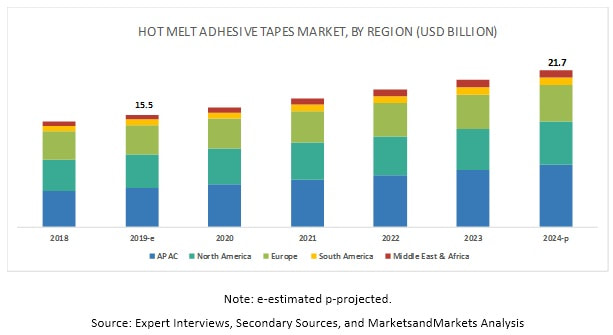

The hot melt adhesive tapes market is projected to grow from USD 15.5 billion in 2019 to USD 21.7 billion by 2024, at a CAGR of 7.0%, between 2019 and 2024. APAC is the largest consumer of hot melt adhesive tapes. The global hot melt adhesive tapes market is witnessing high growth on account of increasing applications, technological advancements, and growing demand in the APAC region.

The key players operating in the market are the 3M Company (US), Nitto Denko Corporation (Japan), tesa SE (Germany), Avery Dennison Corporation (US), and Intertape Polymer Group Inc. (Canada). These players have adopted various strategies, such as merger & acquisition, investment & expansion, and new product launch, to grow in the market. Mergers & acquisition was the key strategy adopted by the major players, between 2015 and 2019, to enhance their market shares and expand their global presence. To know about the assumptions considered for the study download the pdf brochure Avery Dennison Corporation (US) is one of the major companies in the global hot melt adhesive tapes market. The company achieved this position after several successful small and big acquisitions and expansion activities. The acquisition of Mactac’s European business, a leading manufacturer of high-quality, pressure-sensitive materials, catering to several high-value segments, including graphics, specialty labels, and industrial tapes, in 2016, was the major acquisition of the company. The acquisition enhanced the company’s competitiveness in the hot melt adhesive tapes market in Europe. Intertape Polymer Group (Canada), which was founded in 1991, is a leading player in hot melt adhesive tapes market. The company develops, manufactures, and supplies a variety of paper and film-based pressure-sensitive and water-activated tapes, polyolefin films, woven fabrics, and complementary packaging systems for industrial and retail applications. The company offers products for aerospace, automotive, and industrial applications. It has operations in 17 locations, including 12 manufacturing facilities in North America and 1 in Europe. The company, with its products, caters to a number of countries, including Canada, Germany, and the US. After acquiring all the assets of Canadian Technical Tape Ltd., Intertape will be able to improve its distribution channel and add value to its products.

0 Comments

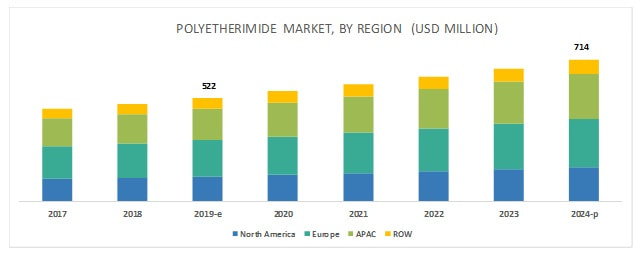

The Polyetherimide (PEI) Market size is estimated to grow from USD 522 million in 2019 to USD 714 million by 2024, at a CAGR of 6.5% between 2019 and 2024. The increasing demand from the transportation sector, electrification of vehicles, and replacement of metals and specialty polymers with PEI in heat resistance applications are expected to drive the market.

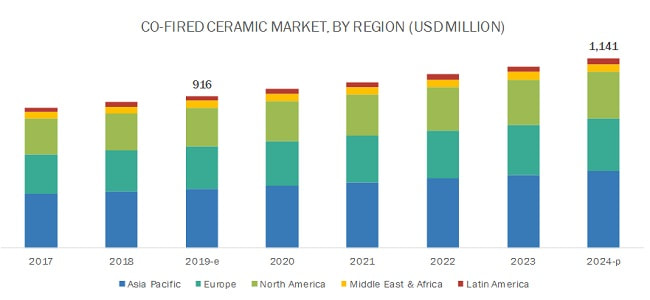

Download the PDF brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=264439177 Injection molding is projected to be the fastest-growing process type segment of the PEI market. PEI is used in applications such as medical and electronics due to its strength and rigidity. This amber, high-performance polymer also provides properties such as dimensional stability and chemical resistance. PEI is ideal for environments that include hot air and water, as it is hydrolytically stable, can be resistant to heat for an extended period, and has excellent electrical properties. PEI processed through injection molding is used in applications such as medical devices, instrument trays, and electrical enclosures. PEI sheet is projected to be the fastest-growing form. It is resistant to UV radiation even in unreinforced grade and offers properties such as high dielectric constant, making it an excellent electrical insulator. The general application of PEI sheet includes electrical switchgear, connectors, microwave cookware, under bonnet components, non-combustible plenum connectors, jet engine components, printed wiring boards, aircraft interiors, and electrical hardware components. The transportation end-use industry is the fastest-growing segment of the polyetherimide (PEI) market. In terms of volume, the transportation end-use industry is estimated to lead the PEI market, while the electrical & electronics segment is estimated to account for the second-largest share of the global polyetherimide (PEI) market. The use of PEI has been increasing due to its ability to replace metal and other thermosets and bulk molding compounds. PEI is apt for applications that require high heat resistance, strength, and chemical resistance. The largest application of PEI is in the electrical and lighting systems, followed by under-the-hood applications. “Europe to account for the largest share in the PEI market during the forecast period.” The key countries contributing to the growth of the PEI market in Europe are Germany, France, the UK, Italy, and Spain. Favorable government policies are expected to provide growth opportunities for R&D in the electronics & semiconductor and automotive industries in these countries. The growth in R&D investment in the region is mainly driven by the automotive, information and communications technology (ICT), and healthcare industries, which is expected to boost the demand for PEI in the region.  The use of co-fired ceramic is increasing due to its useful properties such as excellent physical, chemical inactivity, hermicity, and high thermal stability. The LTCC market and HTCC market size is estimated to be USD 916 million in 2019 and is expected to reach USD 1.1 billion by 2024, at a CAGR of 4.5% between 2019 and 2024. The increasing use of co-fired ceramic in the automotive, telecommunications, and aerospace & defense is bolstering the market growth, globally.

Download the PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=126252032 Based on material used, the market for co-fired ceramic is segmented as glass-ceramic and ceramic. Glass-ceramic material type dominated the overall LTCC market and HTCC market in 2018, in terms of volume & value both. This is due to the high demand for glass-ceramic material used in LTCC process for automotive, telecommunications, aerospace & defense applications. In the automotive industry, it is primarily used to make advanced wireless technology such as Bluetooth, used in high radio frequencies. In the telecommunications sector, co-fired ceramics are used in mobiles, play stations, and high radio frequency data transfer. The co-fired ceramic is divided into five end-use industries, such as automotive, telecommunications, aerospace & defense, medical, and others. The automotive end-use industry is expected to witness the highest growth in the coming years. The demand for excellent mechanical properties such as excellent physical, chemical inactivity, hermicity, and high thermal stability is expected to boost the market for co-fired ceramic in various end-use industries. The Asia Pacific is one of the leading LTCC market and HTCC markets. The growing demand from the aerospace & defense, automotive, and telecommunications sectors is driving the market in the region. The Asia Pacific region has the presence of co-fired ceramic manufacturers and telecommunications component manufacturers. China accounted for a significant share of the global LTCC market and HTCC market and is expected to register substantial growth during the forecast period. The increasing wireless devices production and introduction of 5G across all electronic end-users are expected to drive the demand for co-fired ceramic in China.  The natural fragrance market size is projected to reach USD 4.3 billion by 2024 from USD 2.7 billion in 2019, at a CAGR of 9.6% between 2019 and 2024. Rising growth in the personal care & cosmetic industry and growing demand for natural & organic products are driving the demand for natural fragrance market. High production and R&D costs, as well as compliance with quality and regulatory standards, are restraining the growth of the natural fragrance market. On the other hand, a significant change in the lifestyle of consumers towards natural products over synthetic ones drives the demand for natural fragrances. The players in the natural fragrance market are mainly concentrating on expansions, new product launches, and acquisitions to meet the growing demand in various applications. New product launches help companies strengthen their product portfolio and meet the specific requirements of customers.

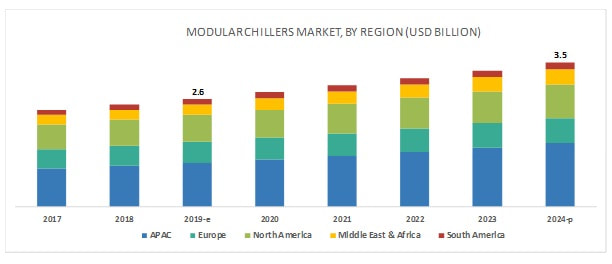

The growth of the natural fragrance market has been influenced mainly by expansions, new product launches, and acquisitions that took place between 2016 and 2019. Givaudan SA (Switzerland), Firmenich SA (Switzerland), International Flavors & Fragrances (US), Symrise AG (Germany), Takasago International Corporation (Japan) adopted expansions, new product launches, and acquisitions to remain competitive in the natural fragrance market. To know about the assumptions considered for the study download the pdf brochure Givaudan (Switzerland) is the largest player in the natural fragrance market. The company is developing its natural fragrance business by acquisition and expanding in countries such as APAC and North America. The company mainly focuses on expansions and acquisition to strengthen its position in the market. The company acquired Albert Vieille, a French company specialized in natural ingredients used in the fragrance and aromatherapy markets. It will help the company cater to the growing demand of customers for natural fragrances. As an expansion strategy, the company opened a new fragrance creative center in Mexico City, Mexico, in October 2017. The new center will help the company support its business growth in North America. Firmenich SA (Switzerland)is one of the major manufacturers of fragrances. In March 2016, the company opened a manufacturing facility in Buenos Aires, Argentina. The expansion has helped the company strengthen its position in the fragrances market in Argentina. In July 2018, Agilex Fragrances, which is a part of Firmenich group, acquired Fragrance West (US). This acquisition will help the company strengthen its position in the fragrances market in the Americas.  The modular chillers market size is estimated to be USD 2.6 billion in 2019 and projected to reach USD 3.5 billion by 2024, at a CAGR of 6.0%, between 2019 and 2024. Modular chillers is mainly used in the commercial, industrial, and residential applications for air conditioning, space cooling, and process cooling. They are energy efficient, compact, and easy to maintain as compared to their substitutes. The growing number of commercial construction projects are also expected to drive the modular chillers market.

The key players in the modular chillers market are Carrier Corporation (US), McQuay Air-Conditioning Ltd., (Hong Kong), Johnson Controls- Hitachi Air Conditioning (Japan), Midea Group (China), Ingersoll Rand (Ireland), Gree Electric Appliances, Inc. (China), Frigel Firenze S.p.A. (Italy), Mitsubishi Electric Corporation (Japan), Multistack, LLC. (US), and Haier Group (China). Acquisition is the key growth strategy adopted by the key modular chillers manufacturers. Apart from acquisition, manufacturers have adopted expansion, joint venture, and new product launch between 2015 and 2019. To know about the assumptions considered for the study download the pdf brochure Ingersoll Rand (Ireland) is among the key players in the modular chillers market. It is specialized in the manufacturing of HVAC systems through its established brand ‘Trane’. It has a strong foothold across the North American region, contributing around 70.0% of group’s revenue. The company has adopted organic and inorganic strategies to increase its market share and revenue. For example, in 2017, it acquired several channel points, such as distributors and independent dealers to expand the distribution network across the region. Gree Electric Appliances (China) is an international air conditioning company. It has a presence across emerging economies, and thus expected to provide growth opportunities to the company in the near future. It is a renowned brand in the HVAC market, which was ranked 385 on the list of Forbes Global 2000 companies, in 2018. It has a strong focus on R&D, having 52 research centres and 570 labs and applied for 15,600 patents including 5,000 innovation patents. The company is adopting growth through the innovation strategy to maintain its leading position in the market. Carrier Corporation (US) is the leading manufacturer and supplier of HVAC solutions. The company owns more than 80 brands, such as Carrier, Chubb, Kidde, and Edwards in the HVAC market. In 2018, the company registered an organic sales growth of 6.0%, majorly driven by the residential and commercial HVAC markets. It has an established joint venture in China with another leading HVAC company, ‘Midea’. This strategic joint venture is expected to expand the company’s footprints in the neighboring countries of China in the APAC region. This overall scenario is expected to create significant revenue opportunities for the company. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed