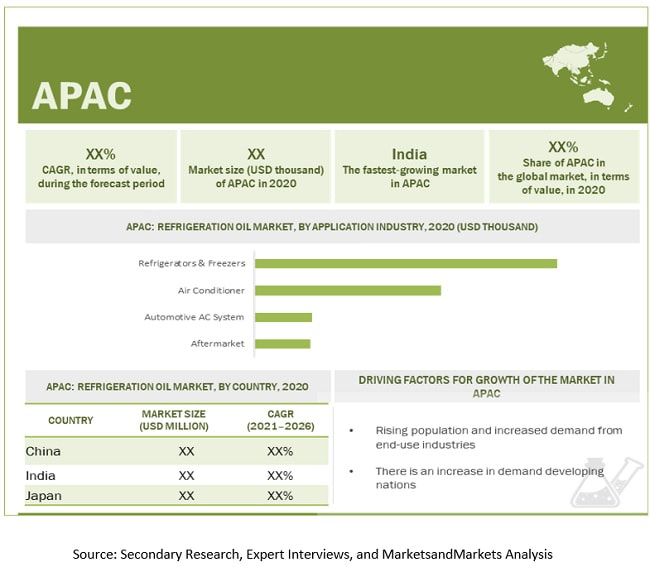

The refrigeration oil market size is projected to reach USD 1.4 billion by 2026 from USD 1.1 billion in 2021, at a CAGR of 4.1%. This growth is primarily triggered by the increasing demand from the refrigerator & freezer, air conditioner, and automotive AC system applications. APAC is the largest refrigeration oil market due to a rise in the manufacturing of consumer appliances and automobiles. Furthermore, the changing lifestyle of consumer and rising income levels have led to higher demand for refrigerators & freezers and air conditioners, which, in turn, drives the refrigeration oil market. The growing demand for perishable food products along with growth in the pharmaceutical industry also drives the demand for refrigerators & freezers, fueling the growth of the refrigeration oil market.

To know about the assumptions considered for the study download the pdf brochure APAC is an emerging market for the refrigeration oil market, and it is mainly attributed to high economic growth rate, followed by heavy investment across industries such as oil & gas, automotive, infrastructure, chemical, and electronics among others. With economic contraction and saturation in the European and North American markets, the demand is shifting to the APAC region. Refrigeration oil manufacturers are targeting this region as it is the strongest regional market for various applications, such as automotive, electronics and home appliances among others. The advantage of shifting production to the Asian region is that the cost of production is low here. Also, it is easier to serve the local emerging market. Key Market Players The key market players profiled in the report include as Eneos Holdings Inc. (Japan), BASF SE (Germany), Idemitsu Kosan Co. Ltd (Japan), ExxonMobil Corporation (U.S.), Royal Dutch Shell Plc. (Netherlands), Total Energies SE(France), China Petrochemical Corporation (Sinopec Corp), Petroliam Nasional Berhad(Petronas), FUCHS Petrolub SE (Germany), Johnson Controls(Ireland). Eneos Holdings Inc. is one of the world’s leading manufacturers and innovators of petroleum, natural gas, and metals. . The company operates through four business segments, namely, Energy, Metals, Oil, Natural gas E&P, and Others. . The company operates through four business segments, namely, Energy, Metals, Oil, Natural gas E&P, and Others. The company operates its refrigeration oil business in Japan, China, and other among other countries. BASF SE is one of the largest chemical producers in the world. It engages in manufacturing and selling a wide range of chemicals and intermediate solutions. The BASF Group comprises subsidiaries and joint ventures in more than 80 countries and operates six integrated production sites and 390 other production sites in Europe, Asia, Australia, America, and Africa. BASF has customers in over 200 countries and supplies products to a wide variety of industries. The company has a presence in more than 60 countries of Europe, North America, APAC, South America, and the Middle East & Africa. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=126068118

0 Comments

Corrosion protection coatings such as CUI & SOI coating are used for the protection of pipelines, equipment, reactors, and storage tanks in oil & gas and industrial sectors. These industries involve the use of hazardous and corrosive chemicals and processes that involve high temperatures and high heat. Also, this equipment is exposed to various climatic conditions which affect the reactor surface. The use of heavy-duty corrosion protection coatings in these areas may prevent or reduce the impact on the reactor surfaces. This results in the extended working life of the equipment.

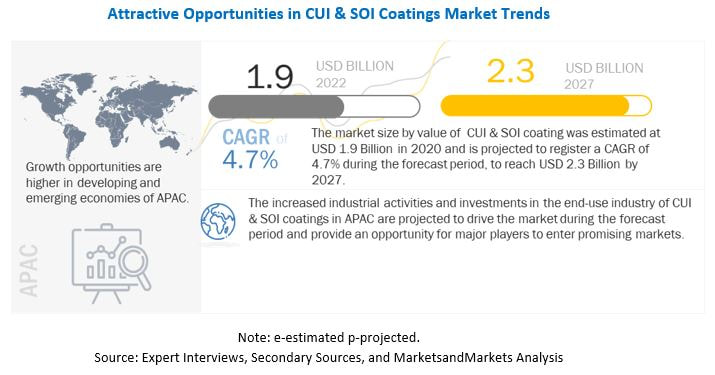

Due to the competitive market, industries are in the process of cost reduction. Use of heavy-duty corrosion protection coatings for providing insulation results in reduced operating costs. The global CUI & SOI coatings market size is projected to grow from USD 1.9 billion in 2022 to USD 2.3 billion by 2027, at a CAGR of 4.7%. Worldwide, corrosion under insulation (CUI) causes huge economic losses in many industries. It also gradually weakens structures posing a threat to property and life. CUI & SOI coating is one of the most effective and economical solutions for tackling corrosion. They obstruct the surface and the corrosion agent and extend the life of the structure as well as enhance efficiency. To know about the assumptions considered for the study download the pdf brochure The different types of CUI & SOI coatings are epoxy, acrylic, silicone, and others. Epoxy is a major type of CUI & SOI coatings, which accounted for the largest share. This is mainly attributed to excellent protection from CUI, water resistance, and widespread applications of epoxy-based CUI coatings. In addition, epoxy-based CUI & SOI coatings can be used in multi-component coatings with other types. The market for CUI & SOI coatings in APAC is projected to register significant growth, and this trend is projected to continue during the forecast period. Asia Pacific is the fastest-growing CUI & SOI coatings market globally. This is attributed to economic growth, followed by large investments in various industries such as petrochemical, oil & gas, marine, energy & power, and others. APAC is the most lucrative market and should be the same in the near future. APAC is the center of foreign investments and booming manufacturing sectors due to the low-cost labor and inexpensive availability of land. The rise in demand for CUI & SOI coatings can be ascribed to the growing marine, oil & gas, and petrochemical industries. These factors are contributing to the rising demand for CUI & SOI coatings in the Asia Pacific. Major players operating in the CUI & SOI coatings market include Akzo Nobel N.V. (Netherlands), PPG Industries, Inc., (US), Jotun A/S (Norway), The Sherwin-Williams Company (US), Hempel A/S (Denmark), Kansai Paint Co., Ltd (Japan), Nippon Paint Co., Ltd. (Japan), and RPM International Inc (US). Read More: https://www.marketsandmarkets.com/ResearchInsight/corrosion-under-insulation-cui-spray-on-insulation-soi-coatings-market.asp Chromatography Resin Market Opportunity: Growing demand in drug development and omics research6/13/2022  The global chromatography resin market will grow to USD 3.8 billion by 2027, at a CAGR of 8.0% from USD 2.6 billion in 2022.

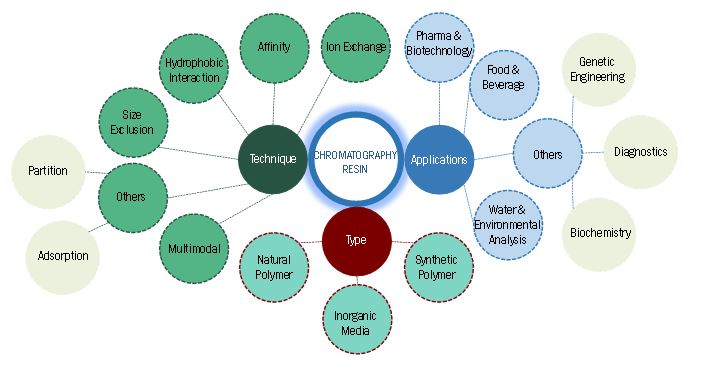

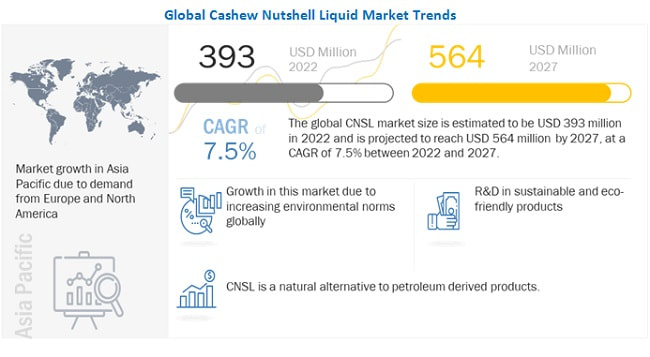

Chromatography represents the most versatile separation technique and is readily available. At the early stage of drug discovery, many closely related compounds are synthesized and are required to be separated. Their identification and purity testing are very essential. Chromatography techniques are widely used for these applications. Chromatography instruments have applications in the separation, purification, and analysis of raw materials, Active Pharmaceutical Ingredients (APIs), and excipients. Thus, the growing requirements for high-quality drugs and implementation of stringent government initiatives are increasing the demand of chromatography resin in several countries. To know about the assumptions considered for the study download the pdf brochure Synthetic resins segment is projected to register the highest CAGR between 2022 and 2027. The demand for synthetic resins is expected to be driven by their use in ion-exchange chromatography. Polystyrene divinylbenzene is the most commonly used synthetic resin, which is increasingly used in IEX technique because of its better performance characteristics in comparison to natural polymers. The growth of the synthetic resins segment is projected to be driven by its increasing use in analytical or laboratory-scale applications. Affinity was the largest chromatography technique in 2021 in terms of value The affinity chromatography technique is based on the selective affinity of molecules in the mobile phase toward ligands coupled to the stationary resin. The rising demand for protein A for convenient and efficient antibody purification is expected to drive the affinity chromatography segment. Affinity chromatography offers high selectivity, resolution, and capacity in most protein purification schemes. It has the advantage of utilizing a protein’s biological structure or function for purification. All these factors drive the demand for affinity technique North America accounted for the largest share of the global chromatography resin market, in terms of both volume and value, in 2021. The US is the leading market for chromatography resin in North America, followed by Canada. A strong therapeutic monoclonal antibody market in North America is one of the key drivers for chromatography resin market. Modern chromatographic techniques are also increasingly used in food analytics and other diagnostic purposes in the US as well as in Canada. Most of the key pharmaceutical companies have their research centers in North America. All these factor drive the demand for chromatography resin in North America. The chromatography resin market is donimated by a few globally established players such as Danaher Corporation (US), Bio-Rad Laboratories Inc. (US), Merck KGaA (Germany), Tosoh Corporation (Japan), BioWorks Technologies AB (Sweden), Kaneka Corporation (Japan), Avantor Performance Materials, Inc (US), Purolite Corporation (US), Repligen Corporation (US), AND Thermo Fisher Scientific Inc. (US). Read More: https://www.marketsandmarkets.com/PressReleases/chromatography-resins.asp  The CNSL market size is estimated to be USD 393 million in 2022 and is projected to reach USD 564 million by 2027, at a CAGR of 7.5% between 2022 and 2027. Increasing demand from the chemical and petrochemical industries, the rising demand for natural resources for various applications are significantly driving the market globally.

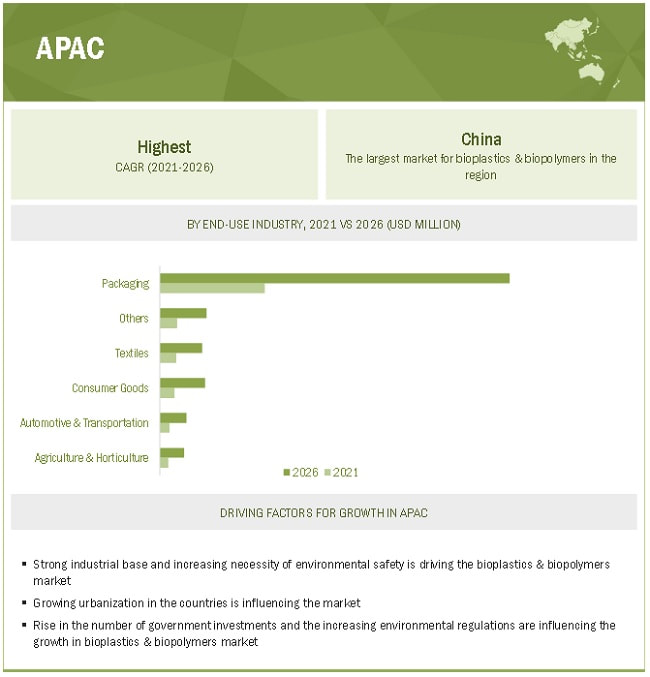

The CNSL market in Europe is segmented into Germany, France, the UK, Italy, the Netherlands, and Rest of Europe. The chemical industry is a significant part of the region’s economy. The growth is driven by investments made in this region by global chemical companies. Though the steady European economic recovery is expected to drive the market, the adoption of several strict regulations against the use of petroleum-based products is likely to challenge the market growth in the region. To know about the assumptions considered for the study download the pdf brochure The key market players are cardolite company(U.S.A), pelmer international(U.S.A), senesel(Poland), sri devi group(India). Cardolite Corporation is a manufacturer of CNSL-based products used in coatings, friction materials, adhesives, composites, and foams. The company is the leader in the production of quality CNSL-based materials. Cardolite delivers high-quality products and services across the globe and has sales offices, representatives, and distribution facilities in the Americas, Europe, and Asia. Palmer International is a global leader in CNSL technology. The company provides polyols, chemicals, friction particles, and resins to automotive, transport, construction, and other industries worldwide. It is the world’s oldest producer of cashew derivatives and a leader in developing OEM friction particles. The company is the worlds leading producer of cashew-manic polyols and epoxy hardener chemistry. Read More: https://www.marketsandmarkets.com/PressReleases/cashew-nutshell-liquid.asp  Global bioplastics & biopolymers market size is projected to grow from USD 10.7 billion in 2021 to USD 29.7 billion by 2026, at a CAGR of 22.7% between 2021 and 2026. Bioplastics are plastics derived from renewable sources such as corn, potatoes, rice, soy, sugarcane, wheat, and vegetable oil, while biopolymers are naturally occurring polymers. A bioplastic may or may not be biodegradable. Bioplastics are mainly segmented into biodegradable and non-biodegradable plastics for various applications in the packaging, consumer goods, automotive & transportation, agriculture & horticulture, medical, and other end-use industries.

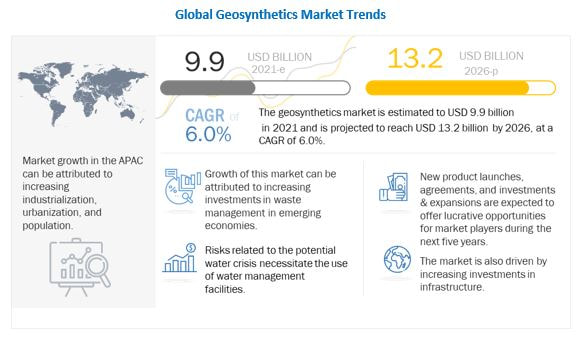

To know about the assumptions considered for the study download the pdf brochure Packaging is the largest end-use industry for the application of bioplastics & biopolymers. They accounted for the share of 61.6%, in 2020, for the global bioplastics & biopolymers market. Increasing environmental regulations and changes in the lifestyle of consumers have increased the demand for bioplastics & biopolymers in the packaging industry. Plastics have high durability and impermeability to water, which has encouraged their use in packaging. Packaging applications of bioplastics & biopolymers include food packaging, healthcare packaging, cosmetic & personal care packaging, shopping bags, and others. High potential in emerging countries of APAC The bioplastics & biopolymers market players are continuously implementing organic and inorganic strategies for their growth. In recent years, the players have made many strategic developments in the emerging countries of APAC. For instance, in 2019, Total Corbion set up a PLA Plant in Rayong, Thailand, with a production capacity of 75,000 tons per year. In the same year, Mitsubishi Chemical Holding Corporation (Japan) and Lenovo Group Limited (China) entered into a joint venture to produce a bioplastic-based body (3D shape rear panel) for smartphones. In addition, Indonesia is exploring bioplastic alternatives, such as seaweed. Evoware, a local player, provides patented seaweed-based packaging. The company is producing containers made from seaweed. The regulations related to the environment are expected to increase, which would eventually propel the demand for bioplastics in these countries in the future. Moreover, Southeast Asia is rich in bio-based feedstock required to produce bioplastic as it has local access to sustainable raw materials. Thus, regulations, coupled with the easy availability of feedstock, will, in turn, help sustain the demand for bioplastics during the forecast period. The key players in this market are NatureWorks (US), Braskem (Brazil), BASF (Germany), Total Corbion (Netherlands), Novamont (Italy), Biome Bioplastics (UK), Mitsubishi Chemical Holding Corporation (Japan), Biotec (Germany), Toray Industries (Japan), and Plantic Technologies (Australia). Read More: https://www.marketsandmarkets.com/ResearchInsight/biopolymers-bioplastics-market.asp  The global geosynthetics market is projected to reach USD 13.2 billion by 2026 from USD 9.9 billion in 2021, at a CAGR of 6.0% between 2021 and 2026.

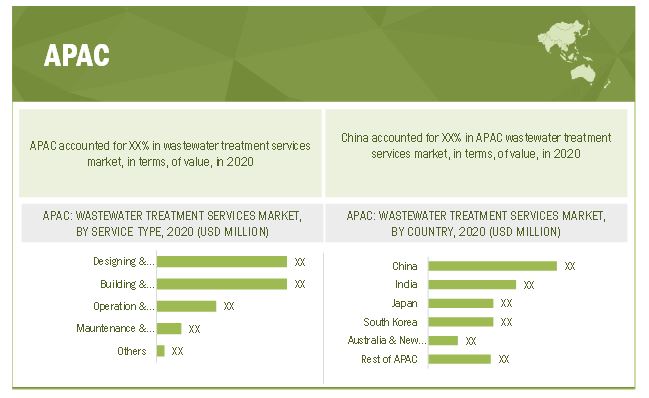

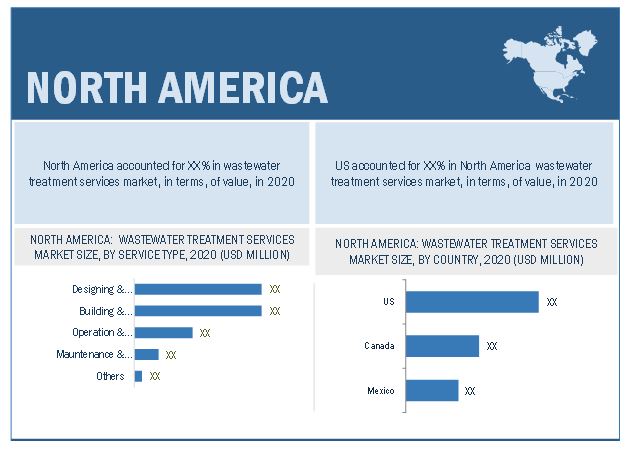

Rapidly increasing population and urbanization is contributing in increasing levels of solid and liquid wastes across the globe. Rising environmental awareness is leading to an increase in the demand for appropriate waste and water management projects. Geosynthetics are used as landfill caps to prevent the migration of fluids into landfills by reducing or eliminating the post-closure generation of leachate and associated treatment costs. Geosynthetics are widely used in various water management activities owing to the increasing public concerns in serious and widespread water pollution. Geosynthetics liner systems are used in waste treatment lagoons at wastewater treatment plants to protect water resources including lakes, rivers, ponds, aquifers, and reservoirs which is expected to boost the demand for geosynthetics during the forecast period. To know about the assumptions considered for the study download the pdf brochure Waste management contributes for the largest market share for the geosynthetics market in 2020. Geosynthetics are used in waste management for performing various functions such as filtration, separation, drainage, barrier, and reinforcement. It includes the proper collection, transport, treatment, recycling, and disposal of residential, industrial, and commercial waste. Geosynthetics are essential for controlling the leakage of contaminated gas and liquid into groundwater, rivers, aquifers, and other freshwater sources. The rising demand for waste management owing to increase in population, urbanization, and industrialization is expected to drive the geosynthetics market during the forecast period. Geosynthetics market is dominated by APAC in 2020. The region is growing at a faster rate which accounts for the high growth of the geosynthetics market. The emerging market of India, China, and other countries of the APAC are growing and boosting the regional market growth. Rapidly increasing population, urbanization, and industrialization are expected to drive the geosynthetics market in APAC. Rising investment In the development of public infrastructure and growing demand for solid waste management system are the major factors driving the geosynthetics demand in the region. Key players in the geosynthetics market are SOLMAX (Canada), NAUE GmbH & Co. KG (Germany), Officine Maccaferri Spa ( Italy), Berry Global Inc ( US), and Agru America, Inc ( US) are the major players in the market. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1174 The wastewater treatment services market size is estimated to be USD 53.0 billion in 2021 and is projected to reach USD 71.6 billion by 2026, at a CAGR of 6.2% between 2021 and 2026. . Growing population, expanding manufacturing industry, urbanization, and regulatory requirements are the major drivers of the wastewater treatment services market. Initiatives by manufacturing industries and state bodies for low waste generation and growing awareness about new water treatment technologies are some of the factors which are likely to boost the wastewater treatment services market. APAC is expected to be the fastest-growing wastewater treatment services market.  The APAC comprises major emerging nations such as China and India. Hence, the scope for the development of most industries is high in this region. The wastewater treatment services market is growing significantly and offers opportunities for various industries. The APAC region constitutes approximately 61.0% of the world’s population, and the manufacturing and processing sectors are growing rapidly in the region. The APAC is the largest wastewater treatment services market with China being the major market which is expected to grow significantly. The rising disposable incomes and rising standards of living in emerging economies in the APAC are the major drivers for this market. To know about the assumptions considered for the study download the pdf brochure The increasing population in the region accompanied with development of new technologies and products are projected to make this region an ideal destination for the growth of the wastewater treatment services market. However, establishing new plants, implementing new technologies, and creating a value supply chain between raw material providers and manufacturing industries in the emerging regions of the APAC are expected to be a challenge for industry players as there is low urbanization and industrialization. Booming power, consumer goods and packaging sectors and advances in process manufacturing are some of the key drivers for the market in the APAC. Countries such as India, Japan, and China are expected to witness high growth in the wastewater treatment services market due to the increasing demand from the food, pulp & paper, chemical, and power & generation industry. North America is estimated to be the largest wastewater treatment services market  North America is the largest wastewater treatment services market in the world. Key countries in the region include US, Canada and Mexico. As the market in North America is mature, it is projected to grow at a lower CAGR during the next five years. North America has always been a major wastewater treatment services market due to the presence of developed industrial sector in the region. This market is growing more due to adoption of stringent regulations towards environment.

Many economies throughout the world have been adversely hit by the COVID-19 outbreak. Governments throughout the world have imposed partial or complete lockdowns to prevent the spread of the disease and its effects, affecting a wide range of manufacturing and service industries, including water and wastewater treatment.COVID-19 has affected the wastewater treatment services market only in industrial applications in the first two quarters of 2020. According to an article, wastewater treatment services for industrial applications have been impacted because of the pandemic as Industries were shut down due to the lockdown restrictions and there was no production, which in turn reduced the wastewater production. The key players in the market are focusing on strategies, such as new product launches, partnerships & agreements, acquisitions, and expansions, to expand their businesses globally The key players operating in the wastewater treatment services market are trying to increase their scope of services to address the increasing demand. Veolia Water Technologies (France), SUEZ (France), Xylem (US), Evoqua Water Technologies (US), Thermax (India), and Ecolab (US) are the leading providers of wastewater treatment services, globally. Request for Sample Paper: https://www.marketsandmarkets.com/requestsampleNew.asp?id=38039841  The insulating glass window market size was USD 12.0 billion in 2020 and is projected to reach USD 17.2 billion by 2026; it is expected to grow at a CAGR of 6.1% from 2021 to 2026. The commercial segment accounted for the largest share of the insulating glass window market in 2020, owing to the increasing rate of commercial building construction in the countries such as the US, Germany, China, and India.

North America is projected to be the largest regional market for insulating glass windows. The market in North America is driven by moderate growth in the construction industry. Glass insulation is considered a viable option for making buildings energy-efficient. Also, factors such as the high quality of infrastructural construction, reduced environmental impact, climatic conditions, and government regulations are fueling the growth of energy-efficient windows in North America. To know about the assumptions considered for the study download the pdf brochure Middle East & Africa region is projected to show positive growth, especially in the commercial construction industry, due to factors such as government initiatives (Saudi Arabia’s Vision 2030), increasing urbanization, and industrialization. Also, the Middle East & African insulating glass window market is projected to witness high growth till 2022, mainly because of the upcoming infrastructural projects such as Expo 2020 (UAE) and the 2022 FIFA World Cup (Qatar). Recent Developments

Request for Sample Paper: https://www.marketsandmarkets.com/requestsampleNew.asp?id=36258309  In 2020, the Chlor-Alkali market saw a dip in growth rate due to COVID-19 and the consequent lockdown across the world. The COVID-19 pandemic has severely impacted North American and European countries. Several manufacturing activities have been suspended as a preventive measure. Disruptions in supply chains impacted the chlor-alkali and other end-use industries, and demand declined by over 5% in a majority of the applications. Several expansion projects across the globe have been suspended, which has resulted in a decline in demand for chlor-alkali. The demand for the chemicals, organic, and inorganic chemicals declined significantly across the globe. To mitigate the impact, several chemical companies in North America and Europe are channelizing focus on operational efficiency, cost management, and asset optimization.

To know about the assumptions considered for the study download the pdf brochure Key players are also focusing on long-term opportunities such as emerging applications, investing in innovations, studying customer buying behavior patterns, and adopting new business models that help generate sustained growth, among others. Due to the pandemic, various building construction and infrastructural projects were suspended or postponed across the globe. Therefore, the demand for PVC declined across the globe, which, in turn, impacted the chlorine market. Decline in automotive industry further reduced the demand for glass and polymers. Moreover, water treatment projects were either rescheduled or suspended, which, in turn, will have a significant impact on the market. The global Chlor-Alkali market size is estimated to be USD 63.2 billion in 2021 and is projected to reach USD 77.4 billion by 2026, at a CAGR of 4.1%. The growth in demand for chlor-alkali in the APAC is expected to be driven by the vinyl chain (EDC/VCM/PVC). The demand for chlor-alkali in the APAC is driven by China, which accounts for a major share, globally. China is one of the fastest-growing countries, in terms of chlor-alkali consumption, due to its large chemical and petrochemical industries. India, with its emerging economy is expected to propel the demand for chlor-alkali products during the forecast period. The rising disposable income and focus on the domestic manufacturing industry is expected to increase the demand for chlor-alkali products. However, in Europe, the market for chlor-alkali products is projected to grow at a marginal rate during the forecast period. In North America, and particularly in the US, the growth in demand for chlorine is expected to be driven by the vinyl chain (EDC/VCM/PVC). New capacities are expected to be introduced as the demand from the vinyl industry is projected to increase due to the rising demand from the construction and residential housing sectors in the US. Chlor-alkali products, namely, chlorine, caustic soda, and soda ash are utilized in various industries. Chlorine and caustic soda are produced through the electrolysis of brine, and soda ash is produced through the Solvay process. These three products are used as raw materials in various industries; chlorine is a vital building block and more than 60% industrial chemicals require it in some form or other in production processes. Caustic soda finds applications in personal care products such as soaps and detergents. Soda ash is used in the glass industry, chemicals, and for water treatment. Some applications such as water treatment, food, and pulp & paper are common in all the three chlor-alkali products. The Chlor-Alkali market is segmented on the basis of type as Chlorine, Caustic Soda, Soda Ash, and others. Chlorine plays an important role in various chemical industries. It is a building block in chemistry because of its reactivity and bonding characteristics. It is produced by electrolysis, majorly with the use of the membrane cell technology. Some of the manufacturers use diaphragm technology and mercury cell technology. Chlorine reacts with almost all elements, except lighter noble gases. It is a good disinfectant and bleaching agent. Chlorine applications includes EDC/PVC, organic chemicals, inorganic chemicals, isocyanates, chlorinated intermediates, propylene oxide, pulp & paper, C1/C2/ aromatics, water treatment, and others. The leading players in the Chlor-Alkali market are Olin Corporation(US), Westlake Chemical Corporation (US), Tata Chemicals Limited (India), Occidental Petroleum Corporation (US), Formosa Plastics Corporation (Taiwan), Solvay SA (Belgium), Tosoh Corporation (Japan), Hanwha Solutions Corporation (South Korea), Nirma Limited (India), AGC, Inc. (Japan), Dow Inc. (US), Xinjiang Zhongtai Chemical Co. Ltd. (China), INOVYN (UK), Ciner Resources Corporation (US), Wanhua-Borsodchem (Hungary), and others. Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=708  APAC led the global electrical conduit market, accounting for a share of 37.8% in 2020. APAC is segmented into China, Japan, India, South Korea, and the Rest of APAC. Factors such as ready availability of raw materials and manpower, along with sophisticated technologies and innovations, have driven economic growth in the APAC region. Emerging economies in APAC are expected to have significant demand for electrical conduit due to the growth of the construction industry led by the rapid economic development and government initiatives in infrastructural developments. In addition, the rising population in these countries represents a strong customer base.

APAC is expected to be the fastest-growing market for electrical conduit globally during the forecast period. Significant consumer base, rising urban population, low labor costs, and easy availability of raw materials are attracting international companies to shift their production facilities to the region, thus creating a high demand for electrical conduits in these industries. The increase in demand for electrical conduit can be largely attributed to the growing infrastructure and building & construction industries. The demand for electrical conduits is rising rapidly in the region owing to the high demand from the infrastructural sector. To know about the assumptions considered for the study download the pdf brochure The global electrical conduit market is estimated to be USD 6.5 billion in 2021 and is projected to reach USD 9.1 billion by 2026, at a CAGR of 6.9% from 2021 to 2026. The driving factors for the electrical conduit market is rapid pace of industrialization and urbanization, and rise in demand for electricity or power generation across the globe. The growth of the electrical conduit market is supported by increasing awareness regarding public safety and the implementation of safety regulations by governments. Atkore International Group Inc. (US), Hubbell Incorporated (US), Legrand S.A. (France), Schneider Electric SE (France), and Sekisui Chemical Co., Ltd. (Japan) among others, are the leading electrical conduit manufacturers, globally. These key players have focused on market consolidation by adopting both organic and inorganic growth strategies such as mergers & acquisitions. These companies adopted acquisitions as the key growth strategy between 2019 and 2021. Atkore International Group Inc. is one of the largest player in the electrical conduit market. It engages in the manufacture of electrical raceway products, primarily for the non-residential construction and renovation markets. It operates through the Electrical Raceway and Mechanical Products and Solutions (MP&S) segments. Some of its products include electrical conduit and fittings, armored cable and fittings, cable trays, mounting systems and fittings, metal framing, and in-line galvanized mechanical tube. The company operates through 37 manufacturing facilities and 28 distribution facilities. Major subsidiaries of the company include Allied Tube & Conduit (Italy), Calpipe Industries (Spain) and Unistrut Limited (UK). Hubbell Incorporated is the second-largest player of the global electrical conduit market. The company is a manufacturer of electrical, lighting, and power components worldwide. It operates through two segments, namely Electrical Solutions and Utility Solutions. The company offers its products and solutions to various industries such as non-residential & residential construction, industrial, and energy-related (oil and gas) markets. The company has a presence in Singapore, China, India, Mexico, South Korea, and countries in the Middle East and has a joint venture in Taiwan and Hong Kong. Hubbell has its subsidiaries in the US, Canada, Switzerland, Puerto Rico, China, Mexico, Italy, the UK, Brazil, Australia, and Ireland. It operates through 52 manufacturing facilities and 18 warehouses. Some of the key brands through which the company serves its products are Bell, Raco, Gleason Reel, Bryant, and Wiegmann. Read More: https://www.marketsandmarkets.com/PressReleases/electrical-conduit.asp |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed