mainly dominated by the EU-5 countries, especially Germany and the UK. The leading players in the fire-resistant coatings market include AkzoNobel (Netherlands), PPG (US), Jotun (Norway), Sherwin-Williams (US), and Hempel (Denmark). The key industry players are adopting strategies to expand their presence and enhance their product portfolio through investments in R&D. For example, in 2017, Hempel invested in an R&D center solely for fire-resistant coatings in Spain. This expansion will help the company comply with the ever-changing demand from the construction industry and develop high efficacy products. Read More: https://www.marketsandmarkets.com/Market-Reports/fire-resistant-coating-market-95861153.html

0 Comments

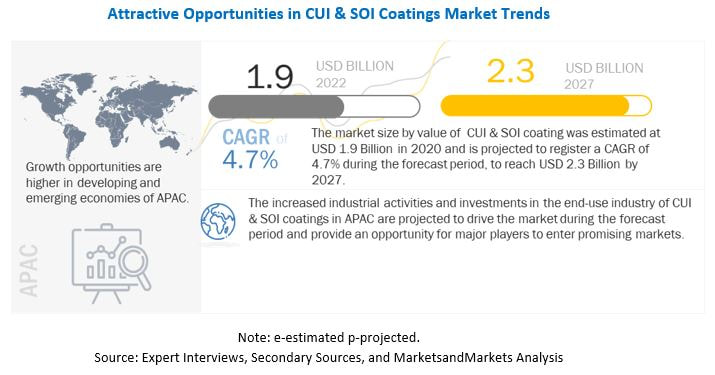

Top Market Leader - Corrosion Under Insulation (CUI) & Spray-on Insulation (SOI) Coatings Market5/12/2022  The global CUI & SOI coatings market size is projected to grow from USD 1.9 billion in 2022 to USD 2.3 billion by 2027, at a CAGR of 4.7% during the forecast period. The growing demand for CUI & SOI coatings from end-use industries, such as marine; oil & gas, and petrochemical; energy & power; and others, drives the CUI & SOI coatings market. Demand for these coatings is encouraged by many companies to formulate various developmental strategies in the CUI & SOI coatings market to increase their footprint in the growing market. The companies have adopted various strategies, such as investment, expansion, partnership, collaboration, and new product development to increase their global presence and maintain sustained growth in the CUI & SOI coatings market.

CUI & SOI coatings find major applications in marine; oil & gas, and petrochemical; energy & power, etc. The oil & gas, and petrochemical industry accounted for the major share of the CUI & SOI coatings market in 2021. The major share is due to the high volumes of CUI & SOI coatings used in the oil & gas & petrochemical industry. The oil fields development in the South China Sea and the growing investments in the oil & gas industry in China, Japan, Indonesia, India, and other countries are projected to drive the demand for CUI & SOI coatings. To know about the assumptions considered for the study download the pdf brochure The CUI & SOI coatings market in the Asia Pacific is projected to register a higher CAGR, in terms of value, between 2022 and 2027. The growth in the region is ascribed to the growing oil & gas, and petrochemical; marine; energy & power industries. The rapid growth of emerging economies in the region makes Asia Pacific an alluring market for CUI & SOI coatings manufacturers. There are various players operating in the CUI & SOI coatings market. The major market players include Akzo Nobel N.V. (Netherlands), PPG Industries, Inc., (US), Jotun A/S (Norway), The Sherwin-Williams Company (US), Hempel A/S (Denmark), Kansai Paint Co., Ltd (Japan), Nippon Paint Co., Ltd. (Japan), and RPM International Inc (US). The developmental strategies adopted by major players are partnership & collaboration, new product launches, investments, and expansion to increase share in the market. Akzo Nobel accounted for the major share in the global CUI & SOI coatings market. The company operates in different segments such as decorative paints, performance coatings, and specialty chemicals. The company has its presence in many countries in Europe, North America, APAC, South America, and the Middle East. The company carries out its business activities in 80+ countries across the globe. It has a strong product portfolio. Also, there are 548 offices and manufacturing sites across the world. The company focuses on various organic and inorganic strategies to increase its global presence. It has leveraged its strong financial background and distribution network to expand its business across Europe and various countries across the globe. This will drive the growth of the company and also its CUI & SOI coatings business, globally.

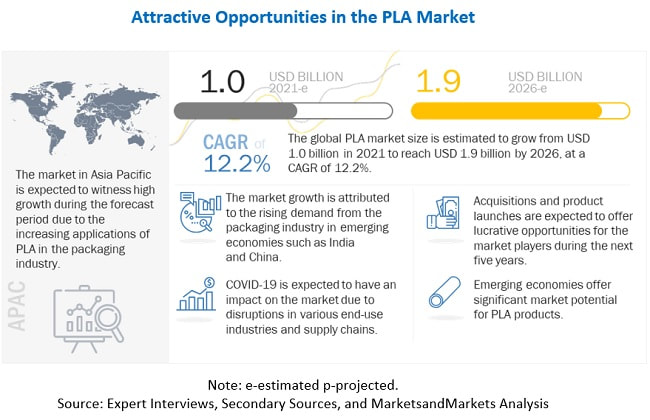

The global PLA market size is projected to grow from USD 1.0 billion in 2021 to USD 1.9 billion by 2026, at a CAGR of 12.2% between 2021 and 2026. The major factors driving the market are rising demand of PLA in packaging industry, stringent waste management regulations in Europe, increased focus of government on green procurement policies, and shift in consumer preference toward eco-friendly and biodegradable plastic products. Moreover, development of new applications, high potential in emerging countries of APAC, and multi-functionalities of PLA is expected to drive the market during the forecast period.

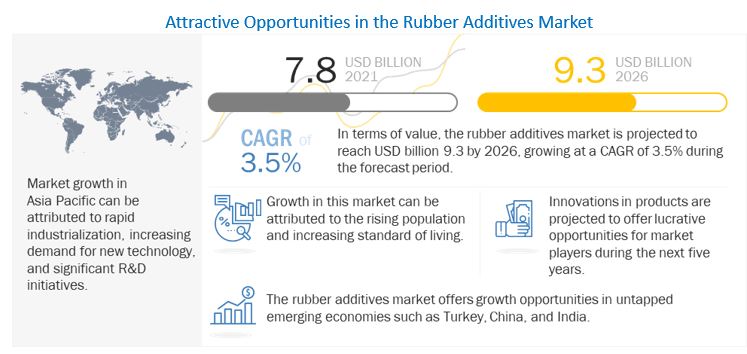

Improving consumer awareness regarding sustainable plastic solutions and increasing efforts to eliminate the use of non-biodegradable conventional plastics contribute to the market growth of PLA. Traditionally used petroleum-based plastics take decades to break down or degrade and lay in landfills for a long period. PLA breaks down faster when they are discarded and are absorbed back into the natural system. In addition, the rate of decomposition of biodegradable plastics by the activities of microorganisms is much faster than that of traditional plastics. To know about the assumptions considered for the study download the pdf brochure The packaging segment is estimated to be the fastest-growing end-use industry for PLA market during the forecast period. Packaging is the largest end-use industry for PLA, with a high CAGR of 13.0% during the forecast period. The need for sustainable solutions has encompassed several industry verticals, including food & beverages, e-commerce, and FMCG. The unique properties of packaging enable its use in various food and non-food applications such as cigarettes, biscuits, sugar confectioneries, baked goods, noodles, and other snacks. The rise in e-commerce has also increased packaging requirements. The thermoforming grade segment is expected to lead the PLA market during the forecast period. Thermoforming grade has enormous growth potential in various packaging applications such as food, beverages, and other consumer products. Thermoformed parts made of PLA have excellent clarity, comparable to those formed in oriented polystyrene (OPS) and polyethylene terephthalate (PET). This, combined with the temperature requirements for product storage, make thermoformed PLA suitable for food packaging trays for baked goods, fruits, and vegetables. Europe is expected to be the largest market for PLA during the forecast period. The packaging industry is the largest end-use industry of PLA in Europe. The political and economic conditions have also driven the market penetration of PLA. The EU Commission has focused on the Lead Markets Initiative, where PLA has been identified as one of the most important potential markets. The strict government norms and economic conditions have also driven the PLA market. These factors have been responsible for the development of PLA with collaborative research in the region. The key players in this market are Natureworks LLC (US), Total Corbion PLA (Netherlands), BASFSE (Germany), Cofco (China), Futerro (Belgium), Danimer Scientific (US), Toray Industries Inc. (Japan), Evonik Industries (Germany), Mitsubishi Chemical Corporation (Japan), and Unitika Ltd. (Japan). Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=29418964 Rubber Additives Market Opportunities: Adoption of green technology and high-performance rubbers5/6/2022  The rubber additives market is projected to reach USD 9.3 billion by 2026, at a CAGR of 3.5% from USD 7.8 billion in 2021. Rubber is a polymer, which is primarily categorized as natural and synthetic rubber. Natural rubber is obtained from certain trees that are found particularly in the tropical areas. On the other hand, synthetic rubber is obtained by the by-products of petroleum refining. To meet the specific requirements of end-use industries, the rubber has to be treated with chemicals to give it the desired properties. Thus, rubber additives are used to improve properties of the rubber. Rubber is processed using various additives to make it suitable to be used for various applications such as automobile, rubber mats, conveyor belts, and others.

To know about the assumptions considered for the study download the pdf brochure According to the report of IARC (International Agency on Research for Cancer), rubber manufacturing industry has proven to be a great contributor towards air pollution. This industry basically adds unwanted latex vapours into the air during the process of heating and forming latex sheets. Hence, manufacturers, with the help of green chemistry, are developing methods for the utilization of safer chemicals which can be easily disposed of. The notable techniques include dry vacuuming is used to prevent the spreading of spilled chemicals; the recycling of wastewater must be done. Other techniques are chemical recovery methods like pyrolysis, devulcanization, and the production of reclaimed rubber. Tire is estimated to be the largest application of rubber additives market in 2020. Rubber is the primary raw material used in the production of tires. Several additives are used to attain the desired properties of rubber. Rubber additives are used in tires to provide specific characteristics such as high friction for racing tires and high mileage for passenger car tires. The growing automotive industry in Asia-Pacific demands processed tires to meet the demand of the customers. The stringent environmental norms in Europe demand the use of high-tech rubber for various applications. Therefore, rubber is processed using additives to attain the desired properties of heat resistance, friction, mechanical stress, and others. The rising global motor vehicle production is the key factor driving the market for rubber additives. Asia Pacific is expected to be the largest rubber additives market during the forecast period, in terms of value. Asia Pacific is the fastest-growing region in rubber additives market owing to rapid economic growth in the region. The increased demand for superior quality processed rubber from the automotive industry is driving the market for rubber additives in the region. The growing population coupled with the increasing purchasing power of consumers is boosting the demand for automobiles in the region. This in turn drives the market for rubber additives as they are required to enhance the properties of rubber which is used to manufacture automotive tires. The key market players profiled in the report Arkema S.A.(France), Lanxess AG (Germany), BASF SE (Germany), Solvay S.A. (Belgium), Sinopec Corporation (China), R.T. Vanderbilt Holding Company, Inc. (US), Emery Oleochemicals (US), Behn Meyer Group (Germany), Toray Industries, Inc. (Japan), and Sumitomo Chemical (Japan). They have adopted strategies such as and new product launch, acquisition, and collaboration in order to gain an advantage over their competitors Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=258971862 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed